• UK Real Estate Hots Up: Record number of UK funds now exposed to Real Estate sector.

• UK Stock Radar: Natwest and Serco among 10 stocks at the extreme ends of their positioning and momentum ranges

• Stock Activity Data. They key moves in stock positioning over the last 6-months

270 UK Equity Funds, AUM $190bn

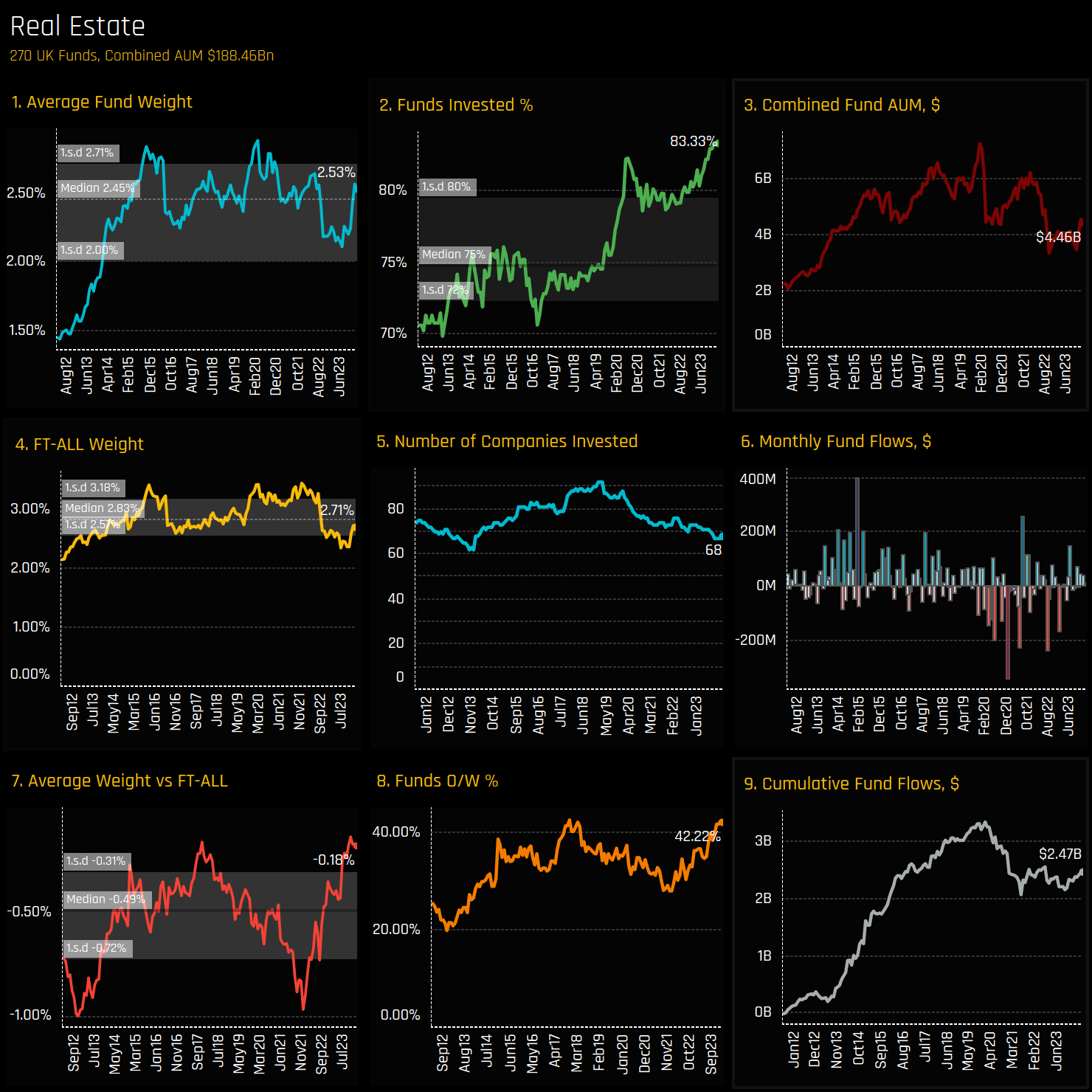

UK Real Estate Hots Up

• Record number of UK funds now exposed to Real Estate sector.

