17 December

UK

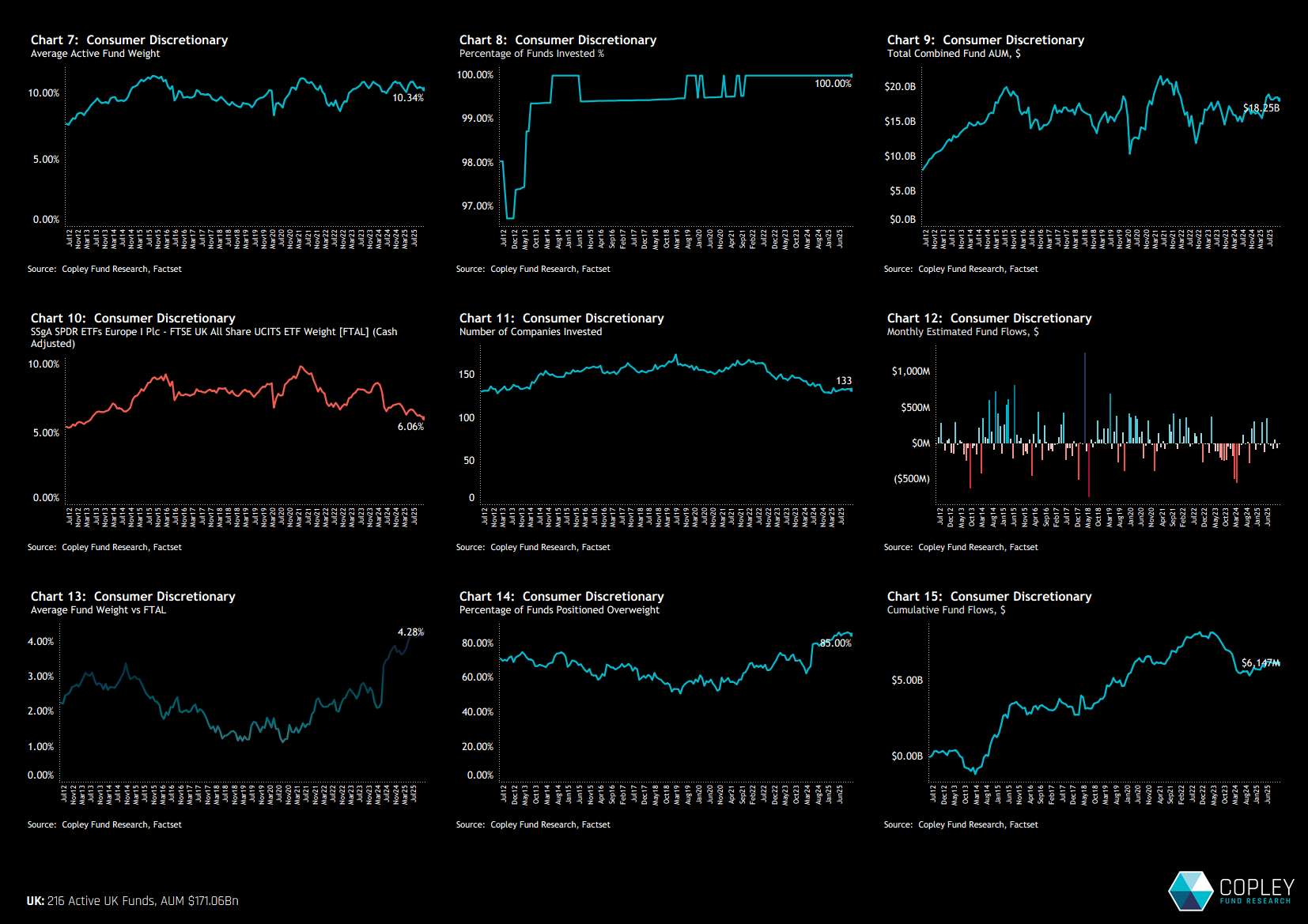

