Ford becomes one of the most unloved stocks in the USA as active funds close out positions.

Time-Series and Autos Positioning

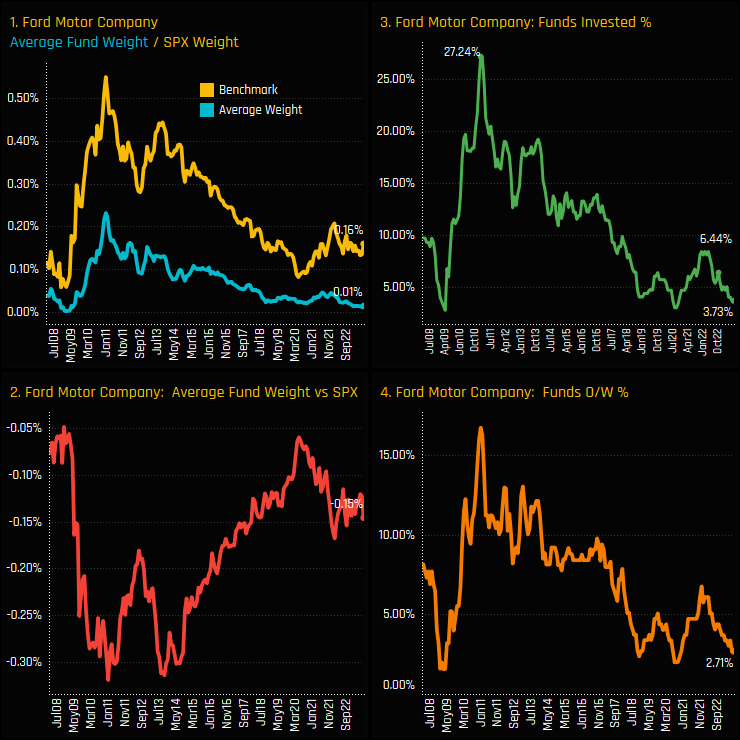

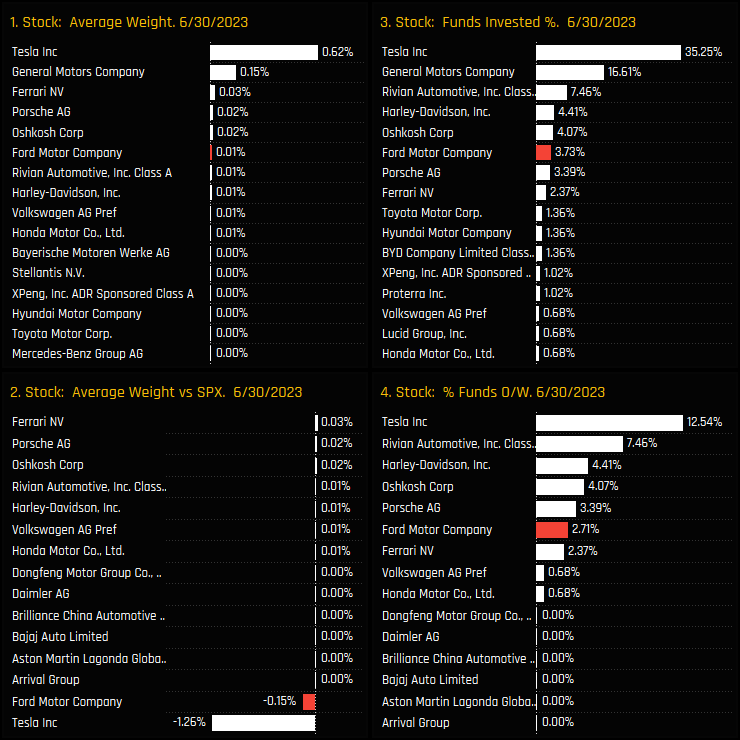

Ford Motor Company is owned by just 11, or 3.7% of the 295 US active funds in our analysis. Chart 3 below shows the decline in the percentage of funds invested in Ford, with peak ownership of 27.24% occurring in late 2010 and today’s level close to the lowest on record. Average fund weights have fallen to just 0.01%, or underweight the S&P 500 weight by -.015%).

