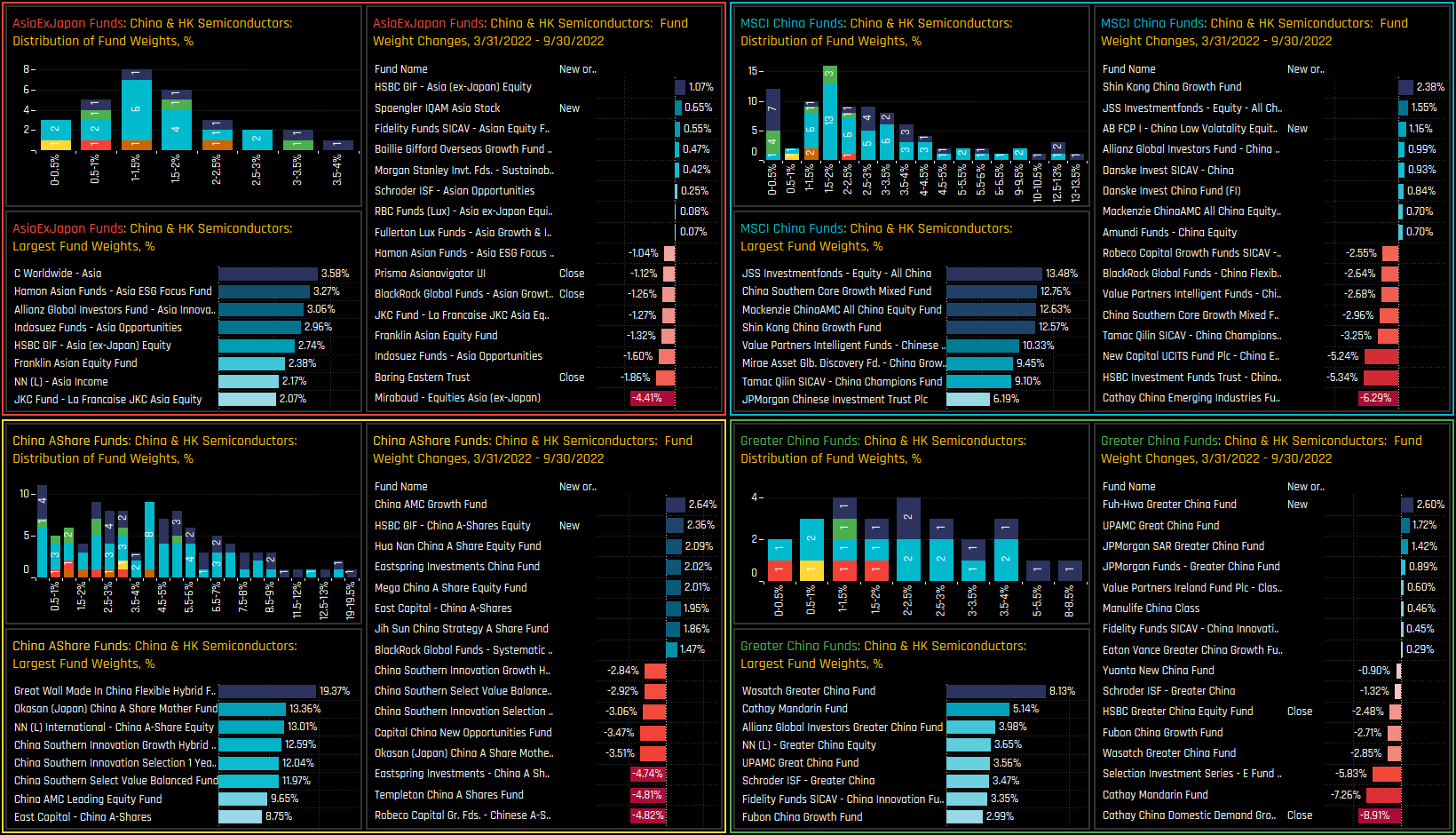

92 Asia Ex-Japan Funds, AUM $52bn, 115 China A-Share Funds, AUM $57bn, 117 MSCI China Funds, AUM $44bn, 45 Greater China Funds, AUM $15bn