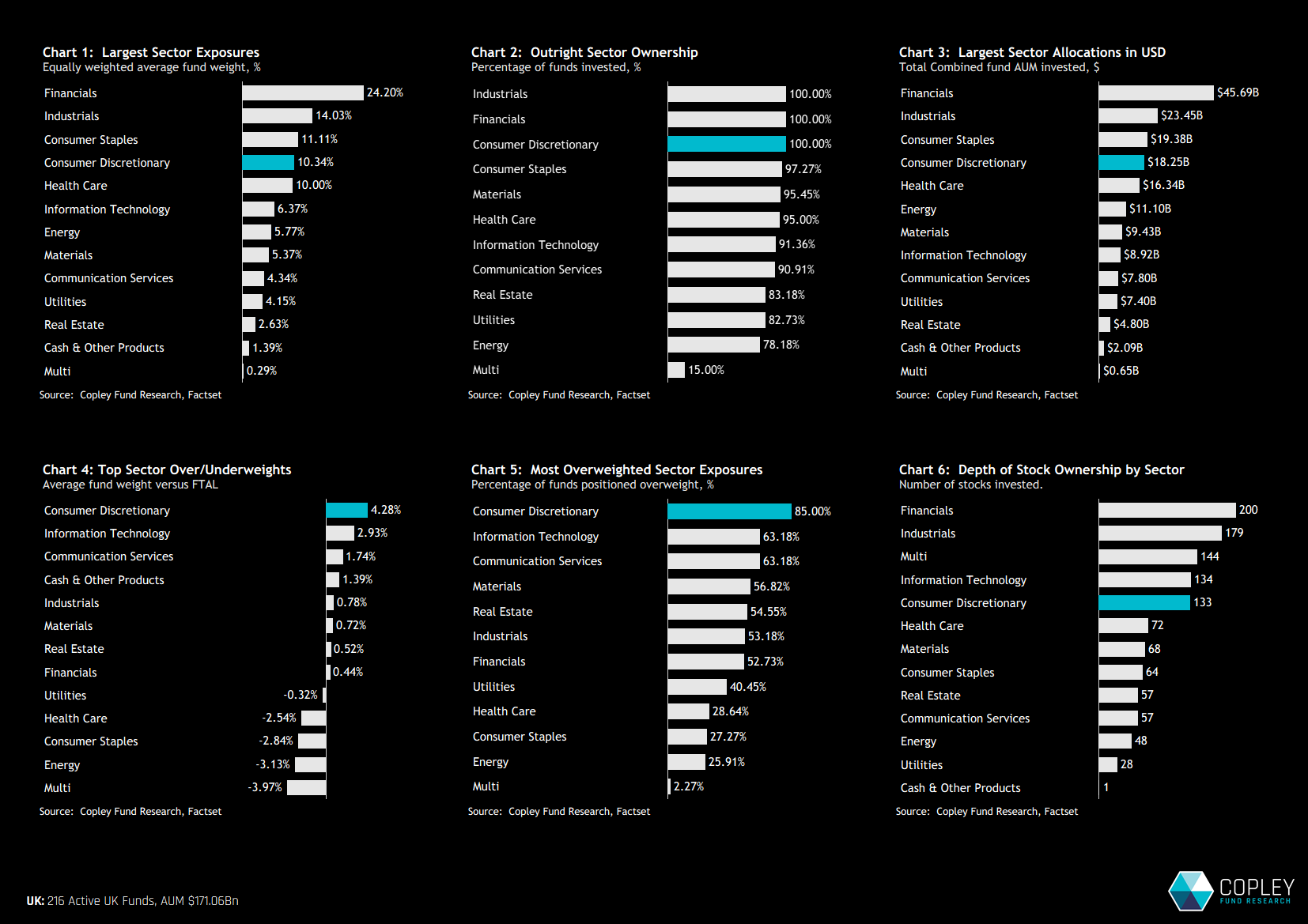

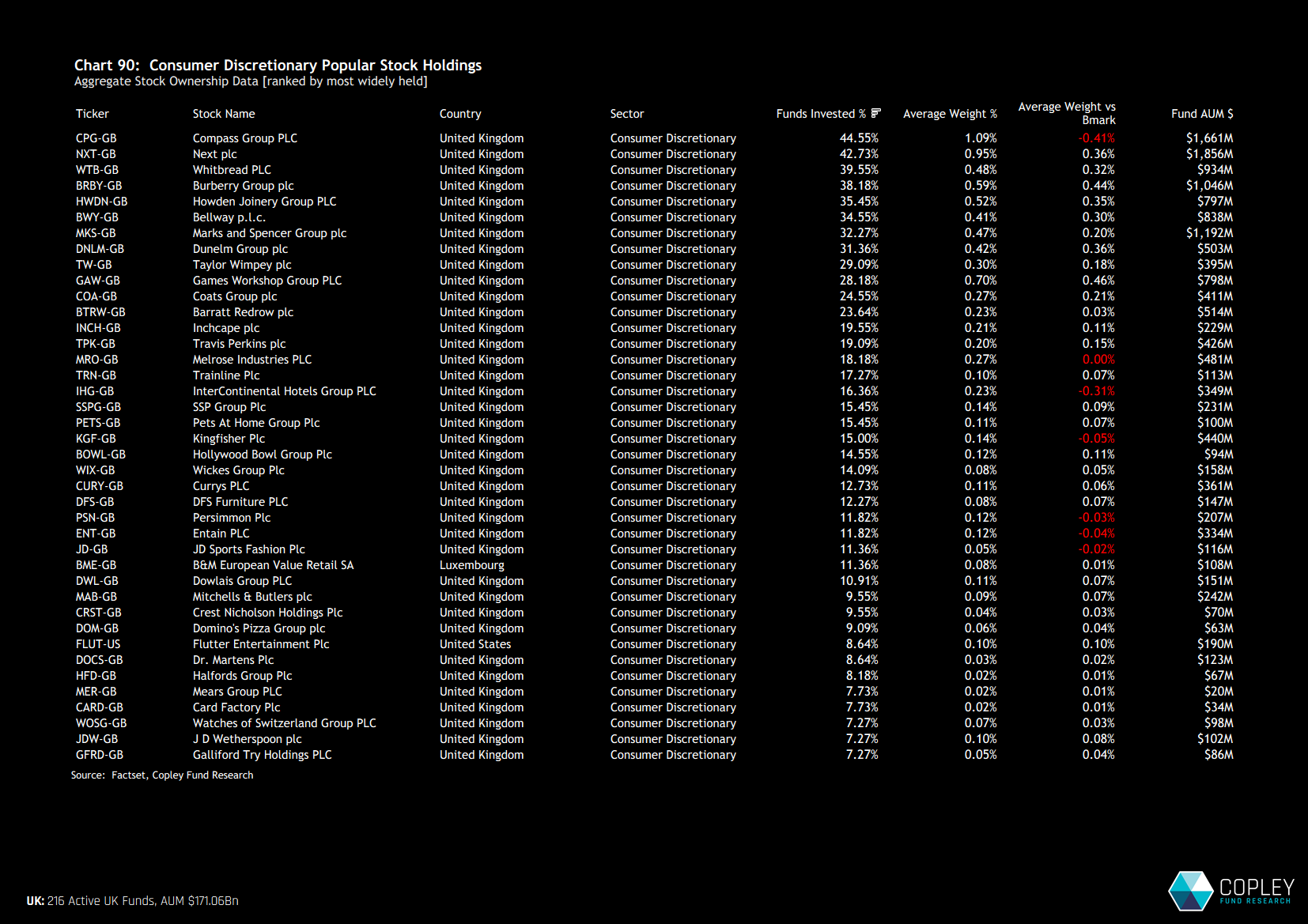

