18 December

Asia

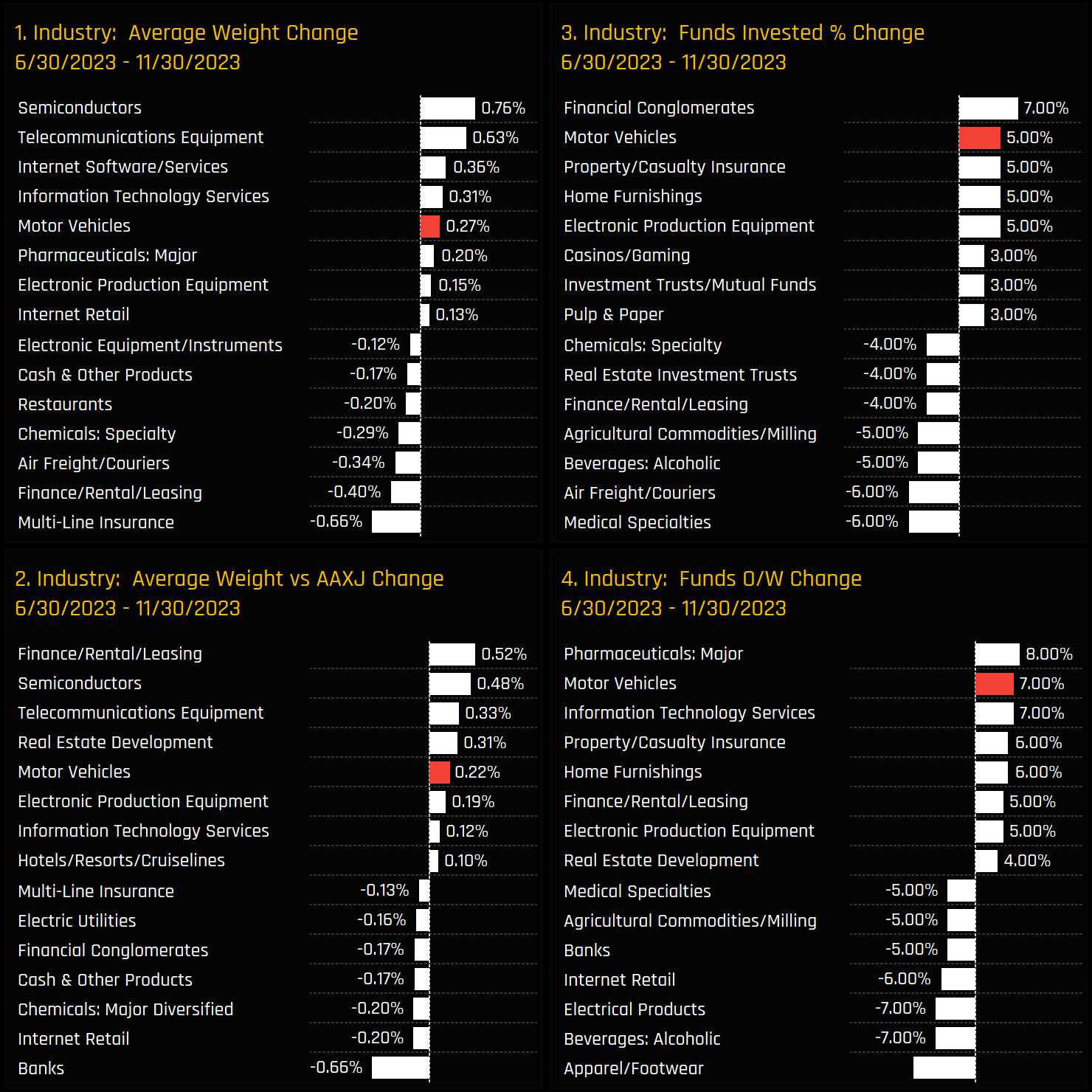

