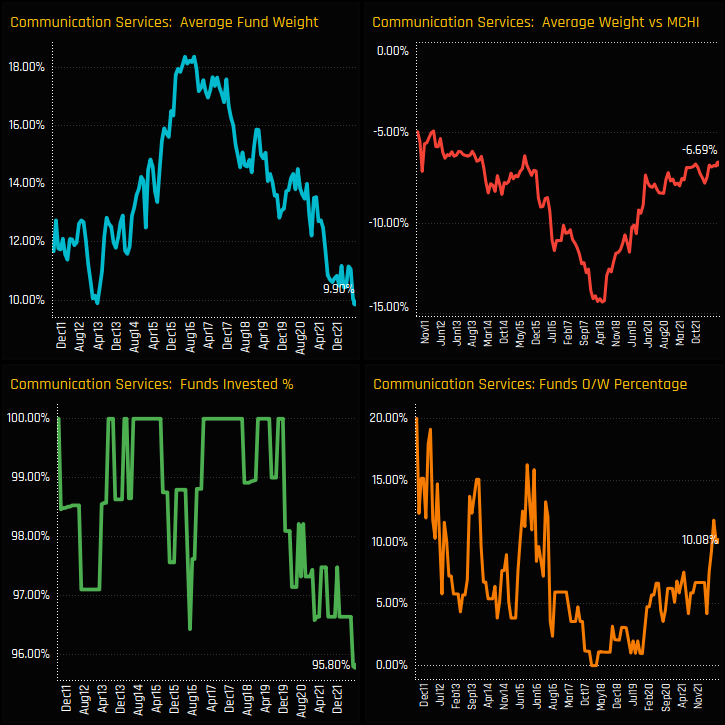

Portfolio weights in the Communication Services sector have hit their lowest levels on record, declining from a high of over 18% in mid-2015 to just 9.90% today. In this analysis. we look at positioning in the communication services sector in detail, highlighting the funds and stocks that make up exposure in the sector.

Time-Series & Sector Positioning

Communication Services allocations among active China managers are at their lowest levels on record. Average weights stand at an all-time low of 9.90%, only the second time in over a decade that exposure has dipped below 10% and a far cry from the 18%+ allocations in mid-2016. Though the sector remains widely owned, the percentage of funds invested has dropped to its lowest ever level of 95.80%. The decreasing underweight in combination with the falling average weight infers some of the allocation shift was also down to price, and the under-performance of key stock underweights.

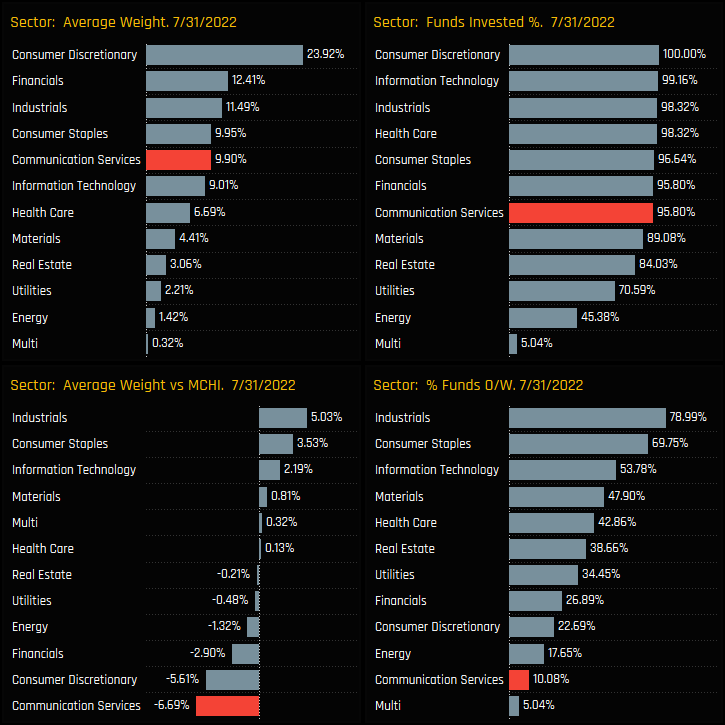

Versus sector peers, Communication Services are now the 5th largest sector allocation on an average weight basis and the 7th most widely owned. Versus the iShares MCHI ETF, the current average weight of 9.90% represents a significant underweight of -6.69% below benchmark, the largest among sector peers and offset by overweights in Industrials and Consumer Staples. The Consumer Discretionary sector remains the standout allocation on an absolute basis, yet it too is held underweight by active China managers.