Versus Auto peers, Ford Motor Company is now the 6th most widely held Auto stock among US active investors. The most widely held is Telsa Inc, owned by 35.25% of funds at an average weight of 0.62%. Both GM, Rivian Automotive, Harley Davidson and Oshkosh Corp are all owned by more funds. Ford is the

Fund Activity & Latest Holdings

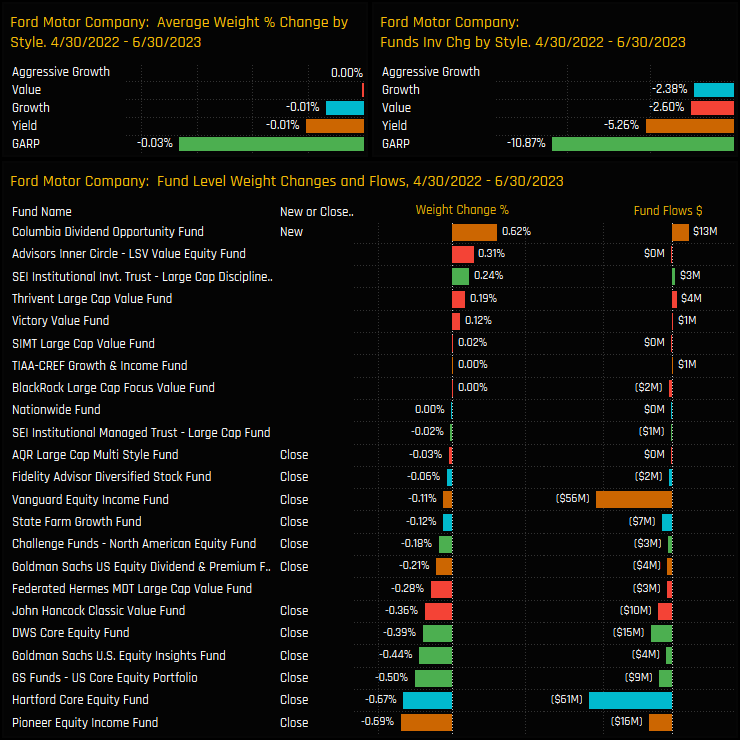

Since the most recent highs of April last year, fund activity has been overwhelmingly skewed to the sell-side. Closures were led by Pioneer Equity Income (-0.69%) and Hartford Core Equity (-0.67%), adding to a total of 12 funds who removed Ford from portfolios over the period.

