17 December

Emerging Markets

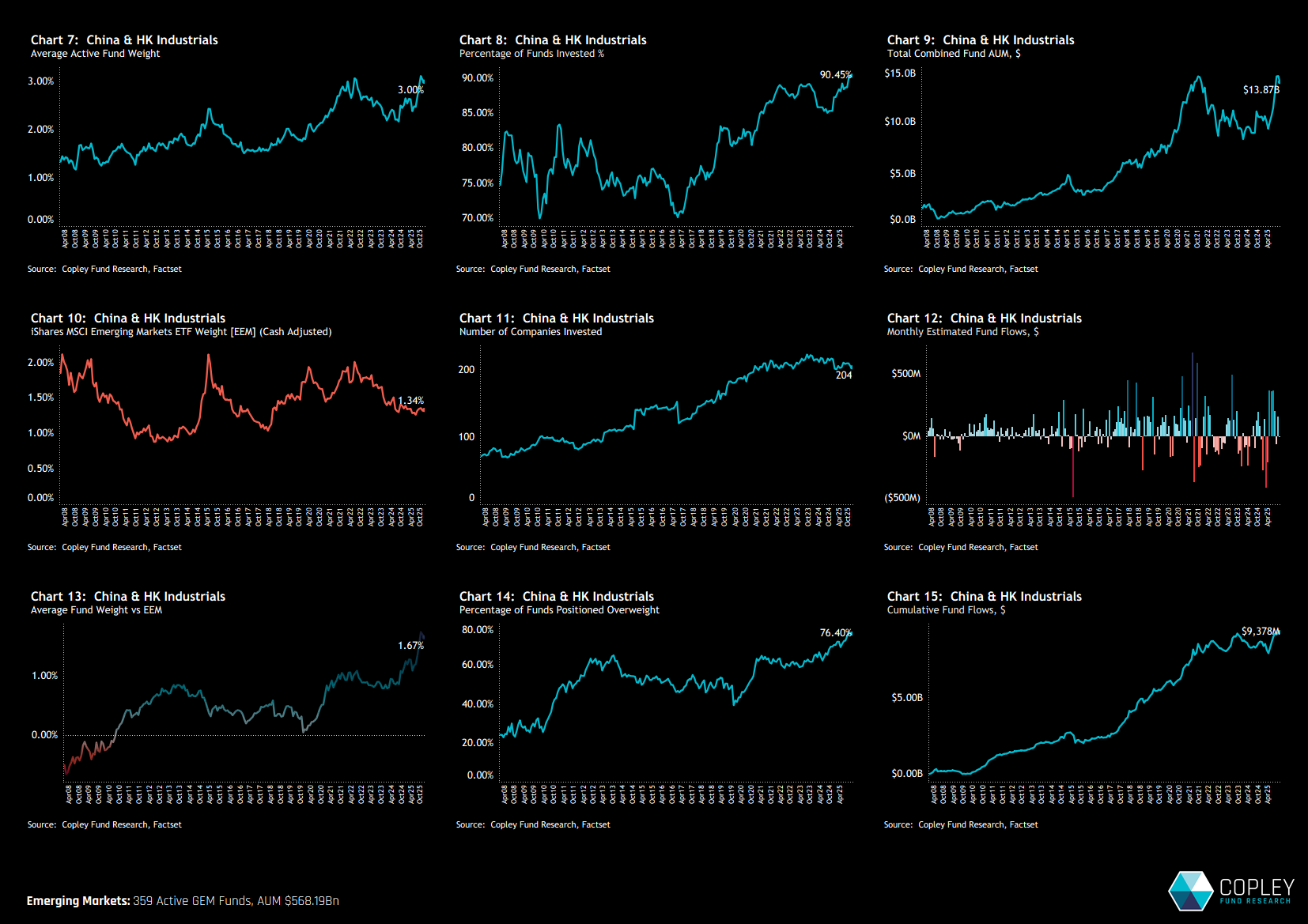