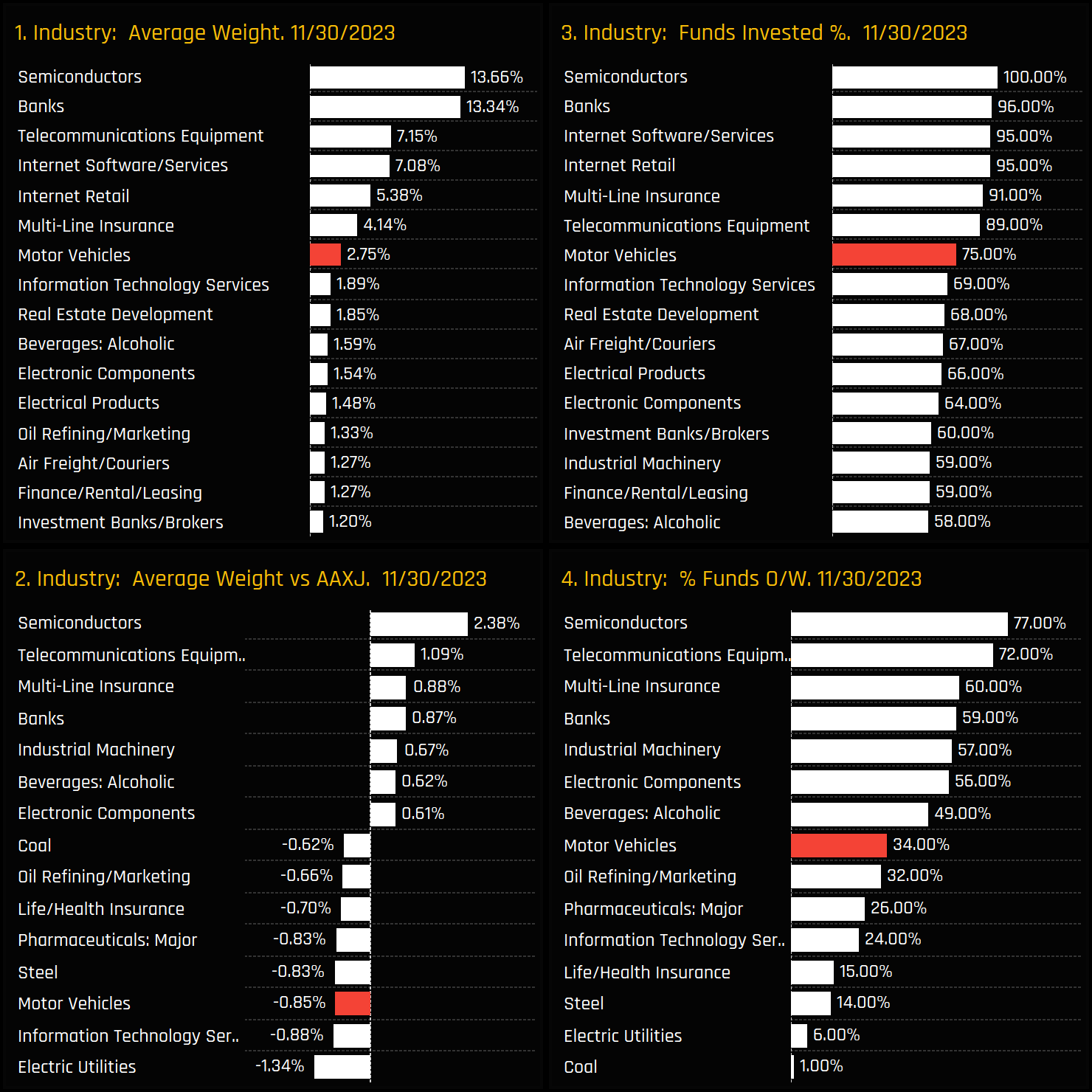

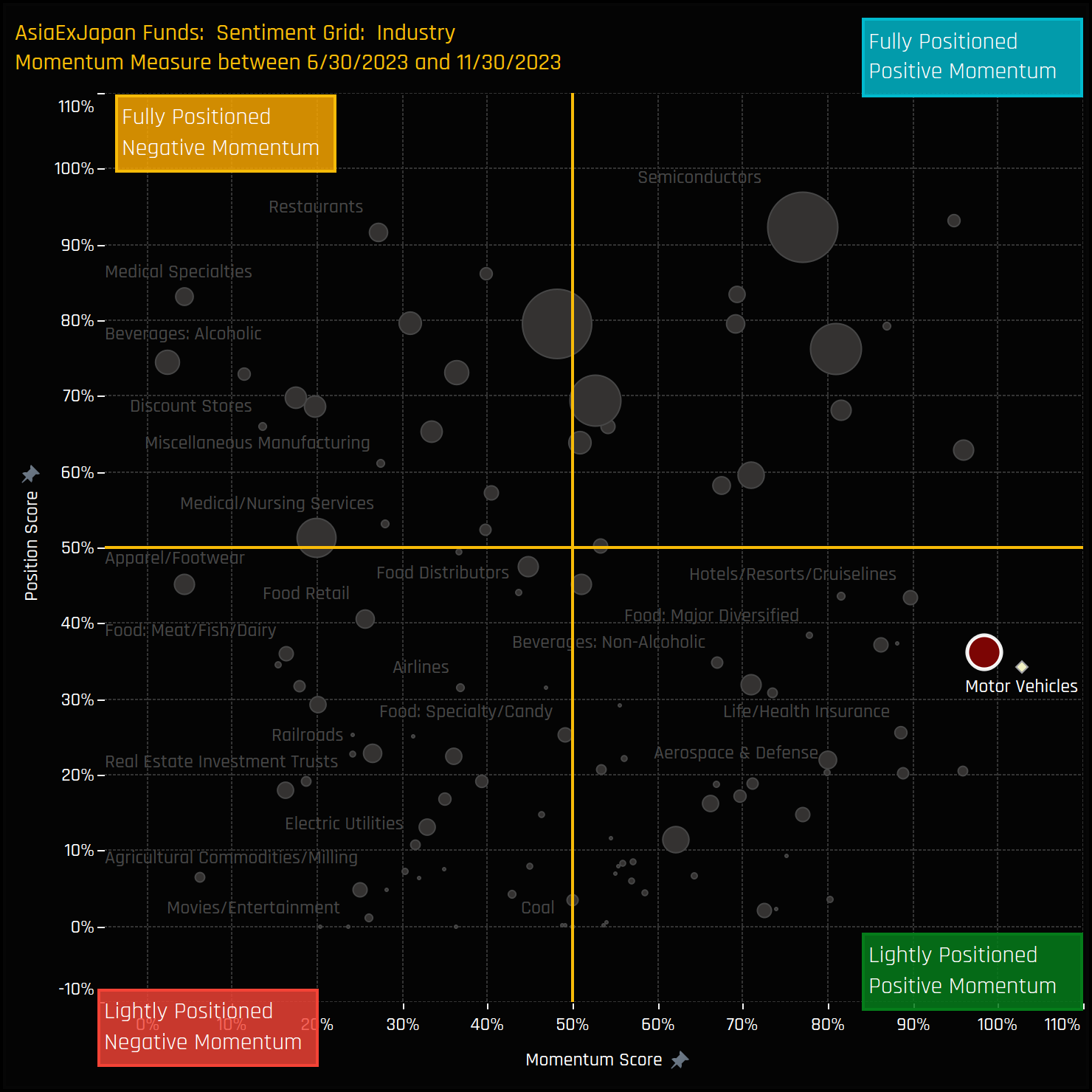

