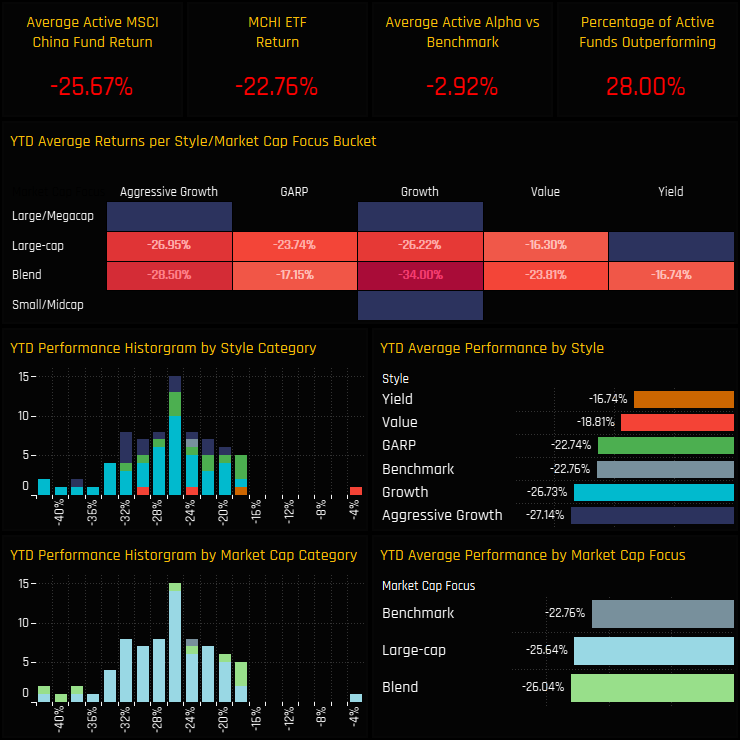

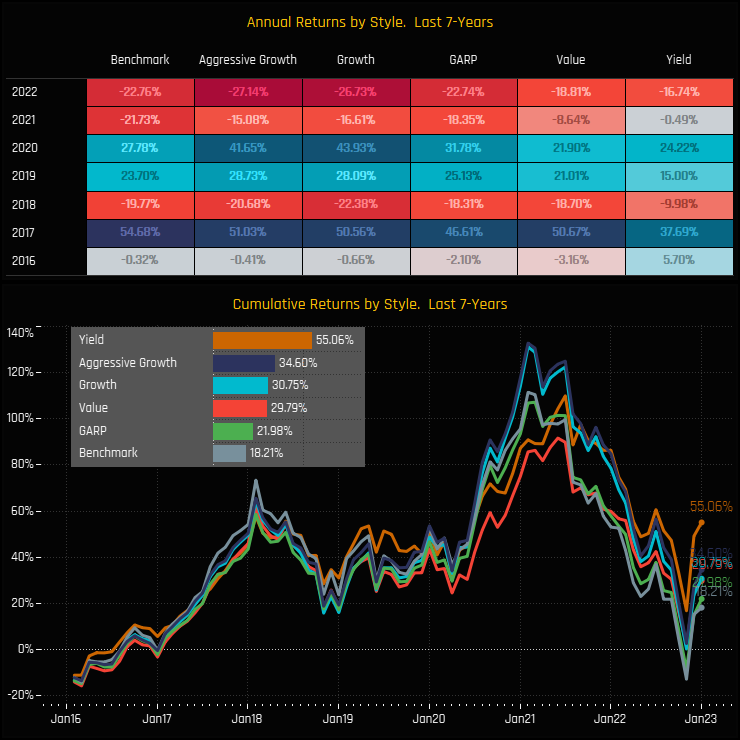

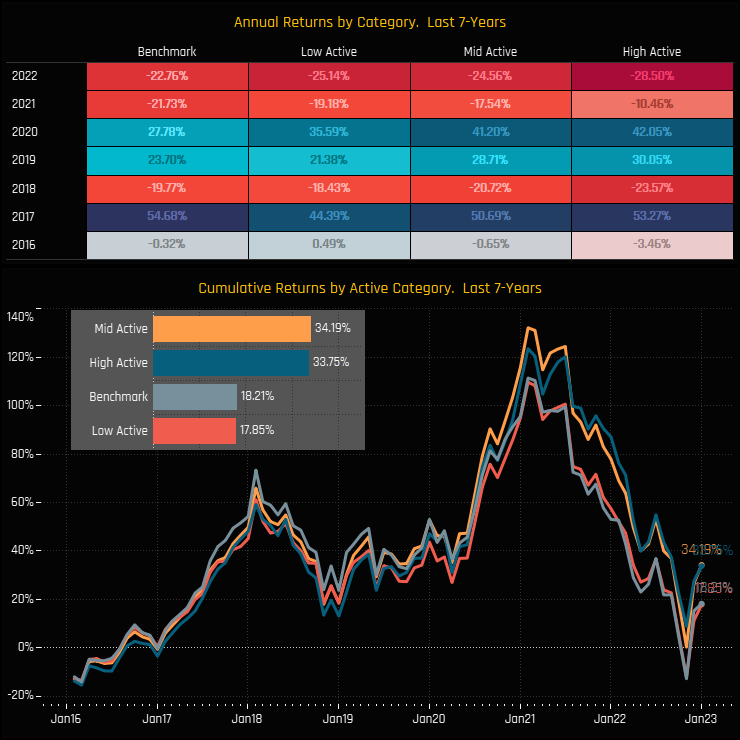

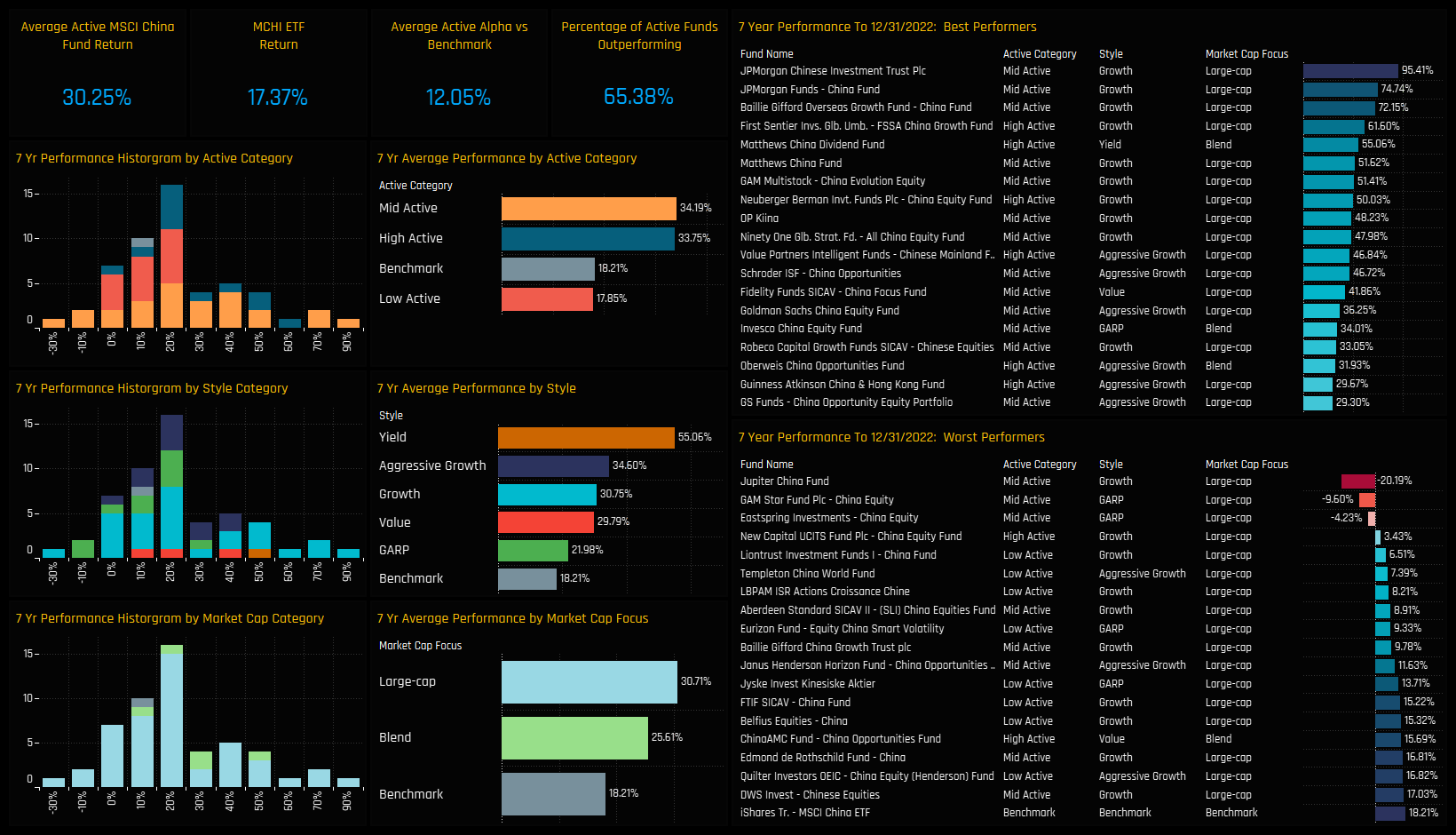

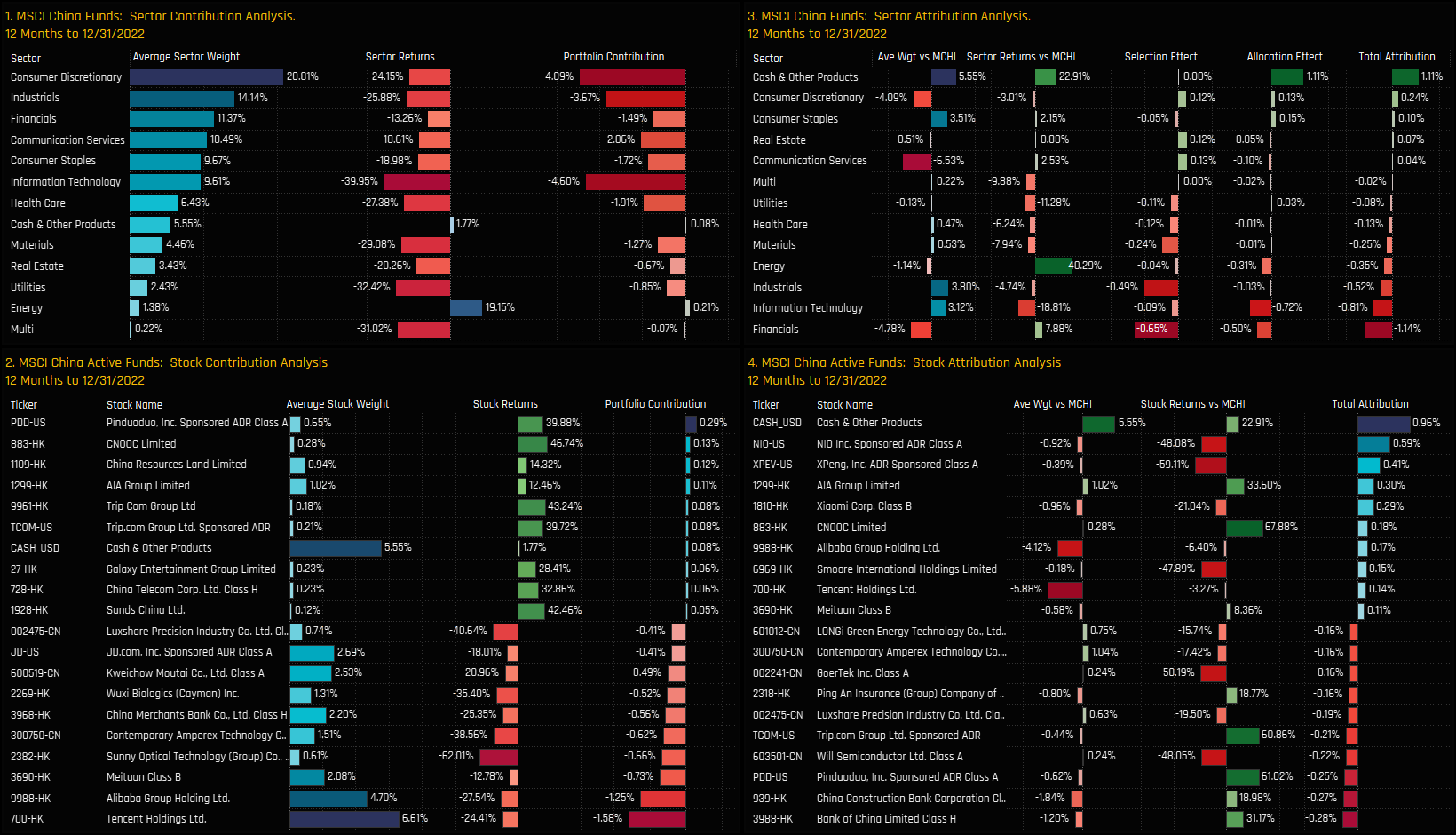

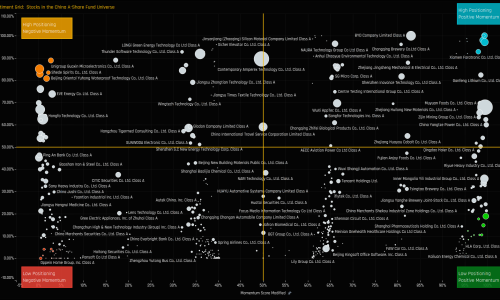

2022 was a rough year for active China managers on all fronts. In absolute terms, average returns came in at -25.67%. Versus the iShares MCHI ETF, this equates to a 2022 underperformance of -2.92%, with just 28% of strategies outperforming. There is a Style correlation to returns, with Yield and Value outperforming Growth/Aggressive Growth, though the small number of funds in the former categories needs to be taken in to account.

{kind=link}