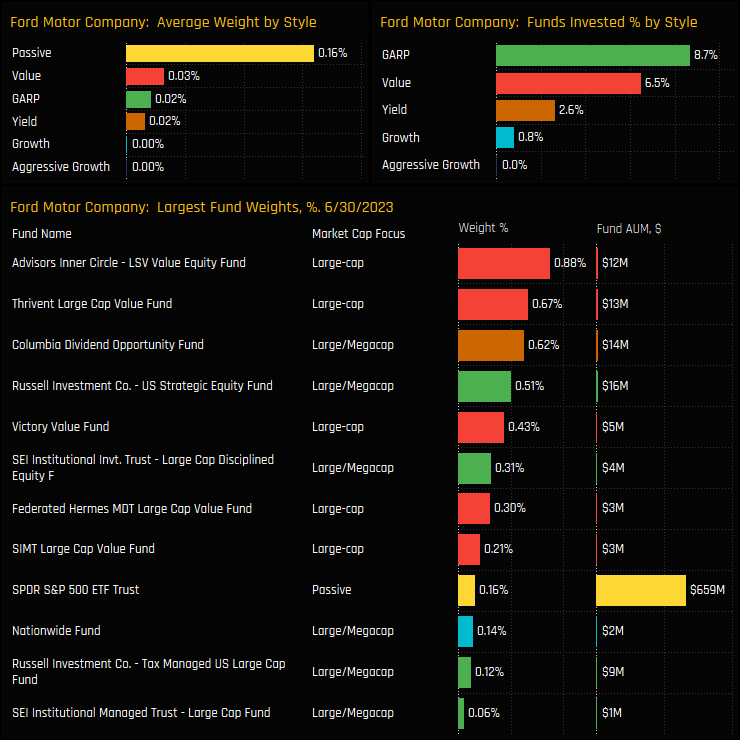

This leaves a small investor base for Ford among active US equity funds. Top holders are at the Value end of the spectrum and led by LSV Value and Thrivent Large Cap Value, but the truth is, Ford is a fringe portfolio holding for even the most bullish of US investors.

Underowned and Unloved

Ford now heads the unenviable list of ‘Únloved Stocks’ among active US investors. These stocks are not only held as net underweight positions compared to the S&P 500 index on average, but also by less than 5% of the 295 funds in our analysis. Very few want to own it, and the vast majority are happy to run the risk of Ford outperforming.

Click below for the full data report on Ford Motor Company among active US Equity Funds.

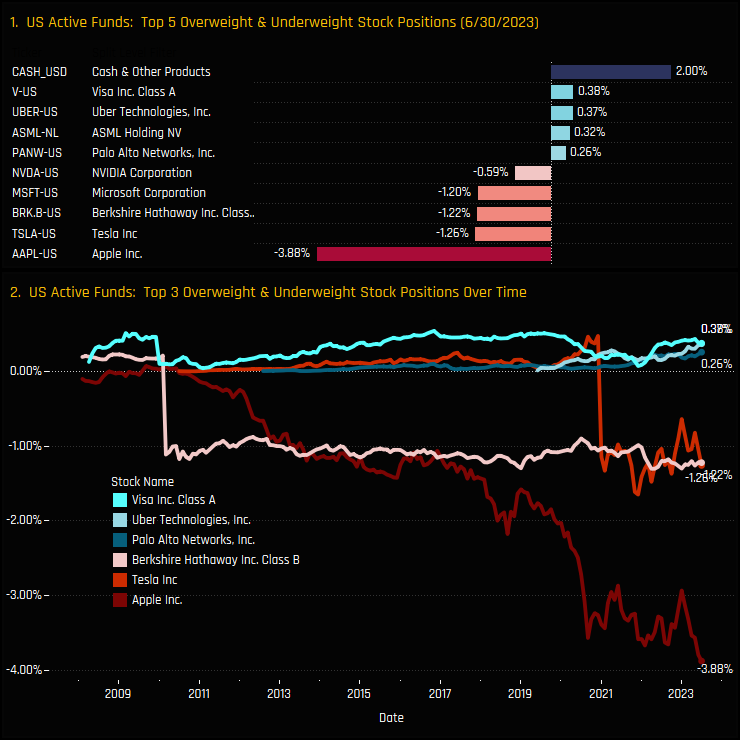

US Active Equity: Top Overweight & Underweight Stocks

Overweights in Visa offset by record underweights in Apple Inc.

Top overweights are in Cash, Visa and then non-benchmark stocks Uber Technologies, ASML Holdings and Palo Alto Networks.

US active funds are running massive underweights in Apple Inc, with average weights of 3.8% way below the S&P 500 weight of 7.7%. In fact, the -3.88% Apple underweight is the highest on record for US active funds. Other decent sized underweights are in Telsa, Berkshire Hathaway and Microsoft Corp.

Note the size difference between the largest underweights and the largest overweights. This is a fairly common set up among active investors across the regions we cover. A few large underweights in the top index names offset by a long tail of smaller overweights.

295 US Equity Funds, AUM $3.2tr

US Active Funds Ownership Report

Please click on the link below for the full data report on US active fund positioning

For more analysis, data or information on active investor positioning in your market, please get in touch with me on steven.holden@copleyfundresearch.com

{kind=link}