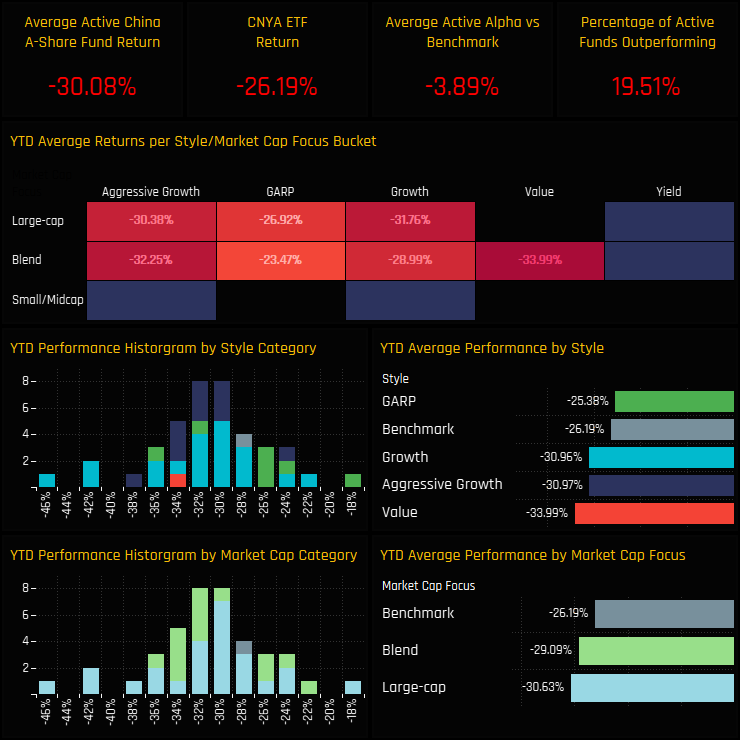

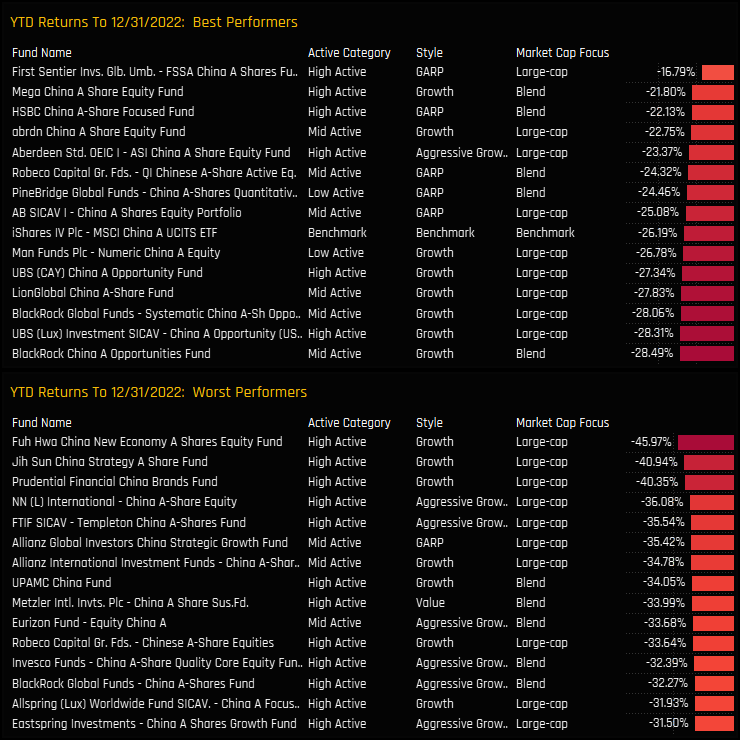

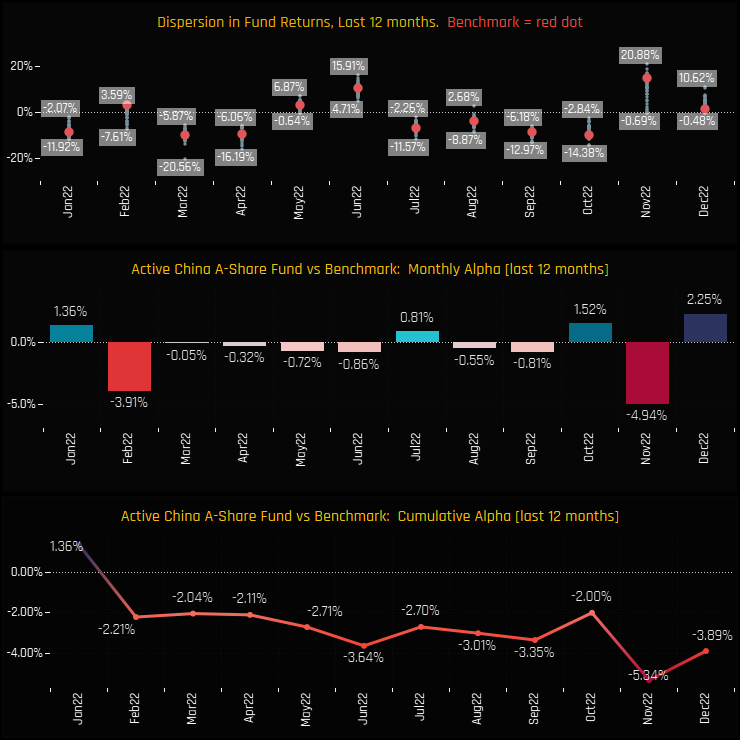

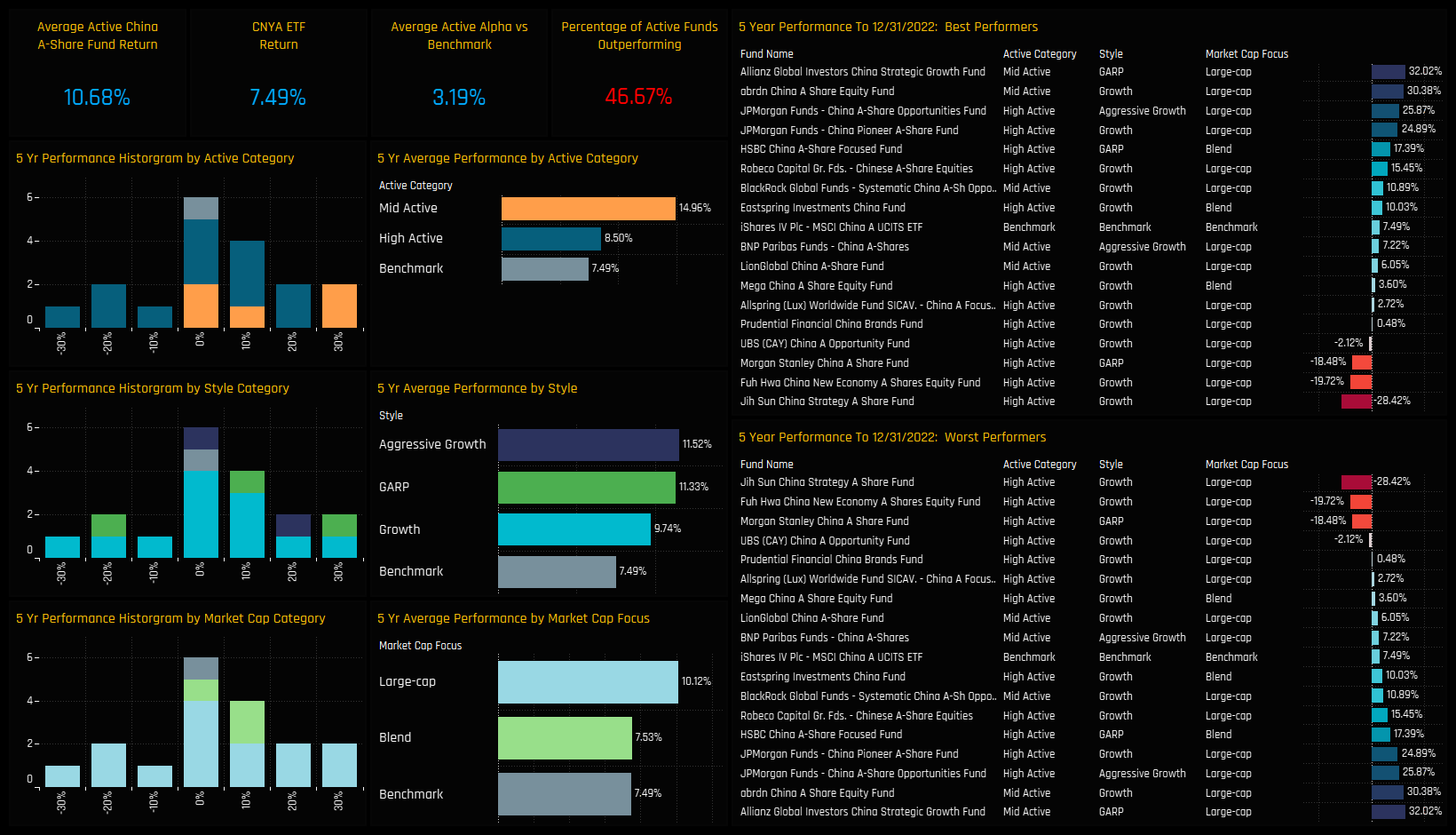