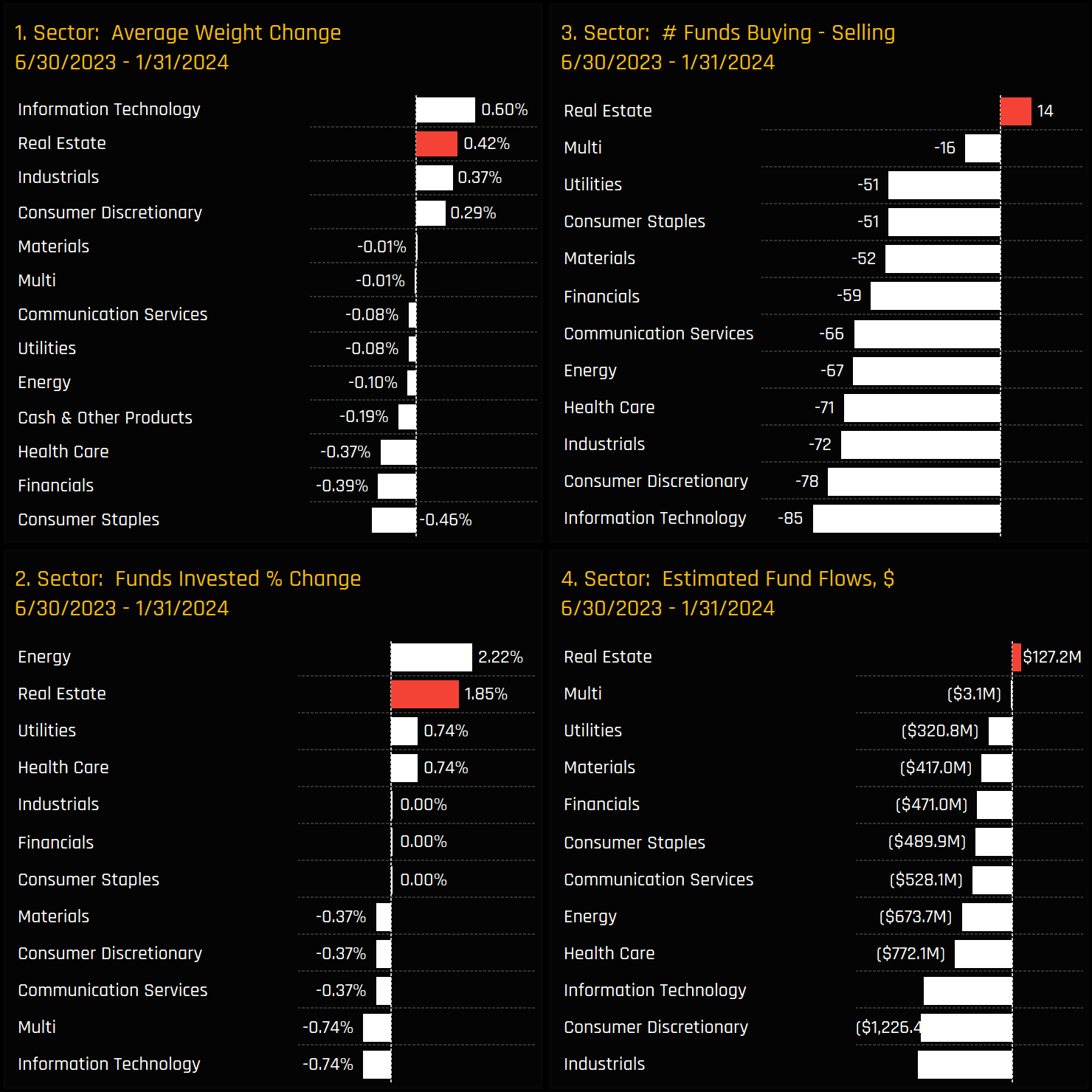

• CT, BlackRock and Quilter among funds adding to exposure since mid 2023.

• SEGRO and Land Securities the key holdings and the drivers behind the recent rotation

Time-Series Analysis

The percentage of UK equity funds invested in the Real Estate sector has hit an all-time high this month. As chart 2 below shows, a record 83.3% of the 270 UK funds in our analysis now own a position in the Real Estate sector, pushing average weights higher at a faster pace than the FTSE All Share index in recent months (ch1&4). As such, the net underweight has tightened from -1% to just -0.18%, with a record 42.2% of funds positioned overweight the benchmark index.

Sector Activity

The charts below show the changes in sector exposure and ownership between the recent lows of 6/30/2023 and 01/31/2024. Real Estate emerged as a major beneficiary over the period, securing the second-largest increase in average weight and funds invested of 0.42% and 1.85% respectively. It was the only sector to see net inflows and more buyers than sellers.