Fund Holdings & Style

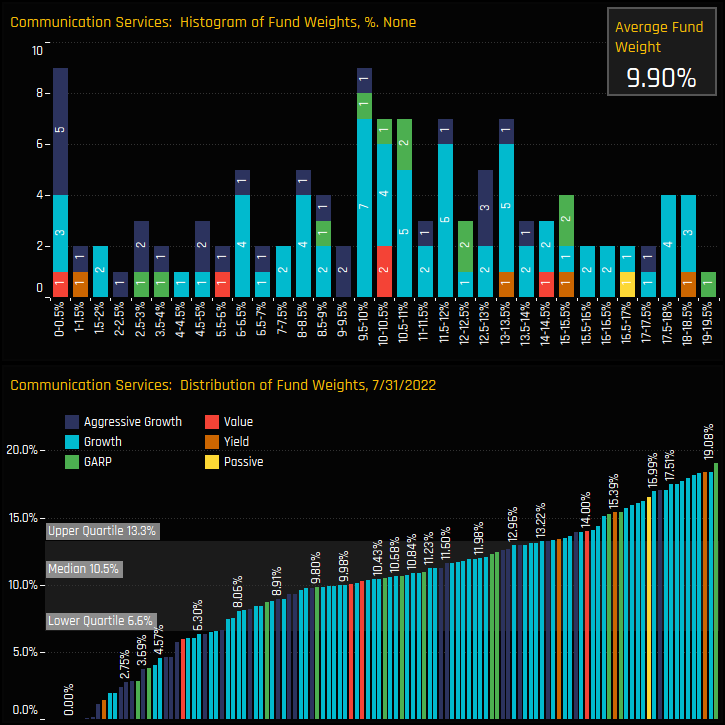

The holdings distribution in the Communication Services sector is well spread from a minimum of zero up to a maximum of 19.1%, with the bulk of allocations between 9.5% and 13.5%. At the extremes, 20 managers hold above 15% offset by 9 managers who hold less than 0.5%. The median allocation is 10.5%, with 75% of managers allocating between 6.6% and 13.3% in the Communication Services sector.

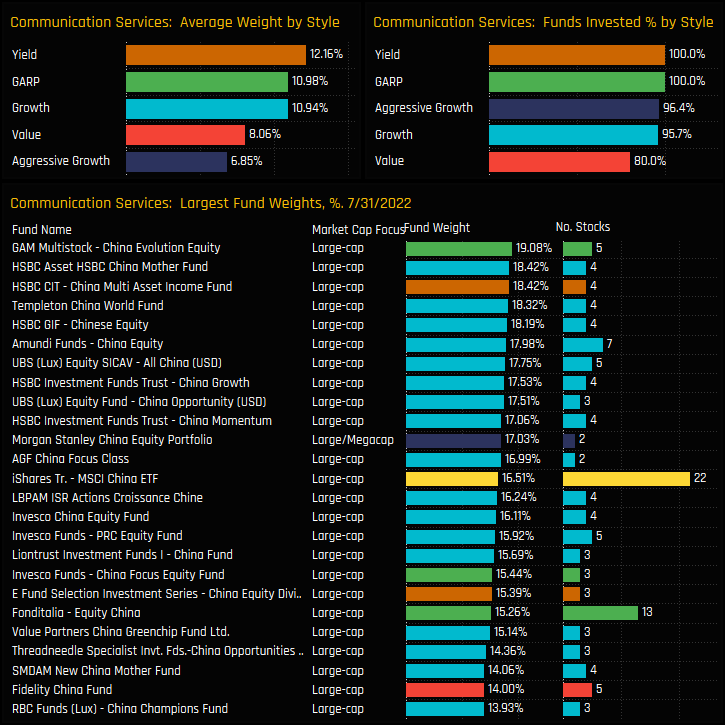

Yield, GARP and Growth managers are well exposed, led by GAM China Evolution (19.08%), HSBC China Mother Fund (18.42%) and HSBC China Multi Asset Income (18.42%). Value and Aggressive Growth managers hold significantly less on average. Most managers hold between 2 and 5 stocks in the sector, compared to 22 in the iShares MSCI China ETF.