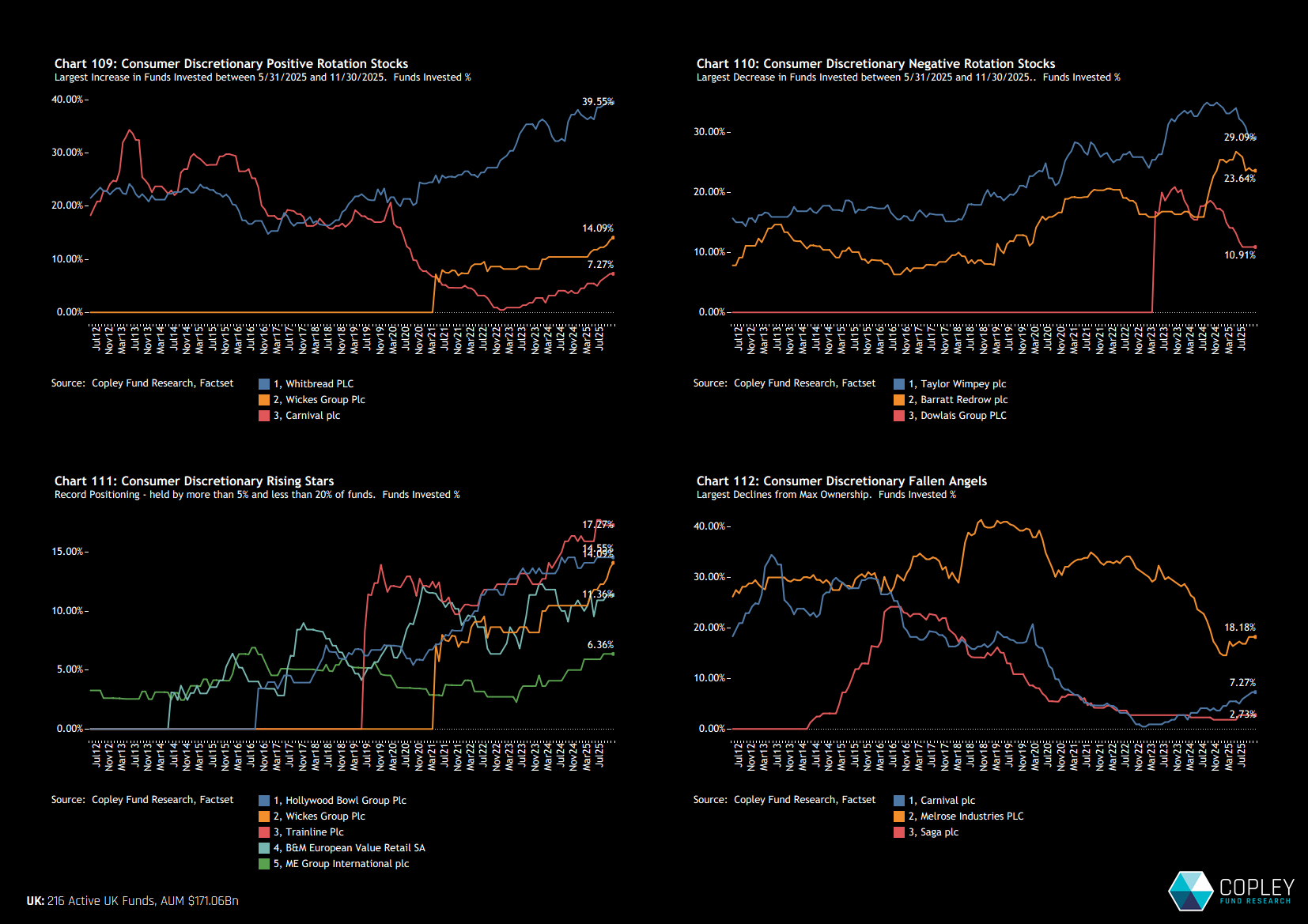

UK Consumer Discretionary Positioning: A Consensus Overweight

- Steve Holden

- 0 Comments

Related Posts

{kind=link}