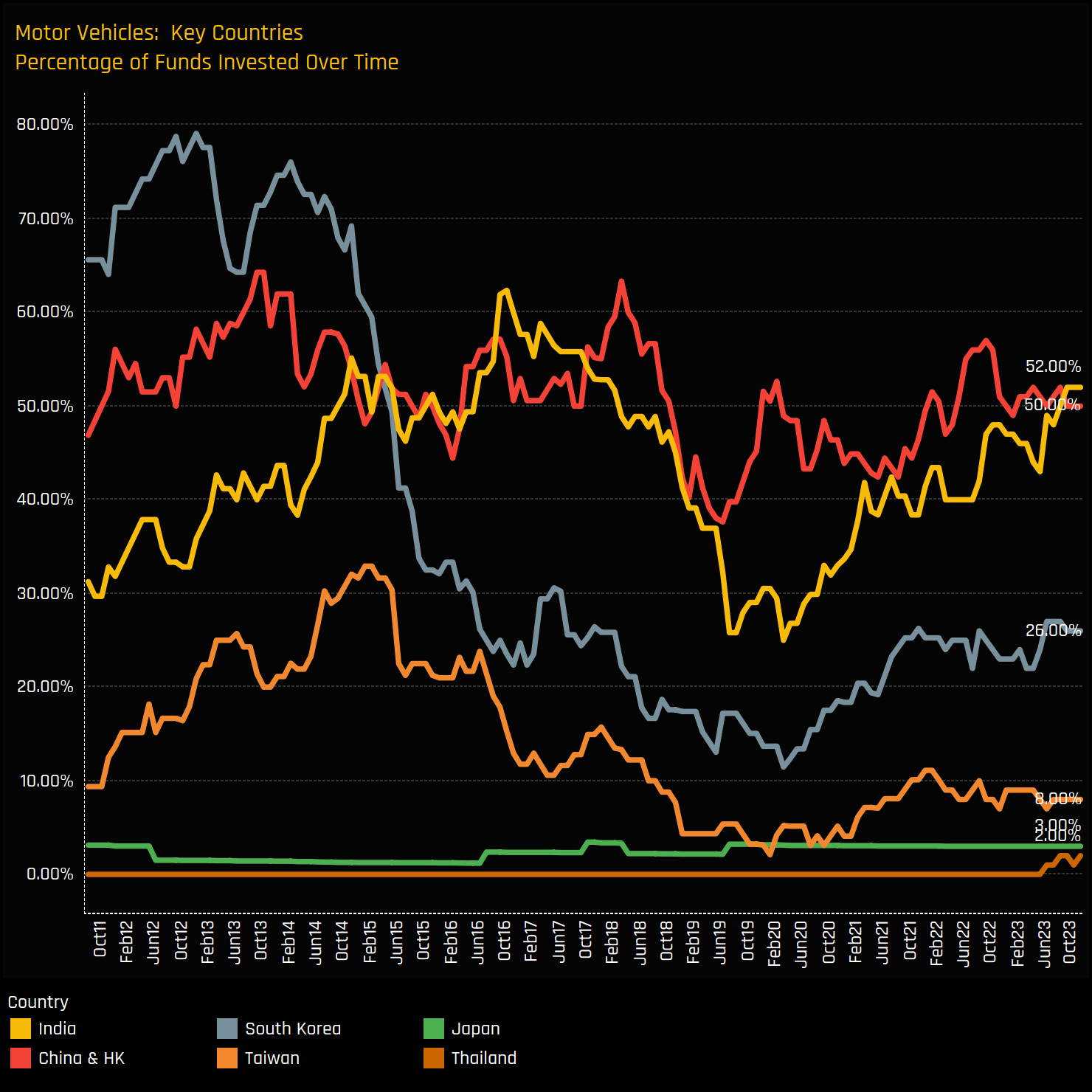

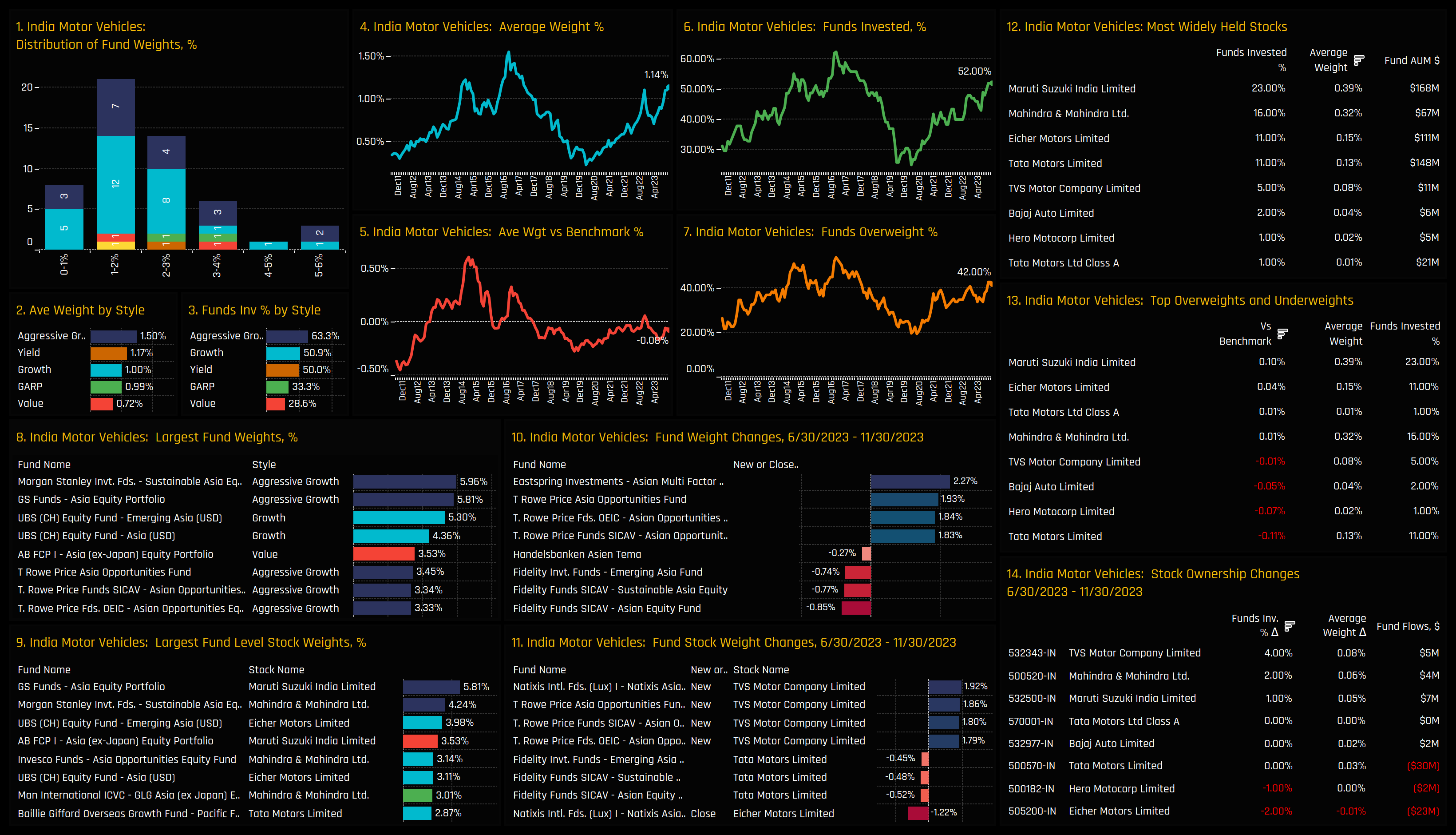