China Semiconductors

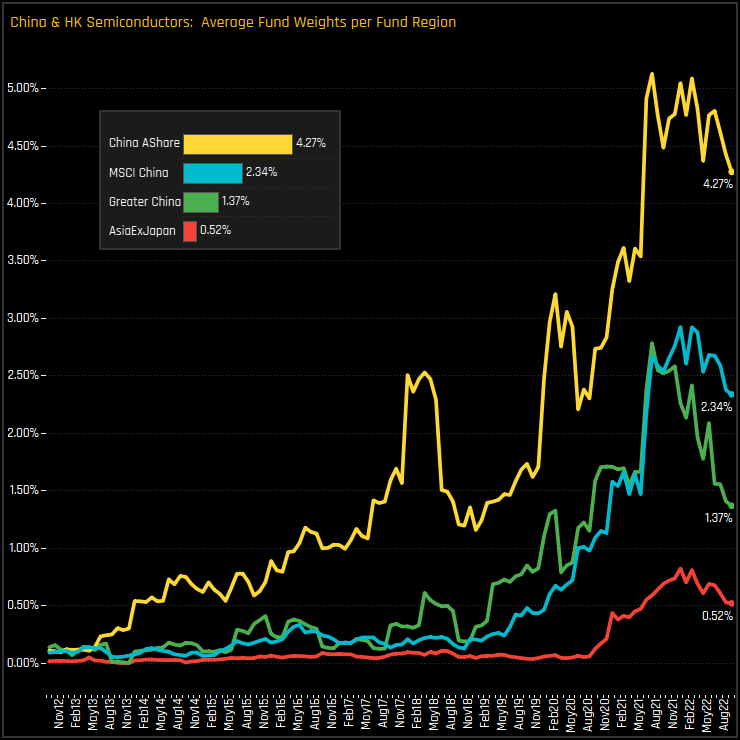

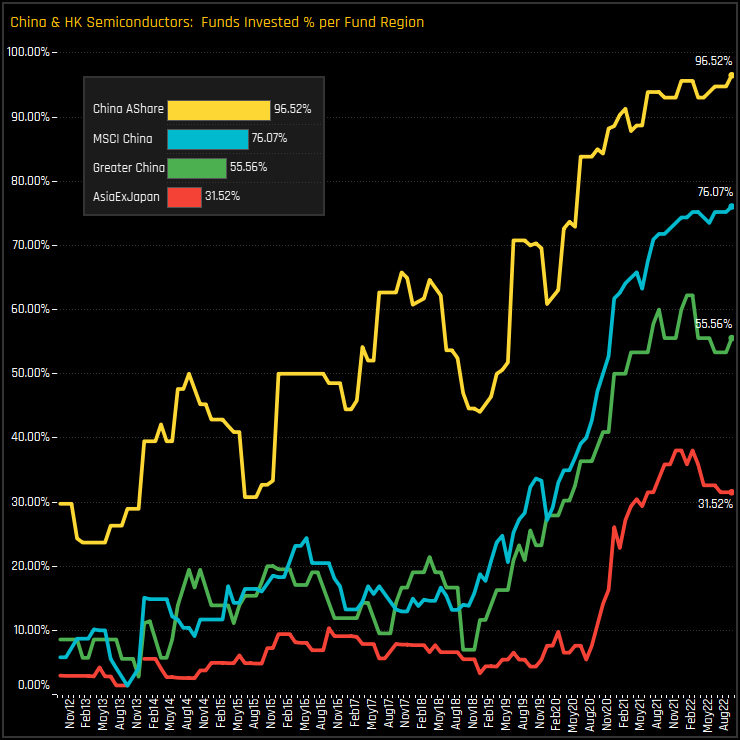

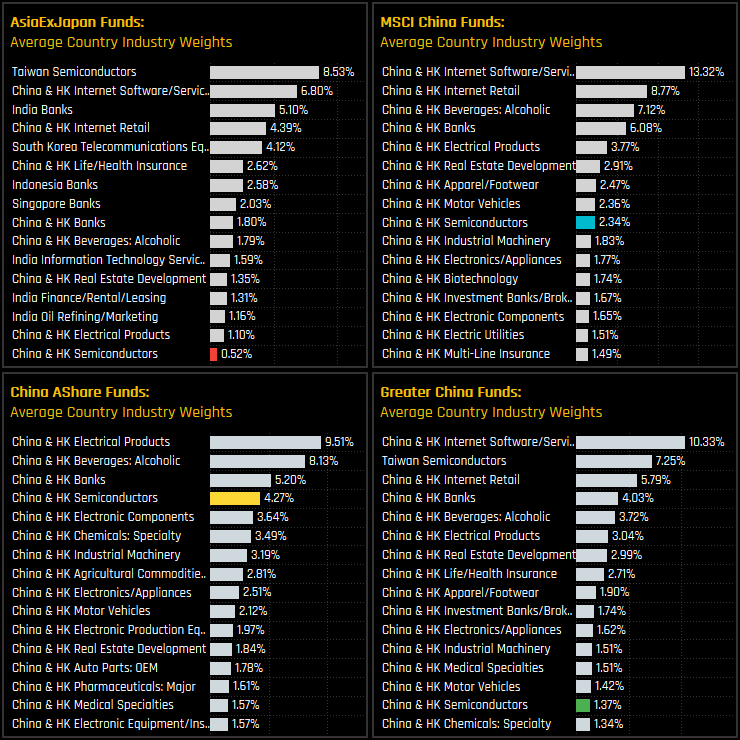

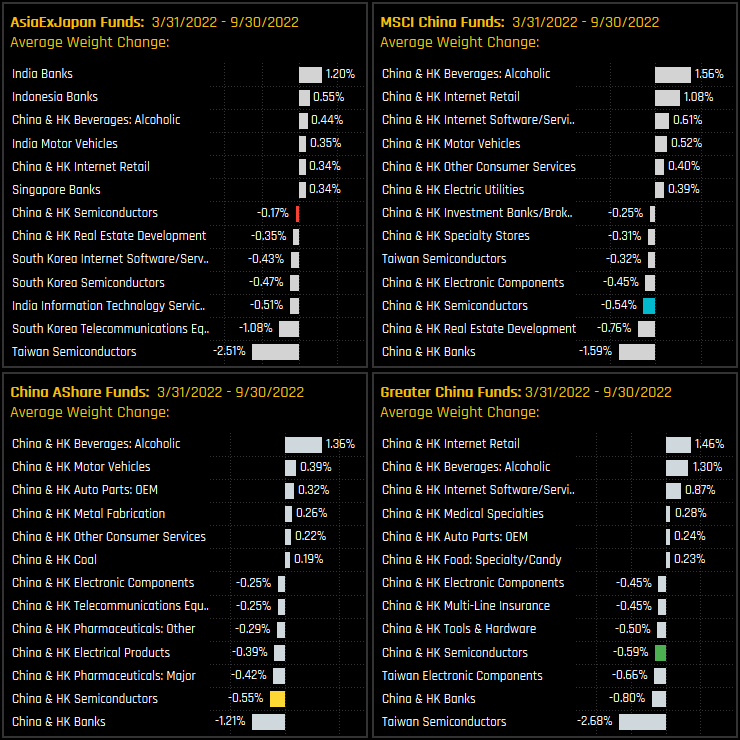

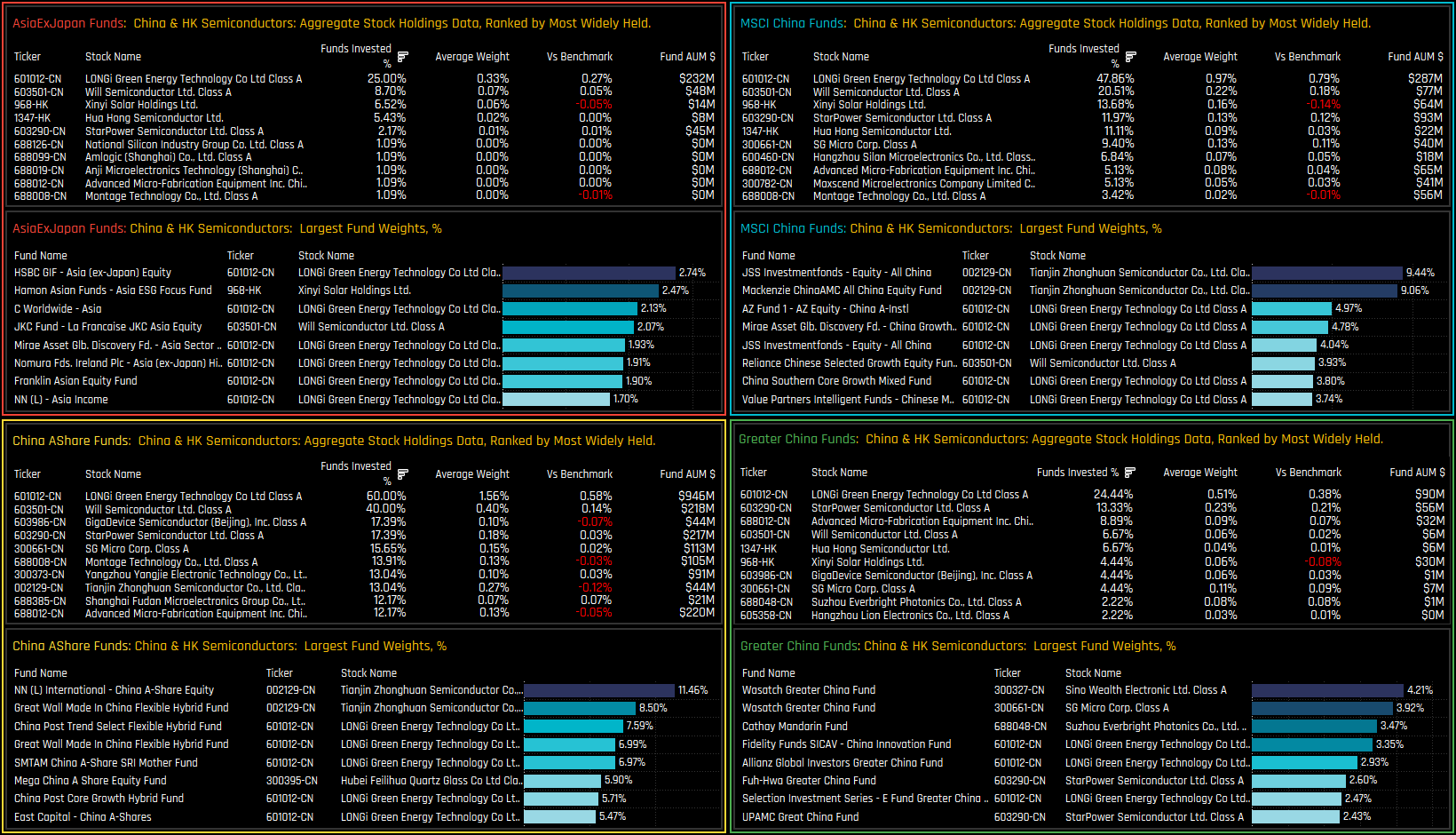

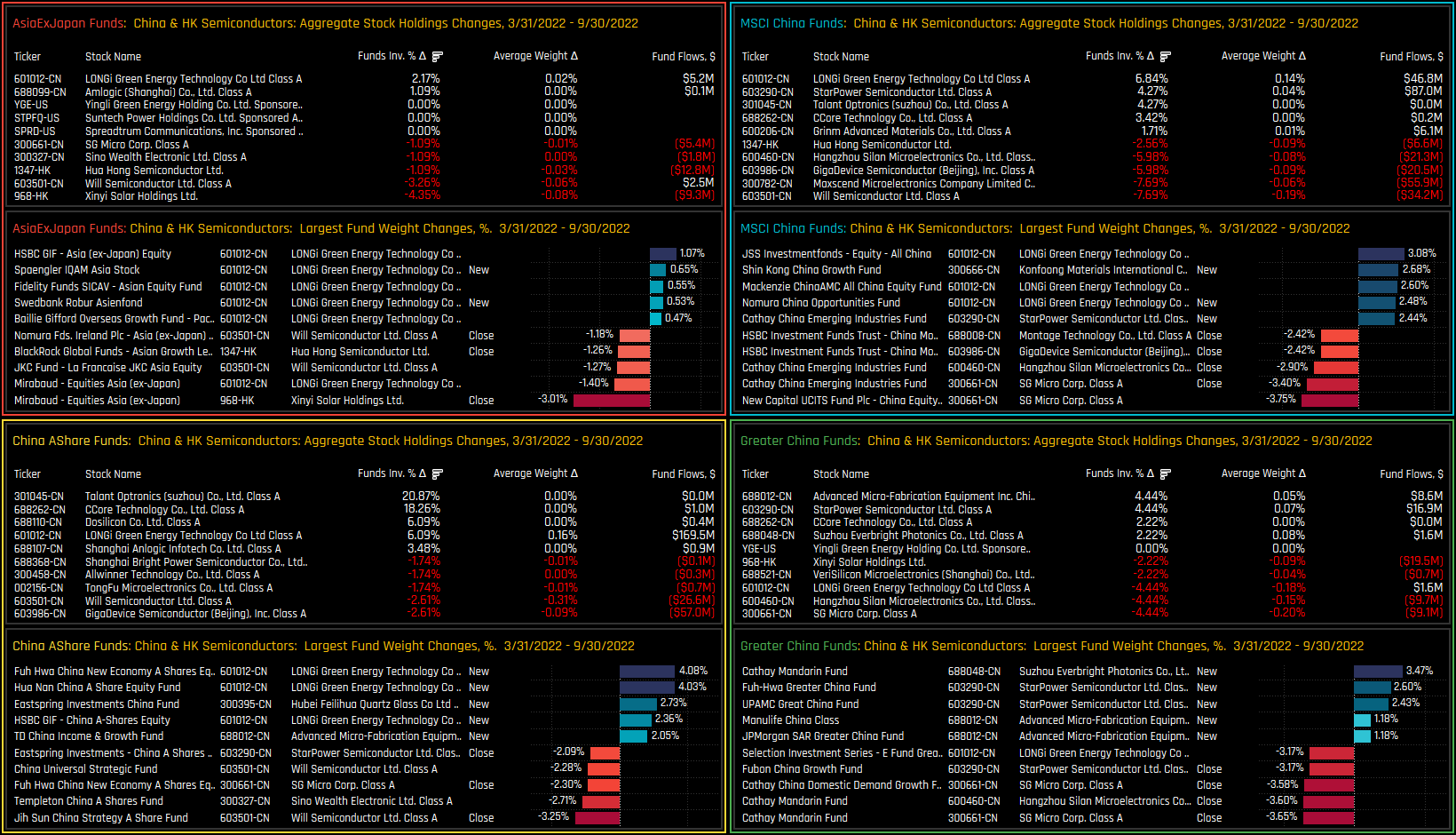