Fund Activity & Style Trends

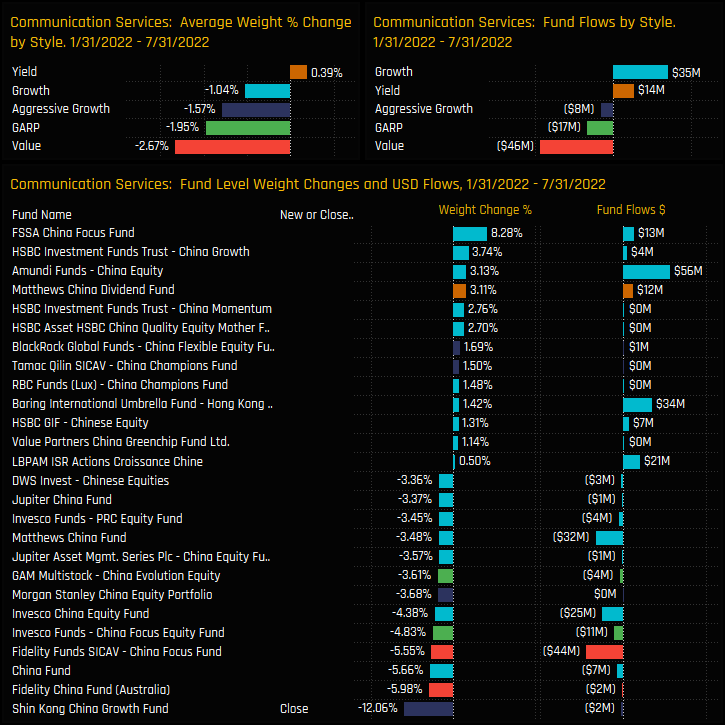

Fund holding changes over the last 6-months show allocations falling for all Style groups except for Yield, though activity wasn’t all one-way on a fund level. The larger changes in fund weight were on the sell side, led by Shin Kong China Growth (-12.06%) and Fidelity China (-5.98%), whilst FSSA China Focus (+8.28%) saw the largest increase.

The charts below show the average Communication Services weights by Style, relative to the iShares MSCI China ETF. All Style groups are underweight and have been for the last decade, though there has been a changing of the order in recent years. Yield managers have climbed from the lowest to the highest allocators over the last 5-years, whilst Aggressive Growth managers have moved to the lowest.