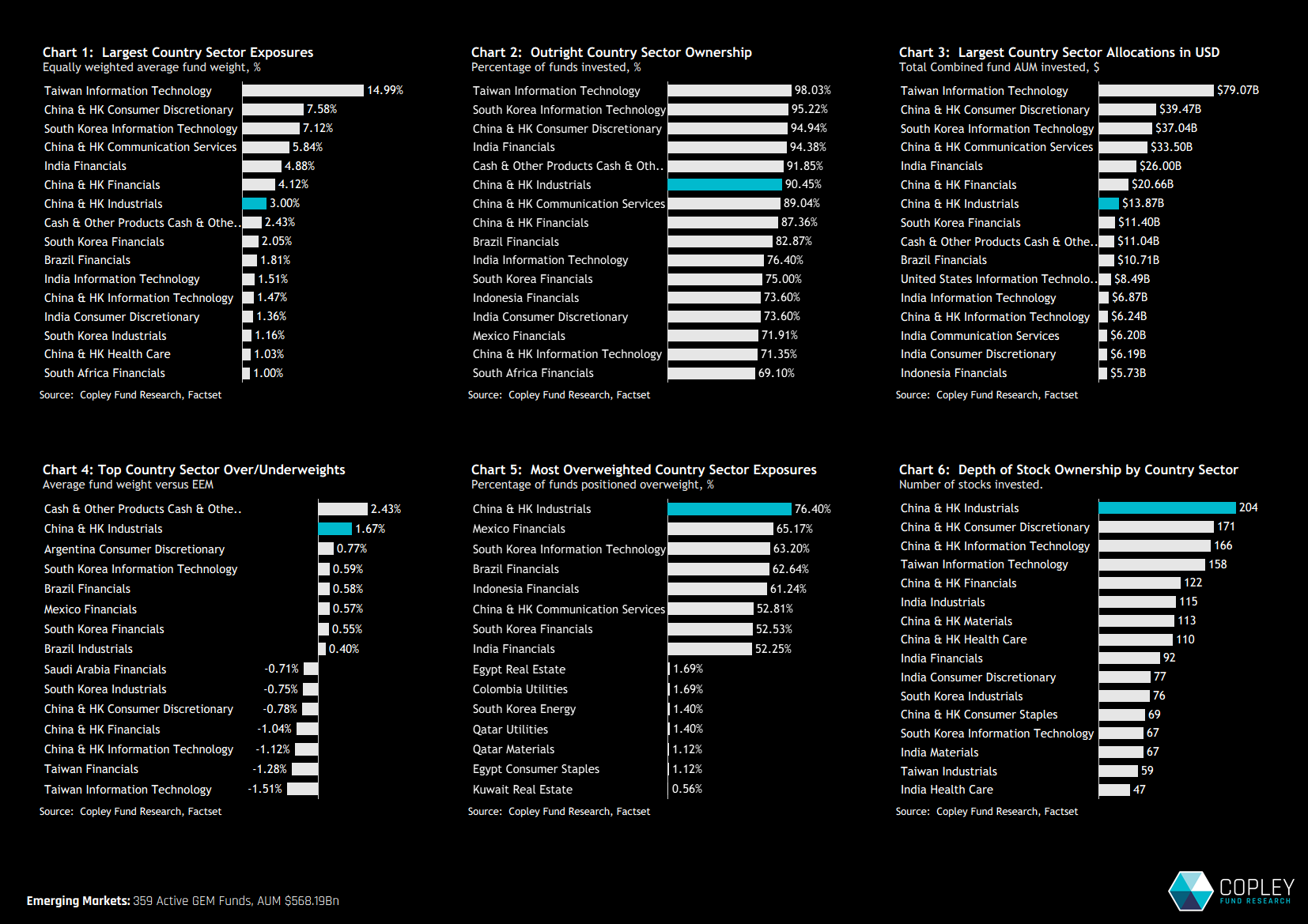

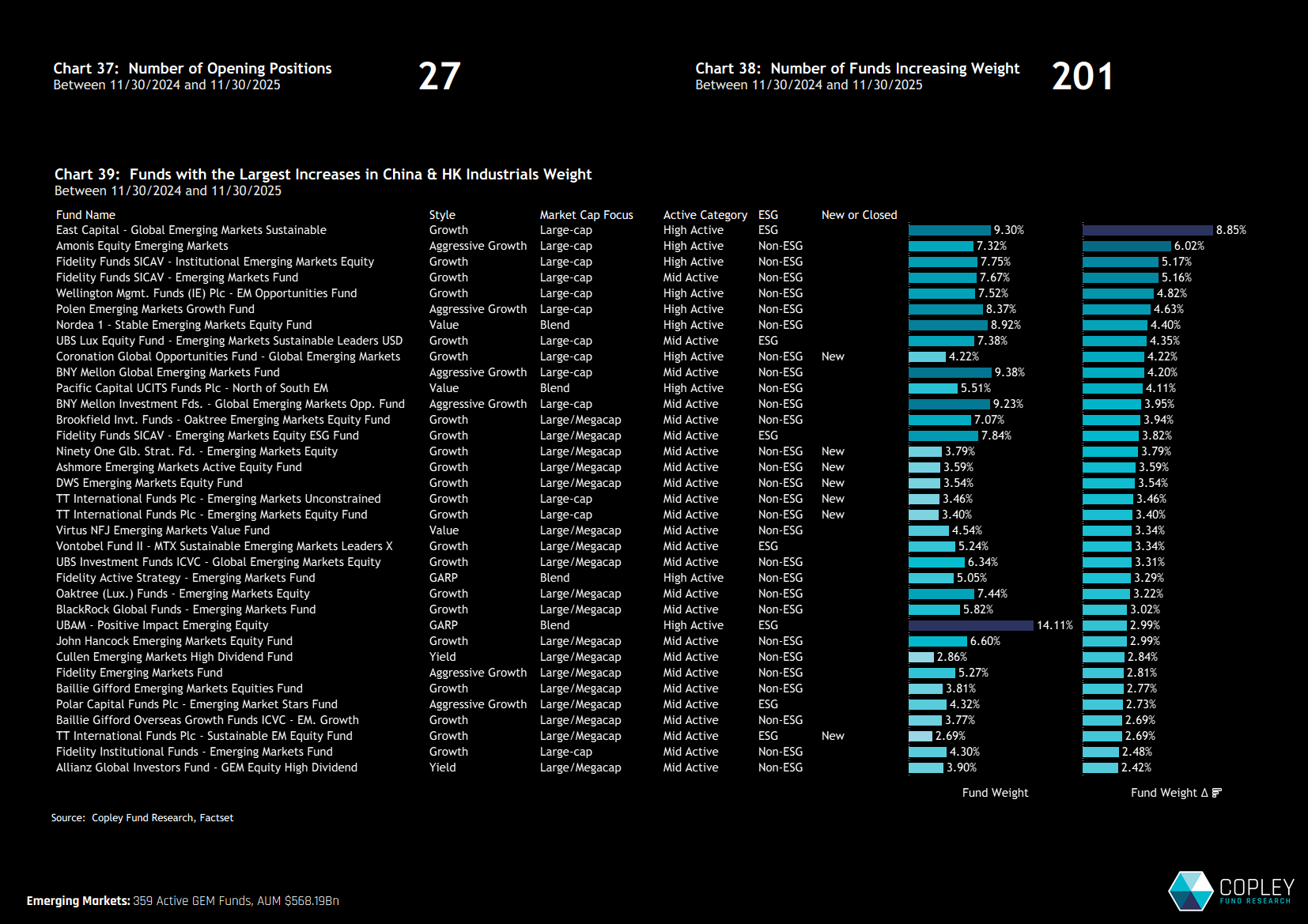

