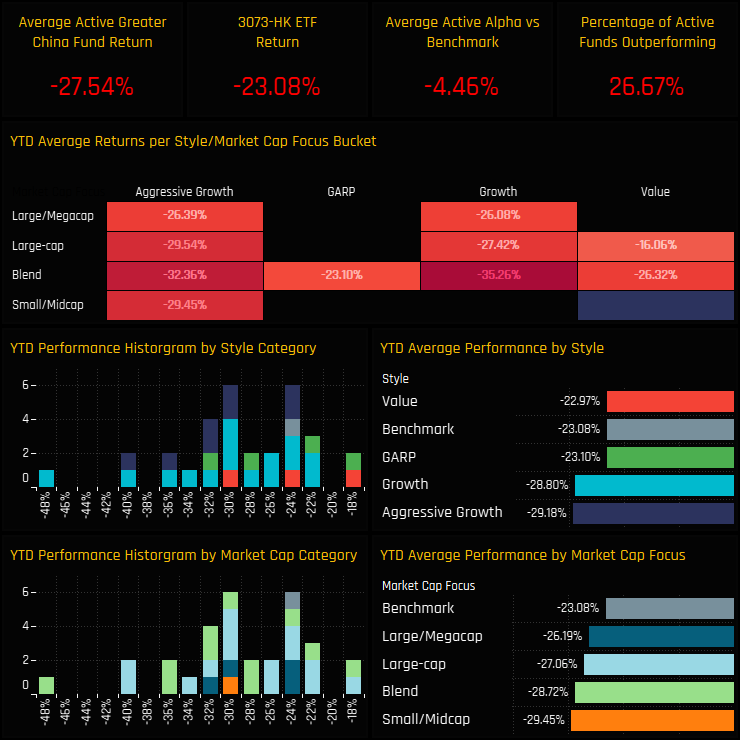

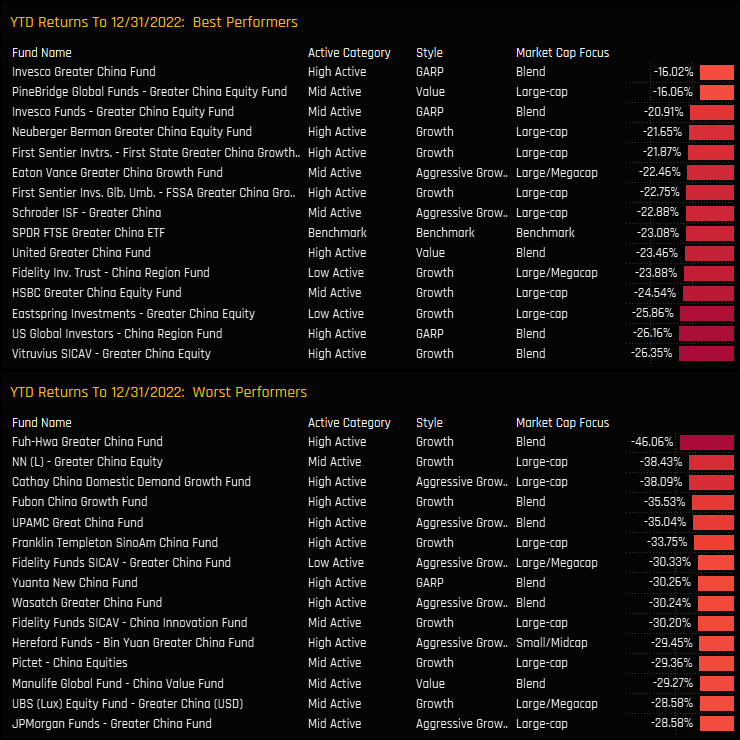

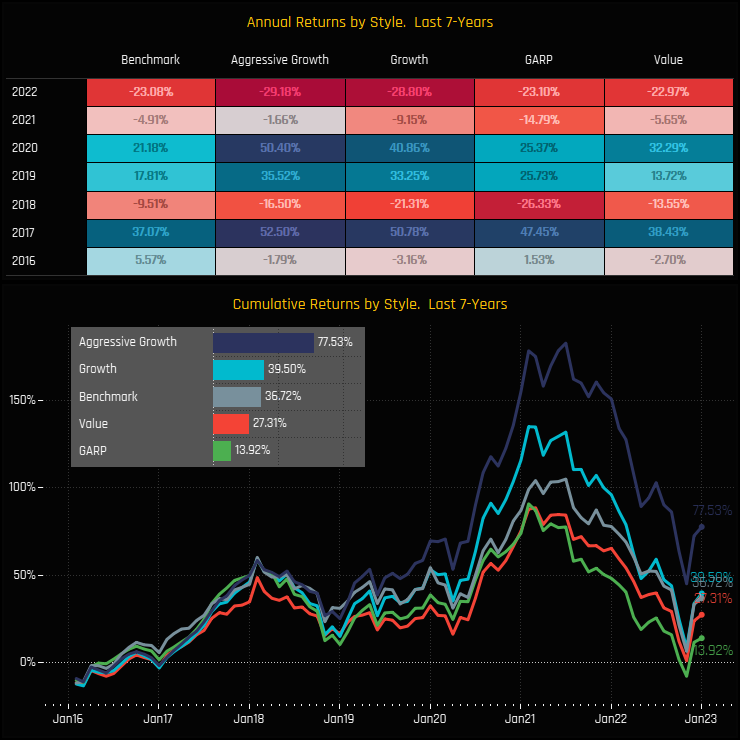

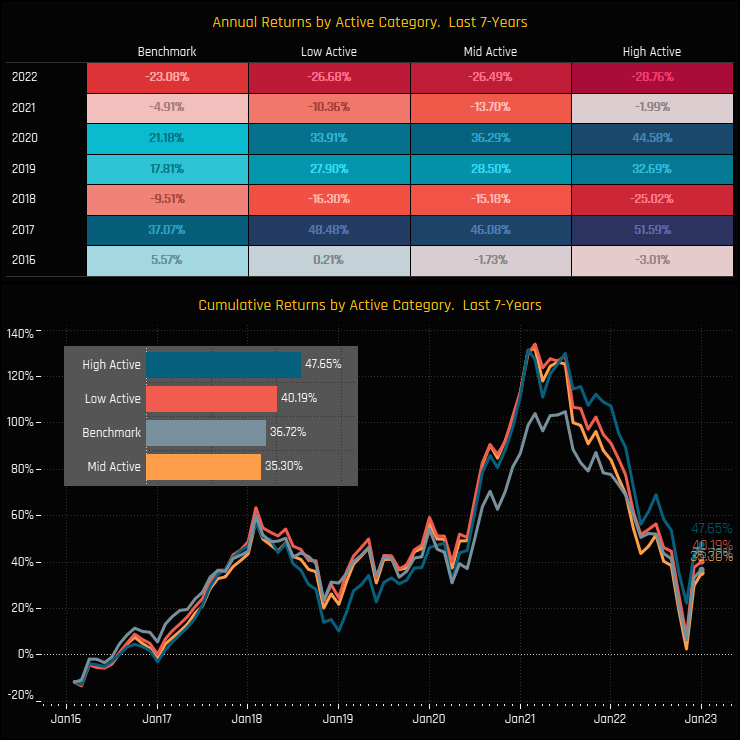