Stock Holdings & Activity

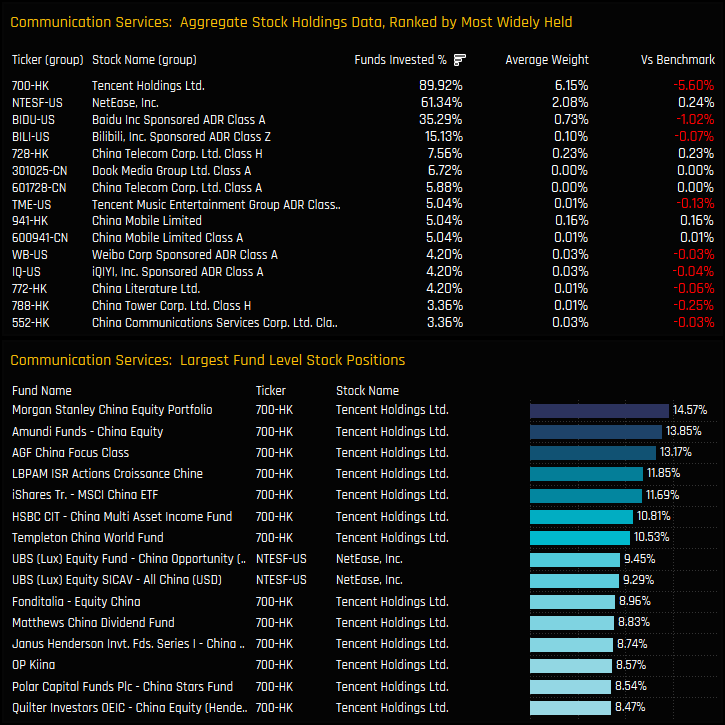

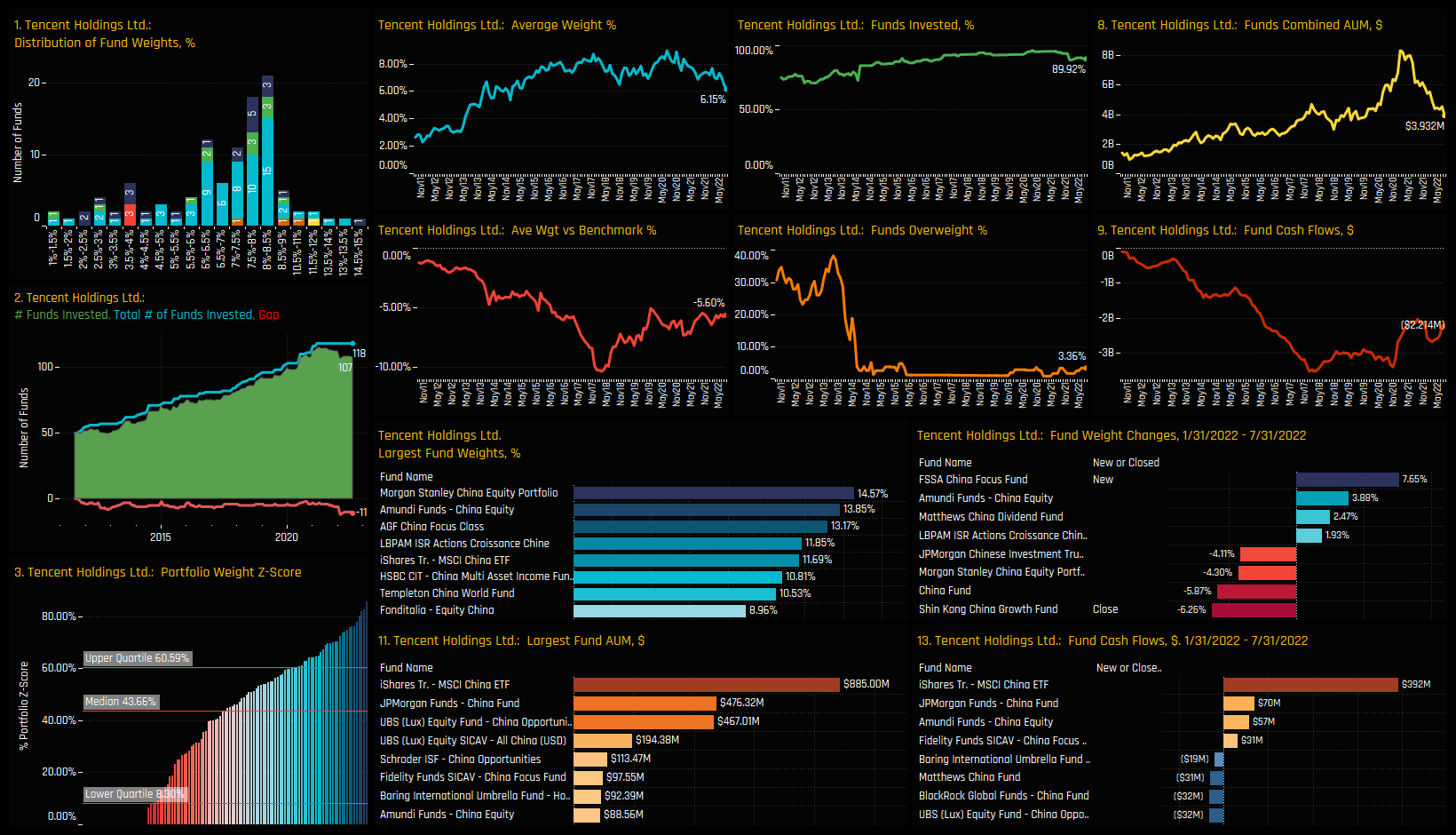

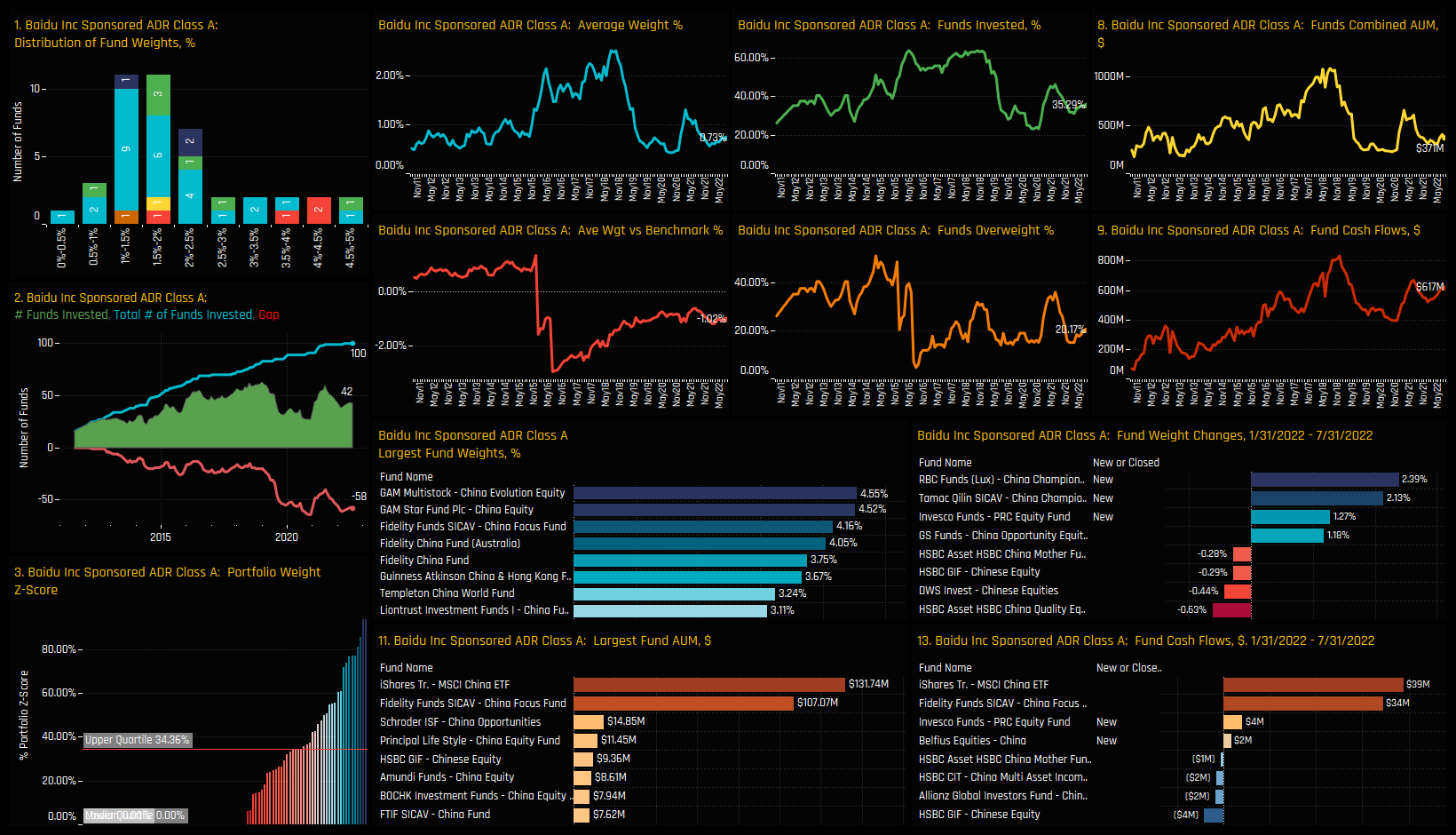

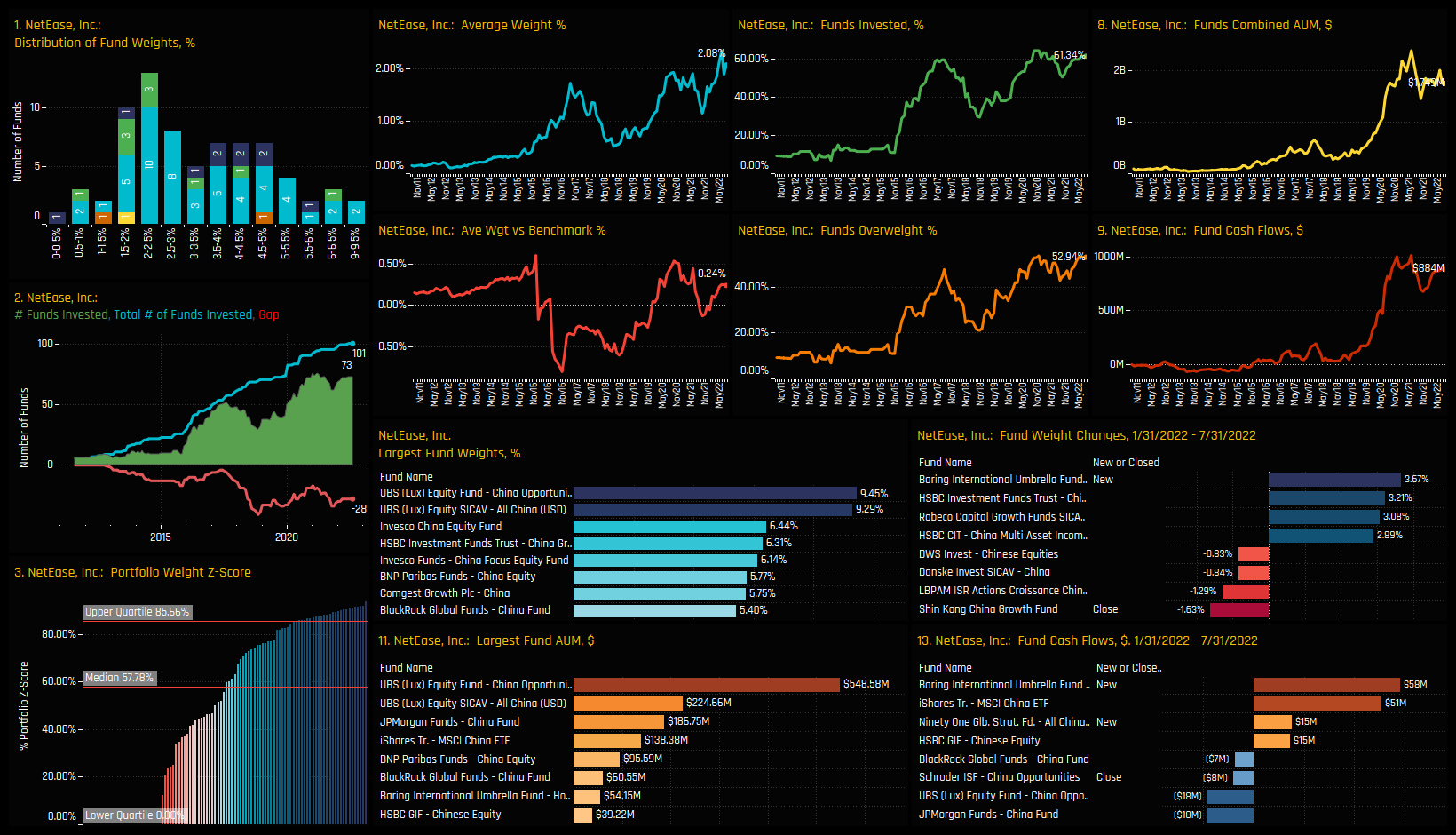

The sector is dominated by 3 stocks, which together account for 90% of total allocations. Tencent Holdings is the most widely held stock by a margin, owned by 89.9% of active China managers at an average weight of 6.15%. NetEase Inc and Baidu Inc form the second tier, with 61.3% and 35.3% of funds invested but after that ownership really drops off. Tencent is the key underweight compared to the MSCI China index, yet it is still held in high regard by China managers, accounting for 86 of the top 100 largest individual fund positions in the sector.