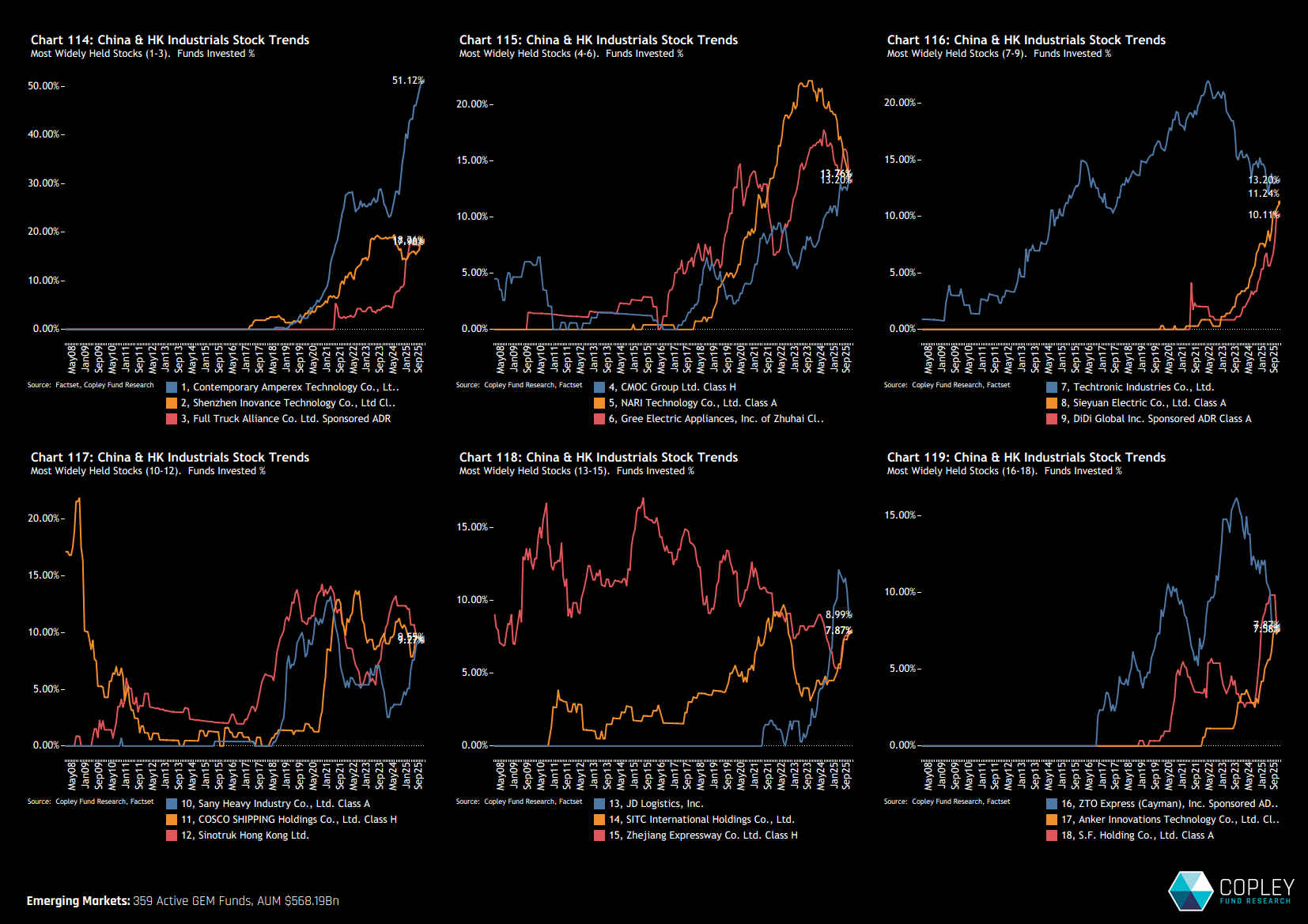