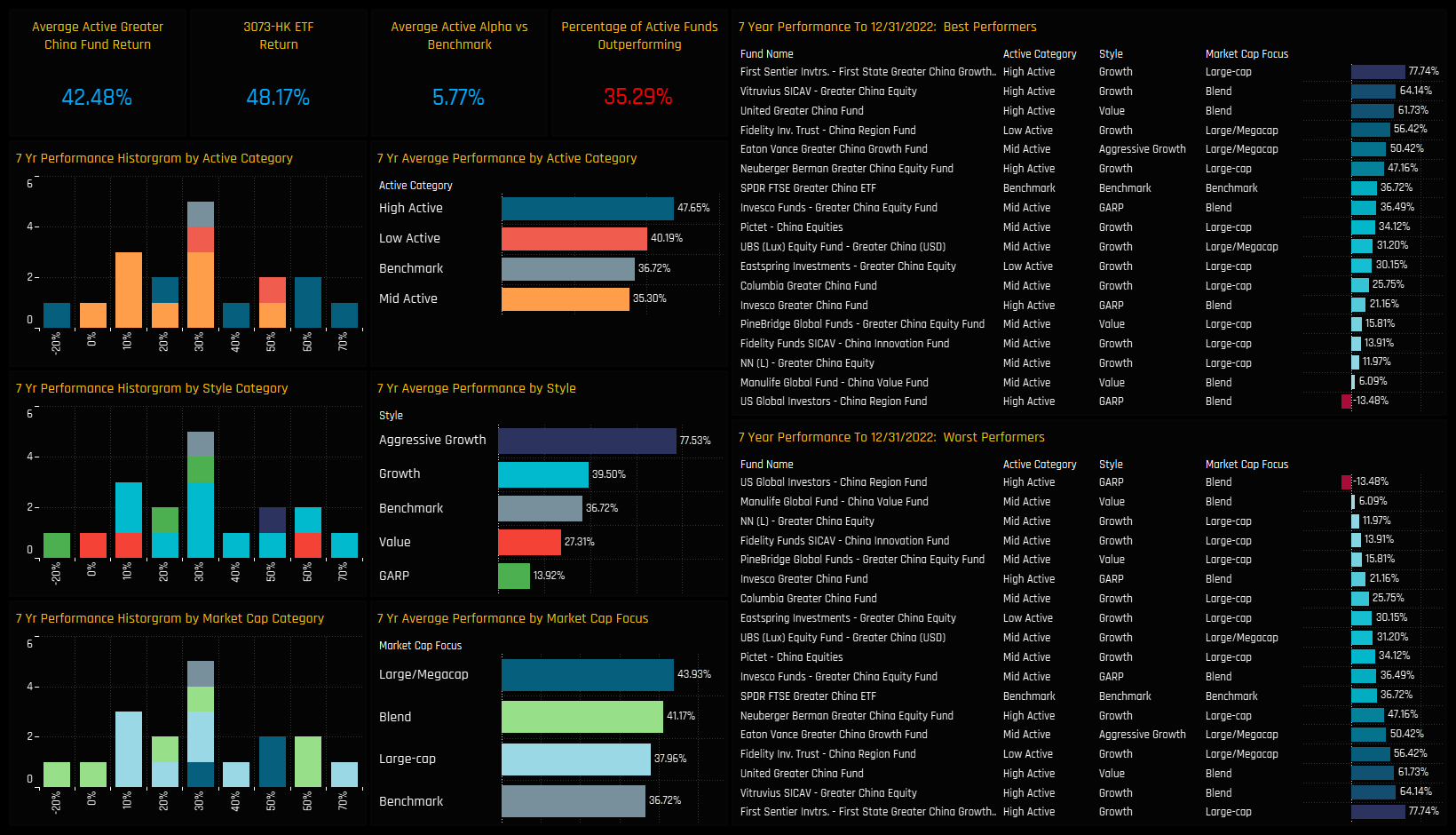

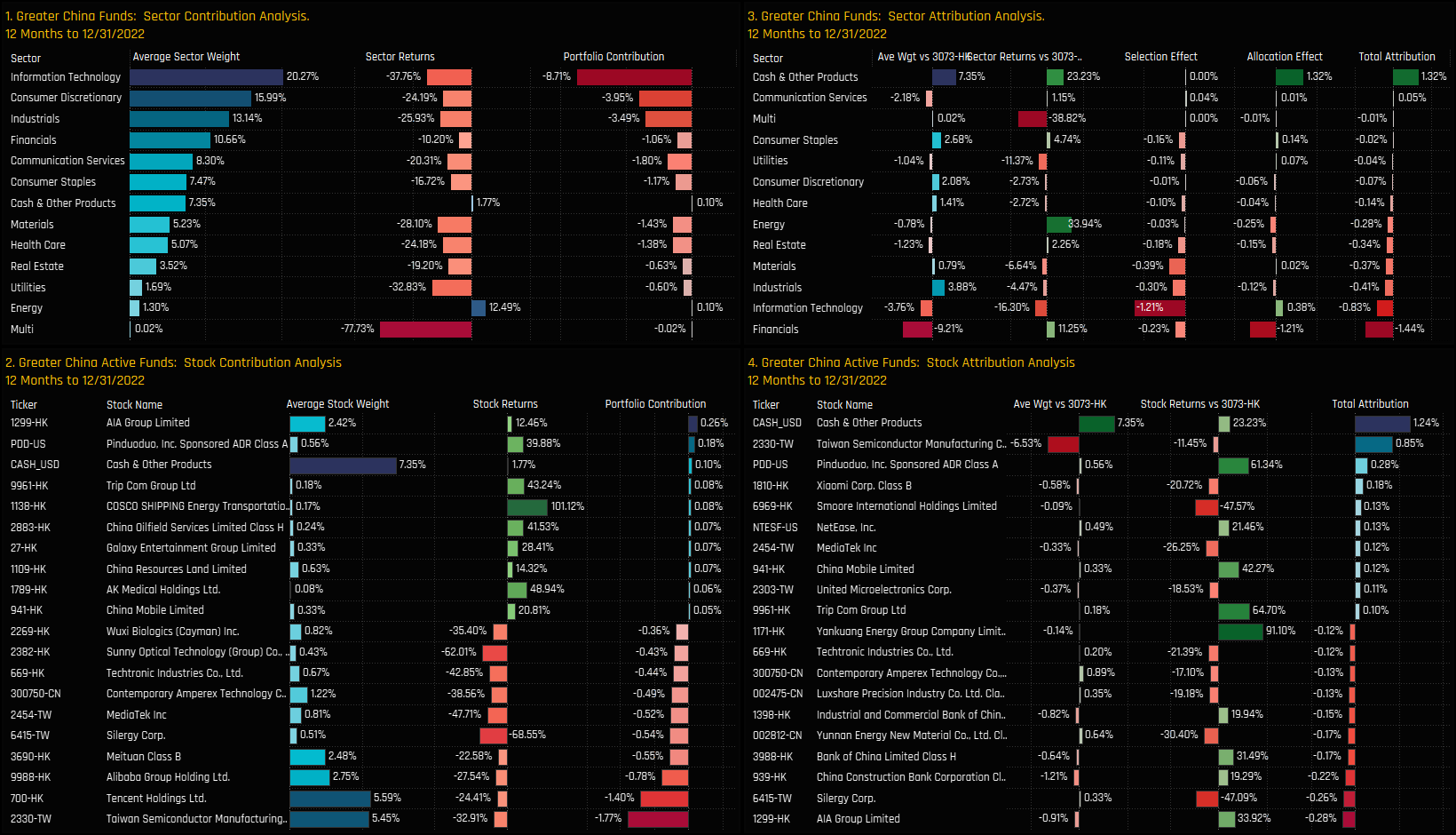

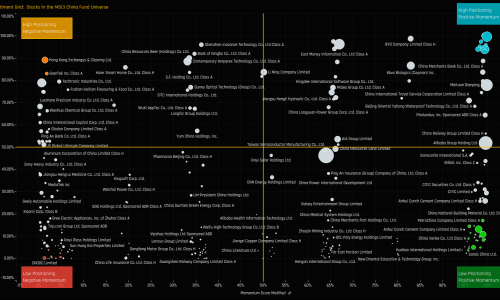

In line with both MSCI China and China A-Share active funds, Greater China managers had a dreadful 2022. Average returns of -27.54% fell some way short of the SPDRs FTSE Greater China ETF of -23.08%, with nearly 3/4 of funds underperforming the benchmark. Value and GARP Funds had the advantage over Growth and Aggressive Growth, and Large-cap beat Small/Midcap and Blend funds over the course of the year.

{kind=link}