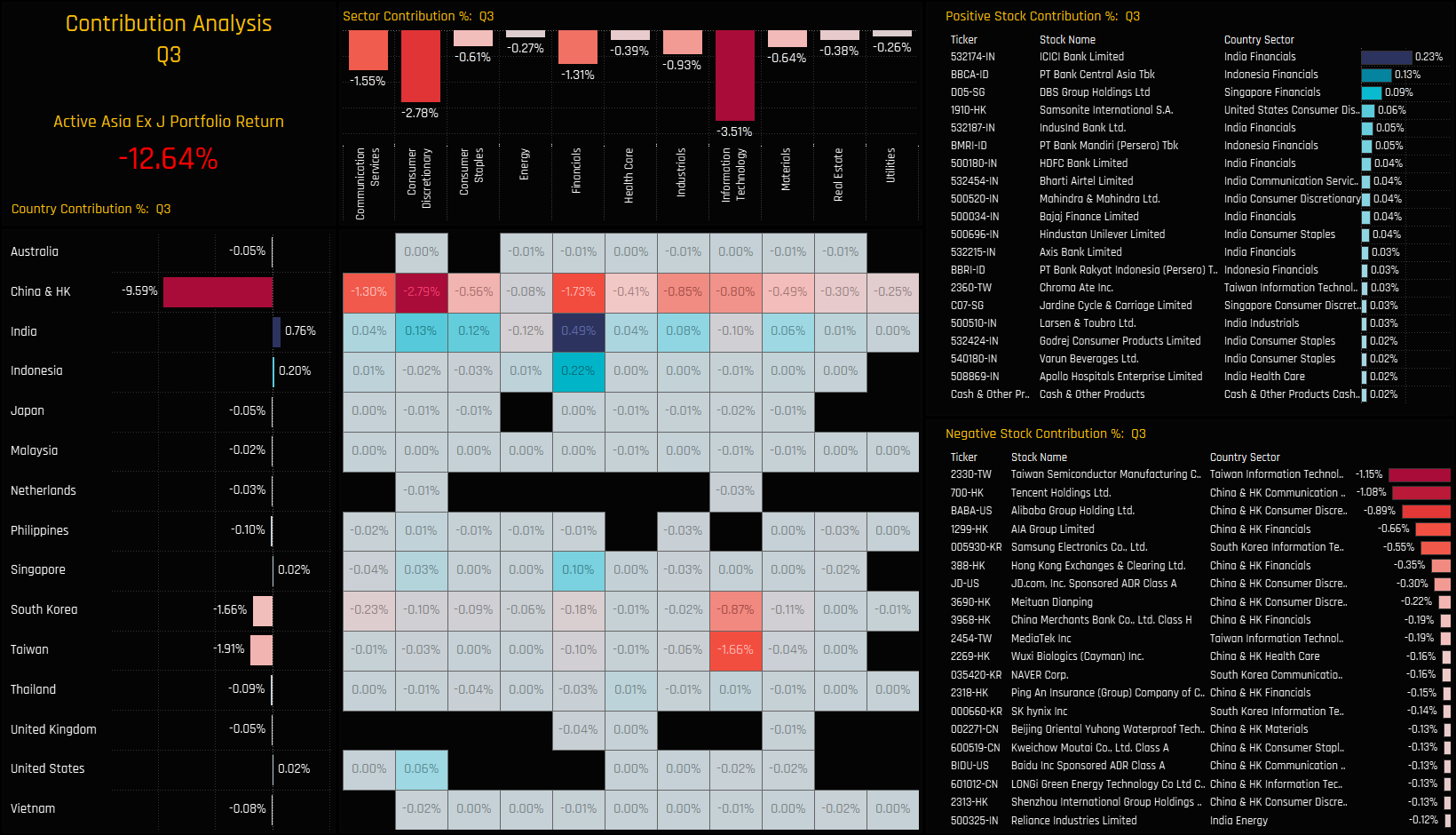

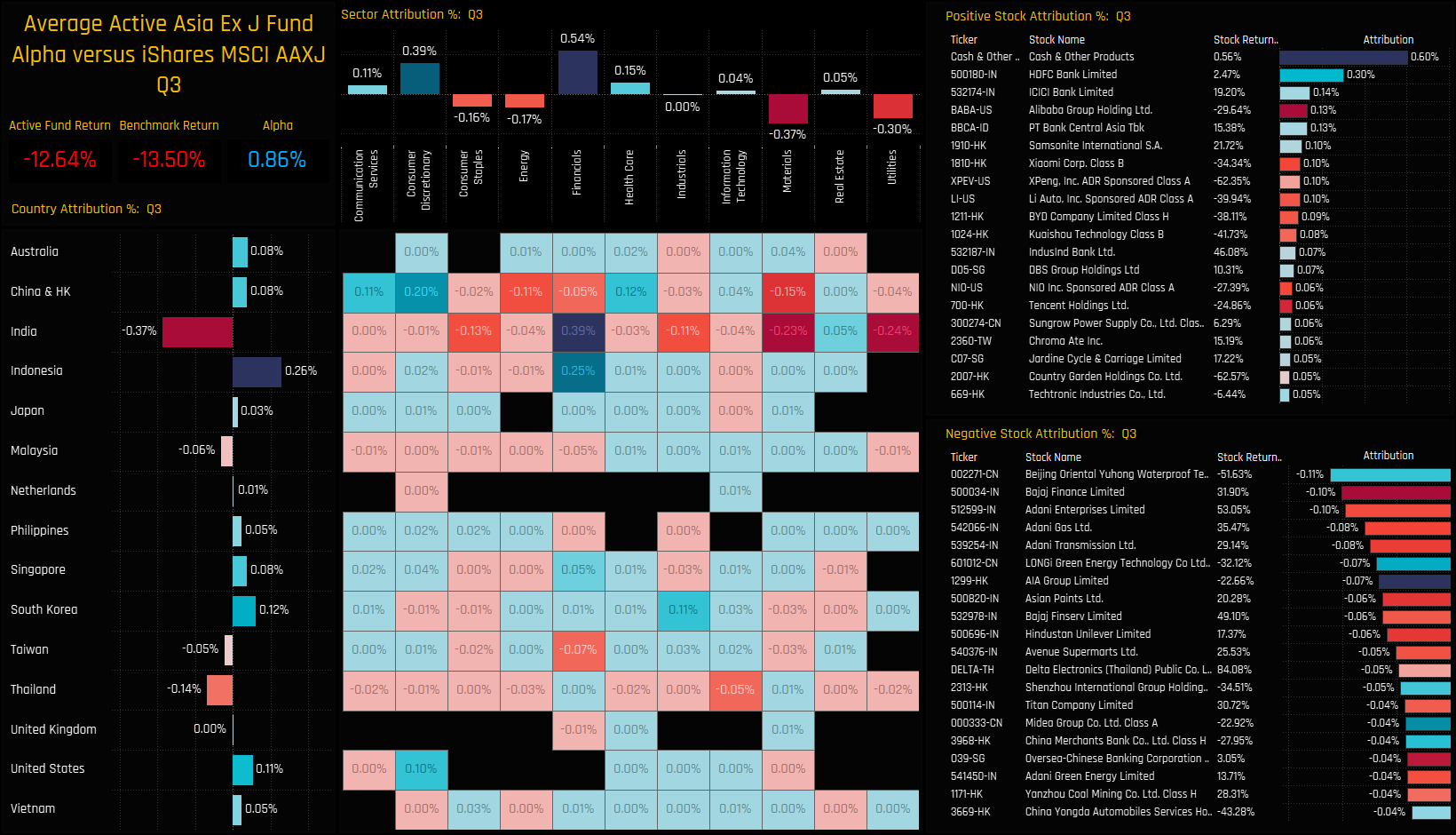

Marrying the performance of each portfolio component with the weight in the active portfolio provides the contribution of each country, sector and stock to the overall quarterly performance of -12.64%. China & HK alone accounts for -9.59% of that return over the quarter, with particular negatives coming from Consumer Discretionary (Alibaba, JD.Com), Communication Services (Tencent, Baidu), and Financials (AIA Group, HK Exchanges). Taiwan Technology (TSMC, MediaTek) and South Korean Tech (Samsung Electronics, SK Hynix) also dragged on overall returns. Financials in India and Indonesia provided some respite on the upside, led by ICICI Bank Limited and PT Bank Central Asia.

{kind=link}