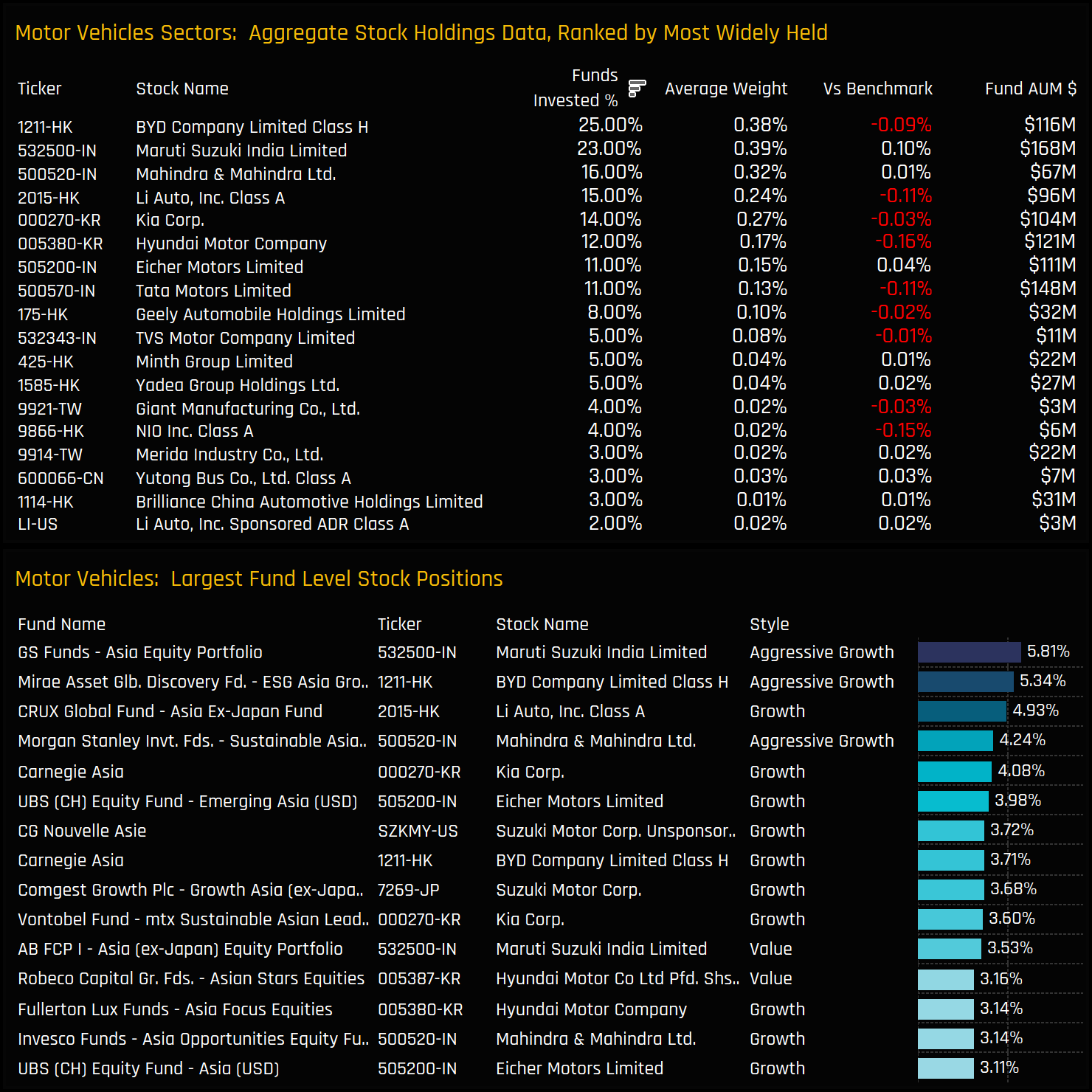

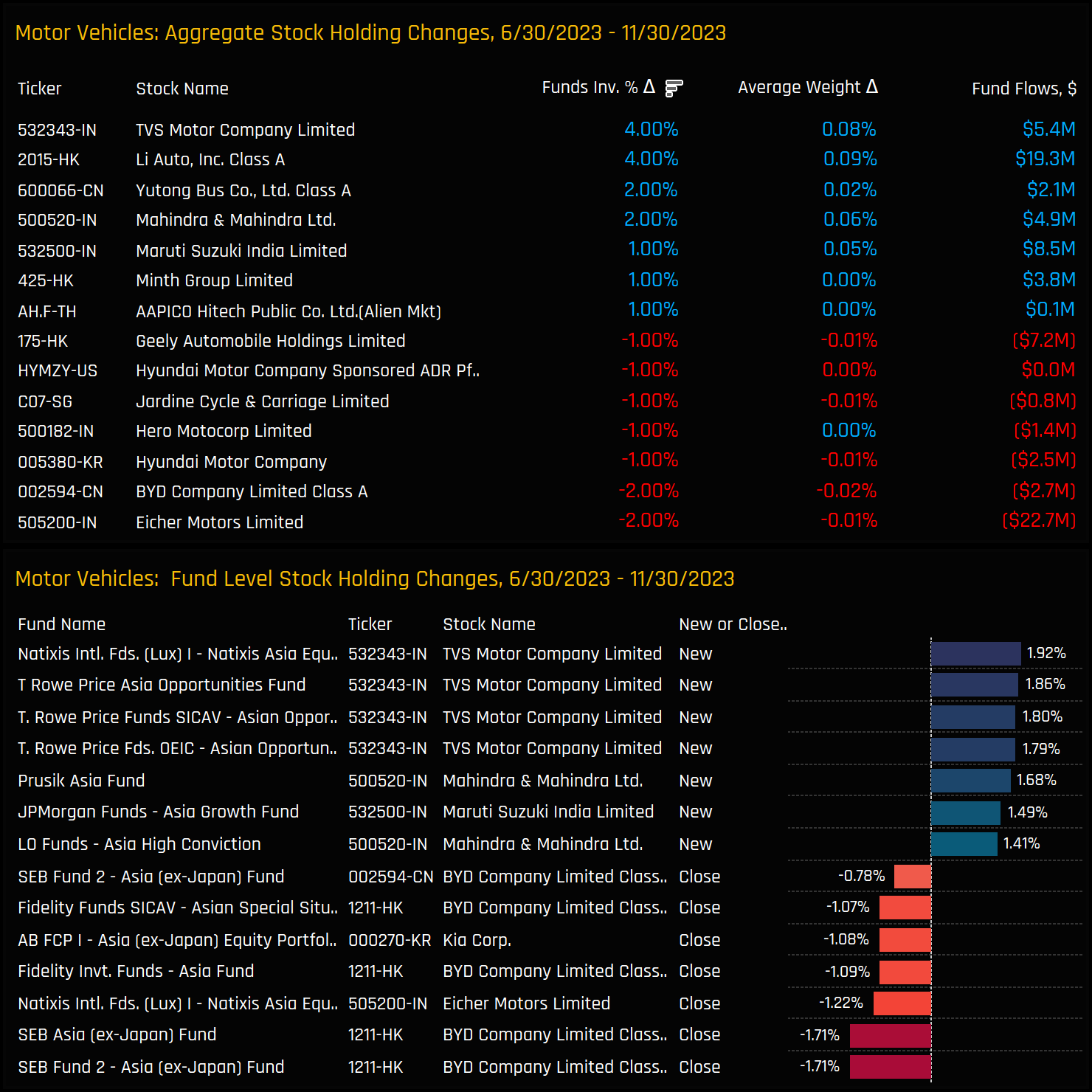