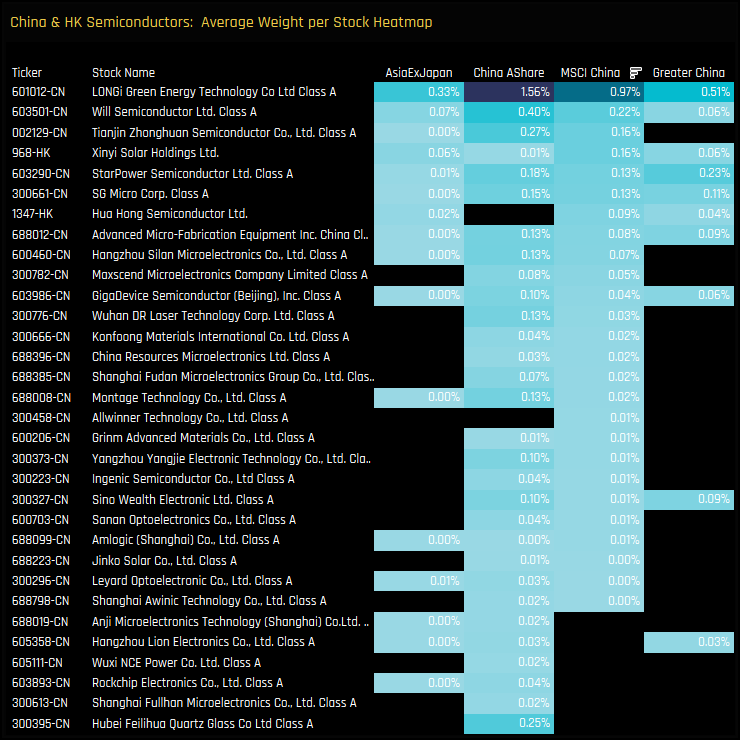

With US sanctions hitting Chinese domestic Semiconductor stocks this week, we analyse allocations in the China & HK Semiconductor Industry group among Asia Ex-Japan, MSCI China, China A-Share and Greater China actively managed equity funds. Without the distraction of Taiwan technology or HK listed internet stocks, China A-Share funds are the most heavily exposed, whilst Asia Ex-Japan and Greater China funds have curtailed investment in recent months. On a stock level, LONGi Green Energy Technology is the high conviction holding by quite a margin, whilst Will Semiconductors has started to see closures from a number of managers. On the whole though, China & HK Semiconductor stocks do not represent a significant risk for the majority of managers in our analysis.

{kind=link}