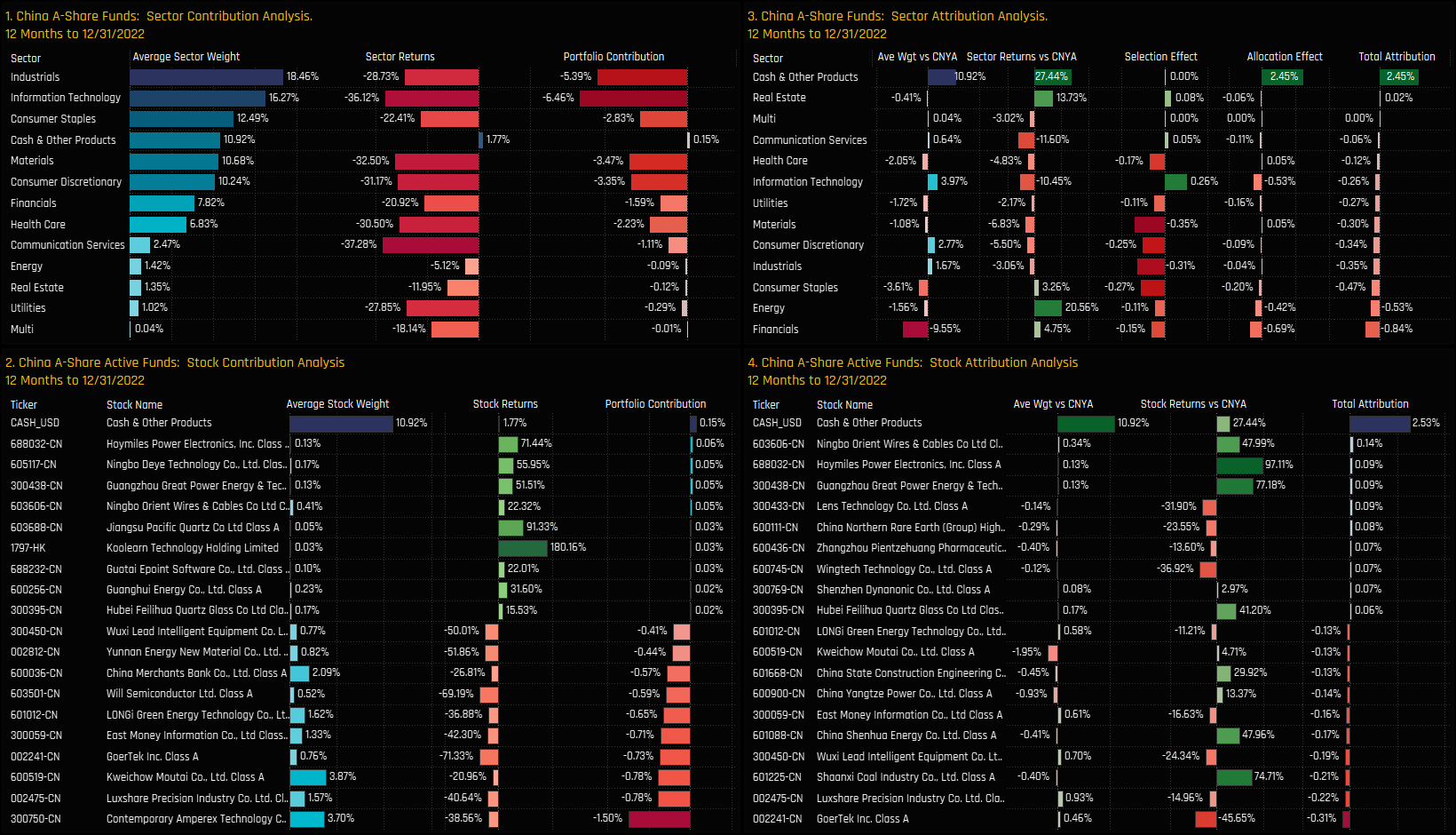

China A-Share managers had a difficult 2022. Average returns of -30.08% fell short of the iShares MSCI China A-Share ETF by -3.89%, with more than 80% of funds underperforming. GARP funds stand out as the best performers and the only Style group to outperform the benchmark, on average.

{kind=link}