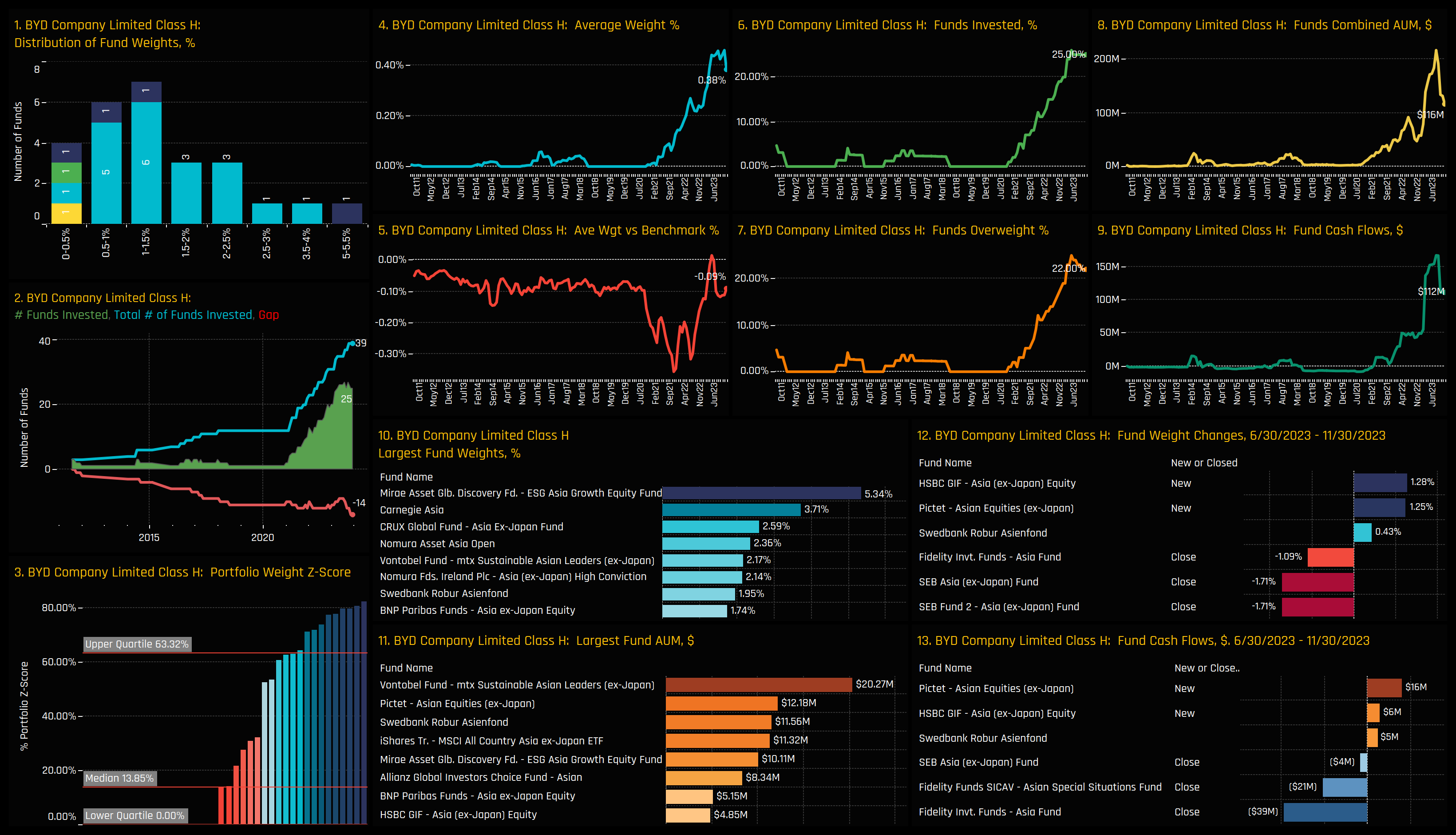

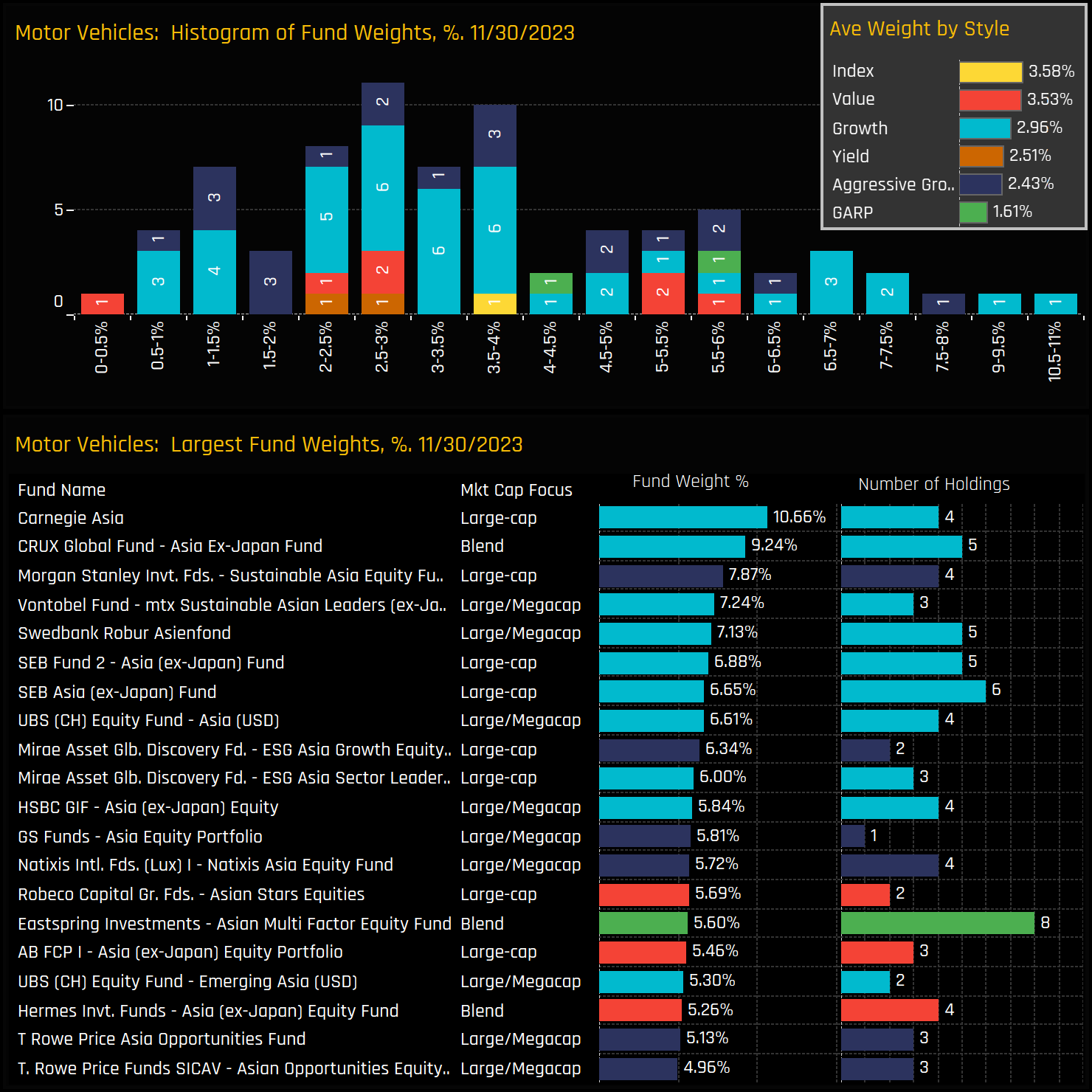