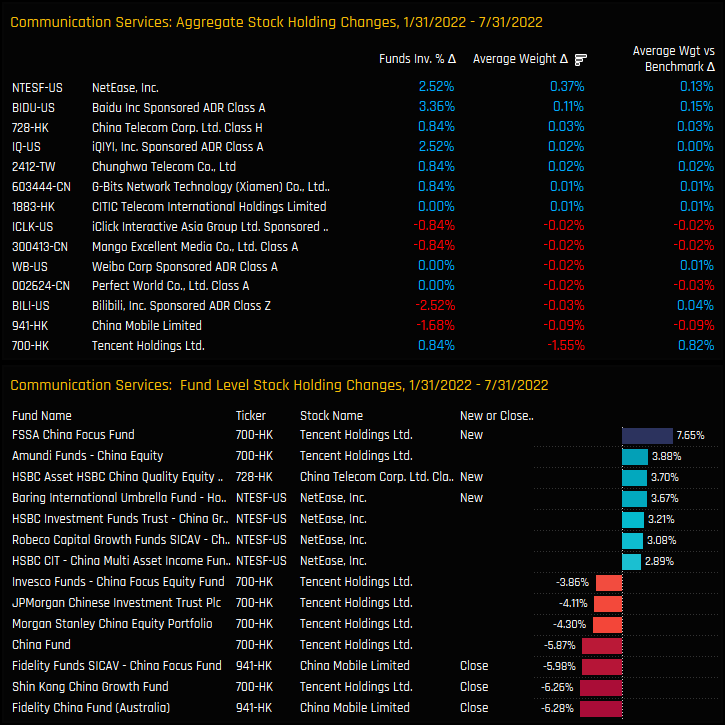

Changes over the last 6-months highlight the effect that Tencent Holdings has had on the overall sector decline. Average weights in Tencent declined by -1.55% over the period, though this wasn’t driven by a mass exodus in the name. In fact, despite an excess of sellers over buyers, outright ownership actually increased by 0.83% over the period. Outside of Tencent, managers cut exposure to Bilibili Inc and China Mobile and increased ownership in NetEase Inc and Baidu Inc.

Conclusions

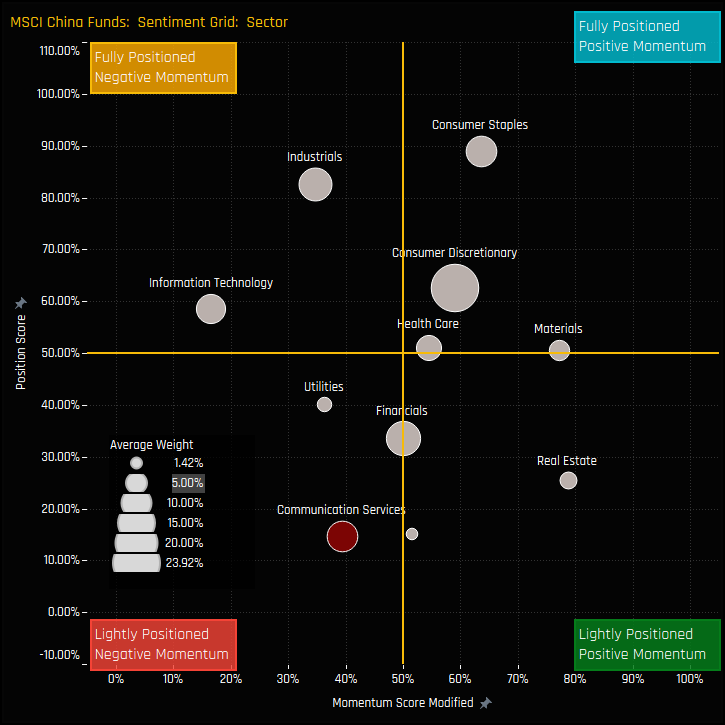

Sentiment in the Communication Services sector is close to an all-time low. The chart to the right shows where current positioning in each China sector sits versus history going back to 2011 on a scale of 0-100% (y-axis), against a measure of fund activity for each sector between 01/31/2022 and 07/31/2022 (x-axis). Positioning is the lowest of all sectors and momentum is what we might call apathetic.

The fact that active China funds are sticking with Tencent through this period of underperformance is encouraging, in addition to the increased ownership levels in key holdings Netease Inc and Baidu Inc. Rather than an outright exodus, it feels like active China managers are riding out the storm.

See below for more ownership information on Tencent, Baidu and NetEase. Please click on the link below for the extended report on Communication Services exposure among active MSCI China funds.

Click on the link below for the latest data report on Communication Services positioning among active China funds.

For more analysis, data or information on active investor positioning in your market, please get in touch with me on steven.holden@copleyfundresearch.com

{kind=link}