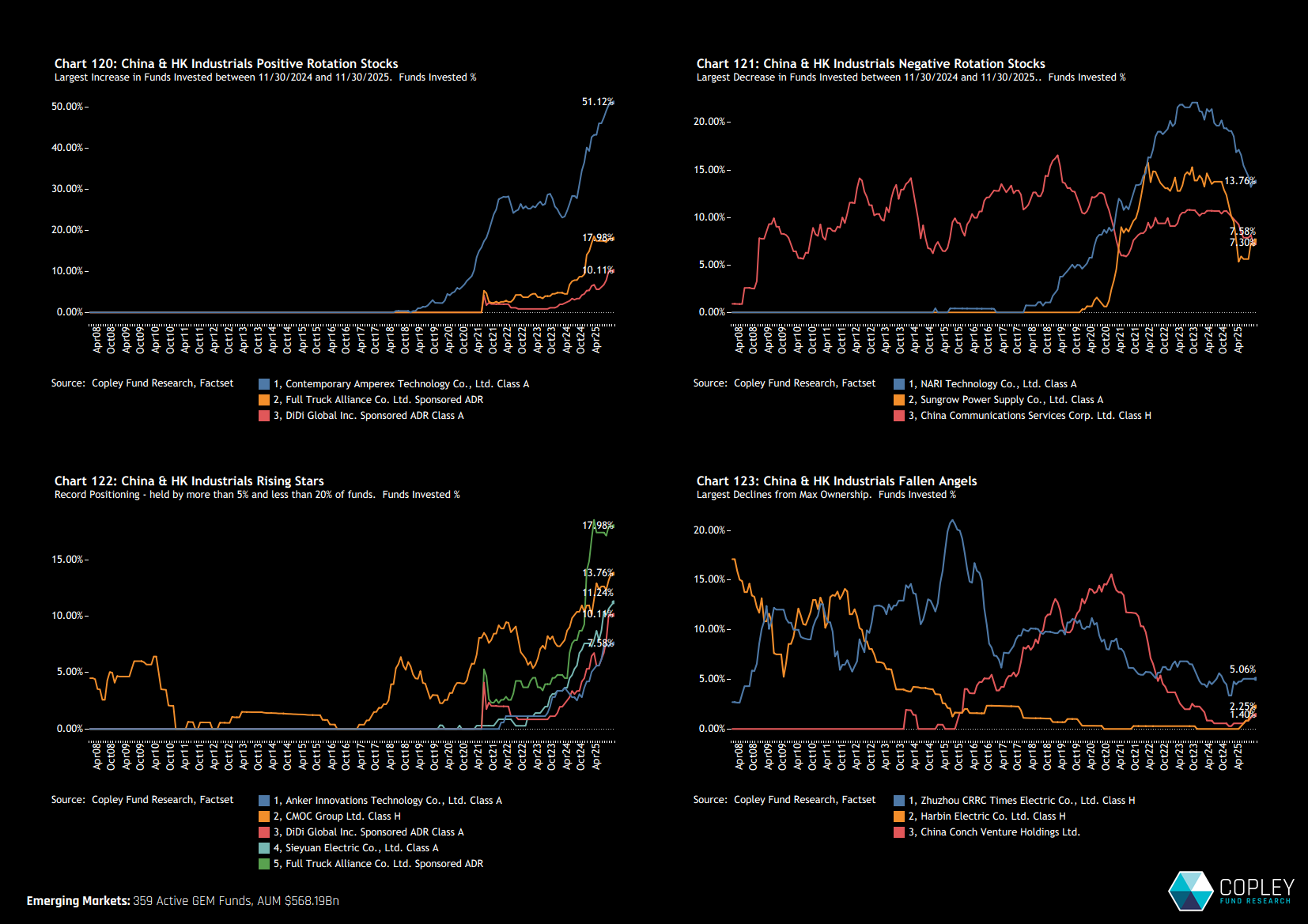

China & HK Industrials: EM’s Key Overweight Grows Stronger

- Steve Holden

- 0 Comments

Related Posts

{kind=link}