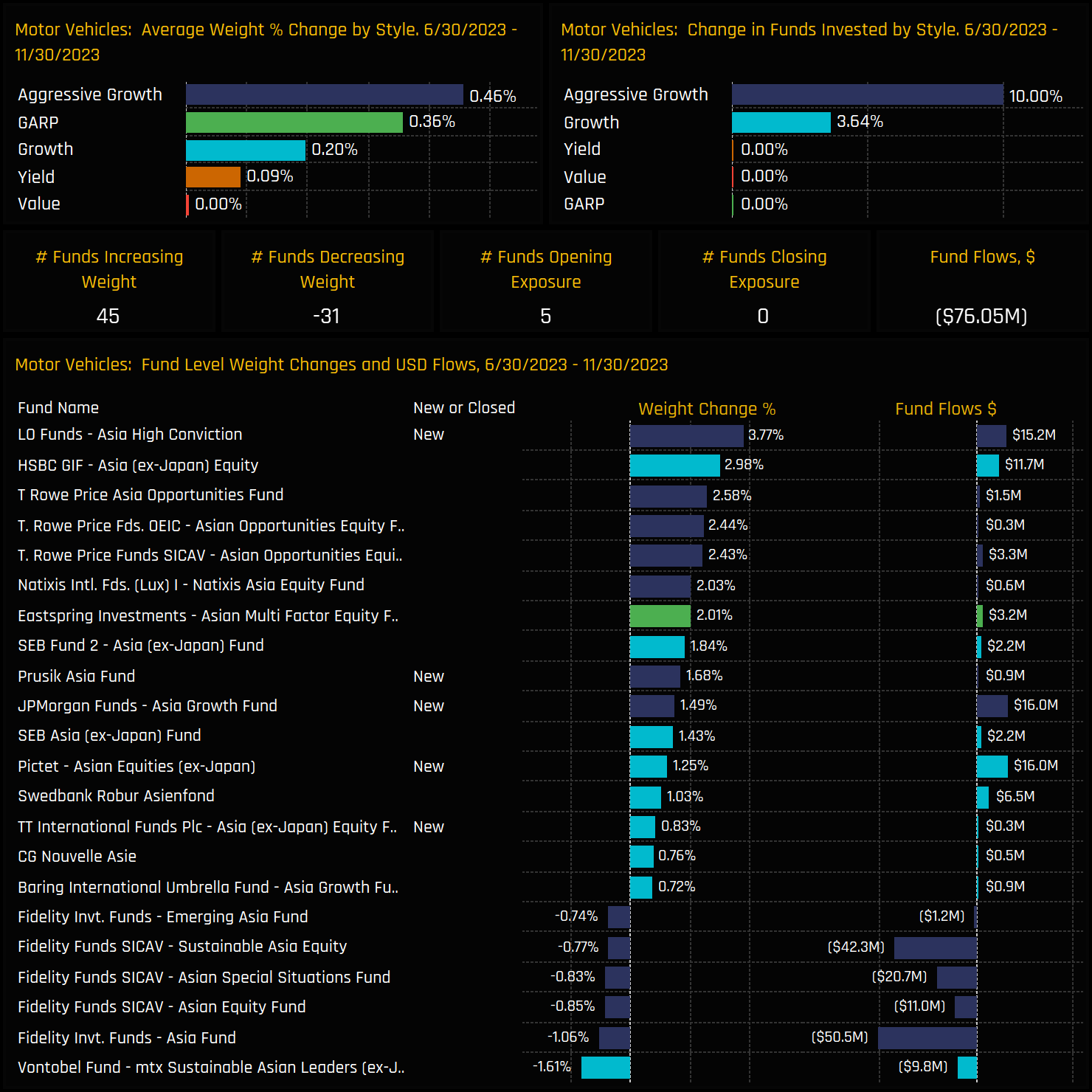

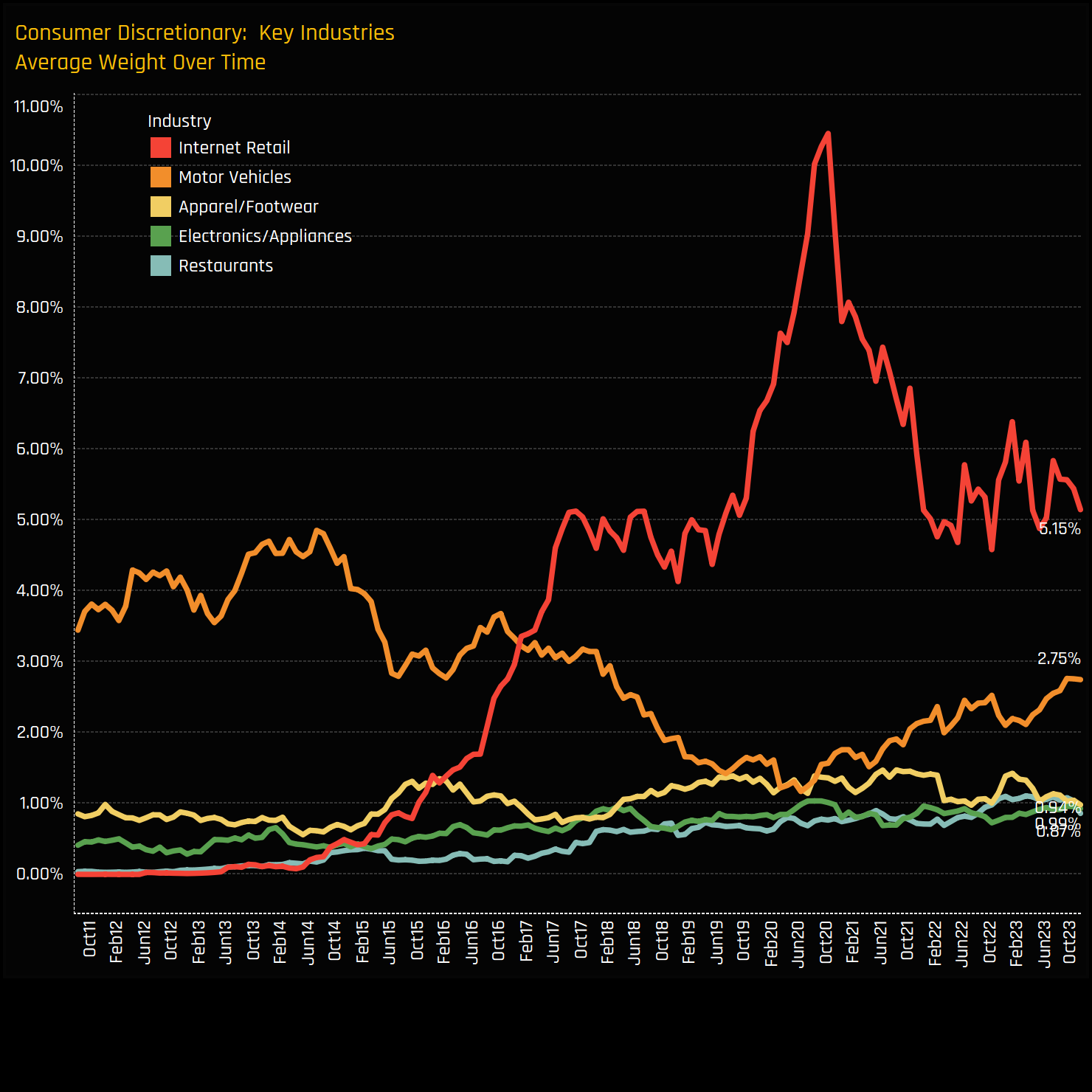

Asian Autos: Increasing Exposure Reflects Rising Market Confidence

- Steve Holden

- 0 Comments

Related Posts

{kind=link}