Fund Level Activity

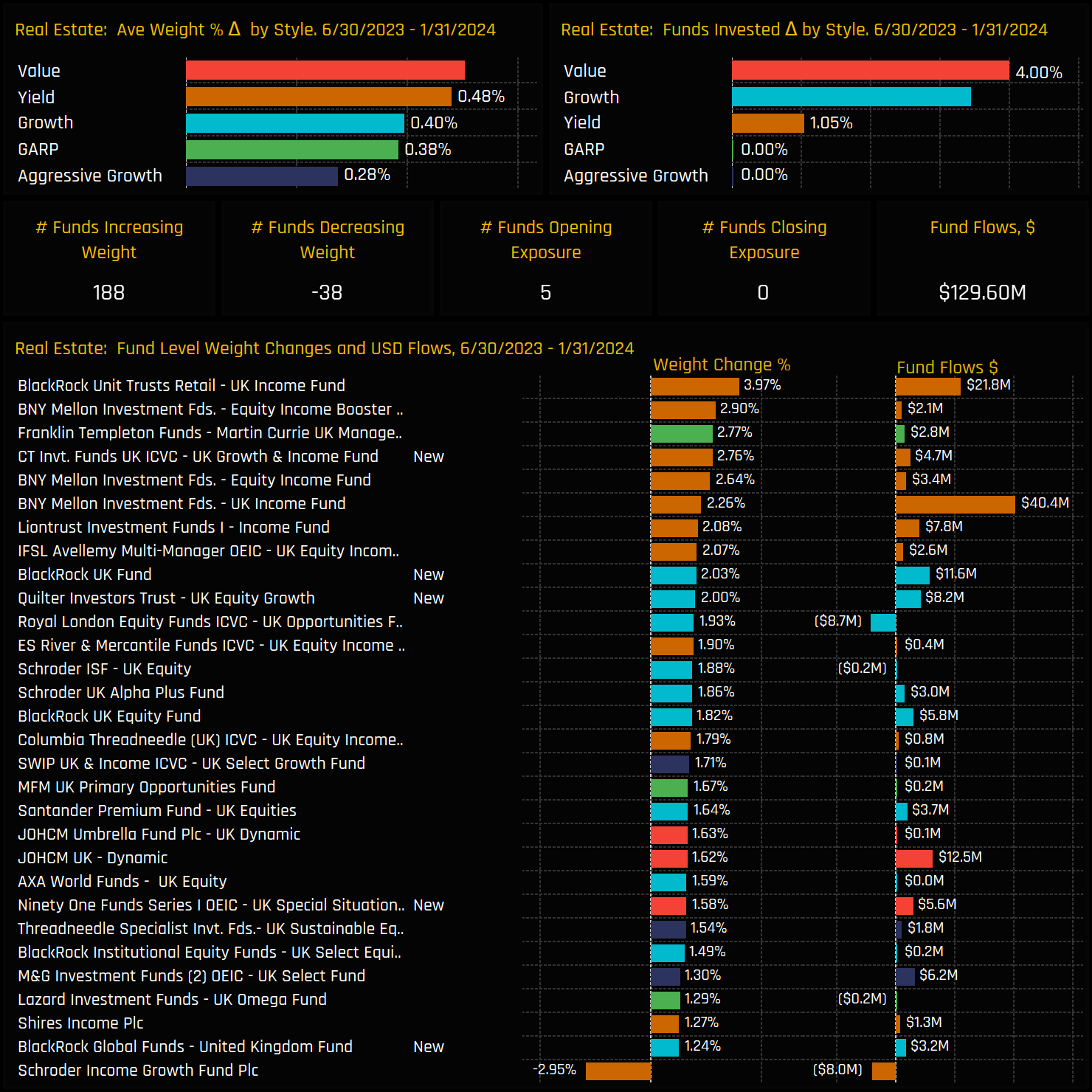

On a fund level, 188 funds increased their Real Estate holdings from 06/30/2023 to 01/31/2024, compared to 38 funds that reduced their stakes. Additionally, 5 funds opened new Real Estate positions, with no exits reported. Value and Yield funds saw the most significant increases, though Growth funds also participated.

The largest gains in Real Estate exposure were recorded by BlackRock UK Income (3.97%) and BNY Mellon UK Income (2.9%), with Yield managers making up 7 of the top 10 increases.

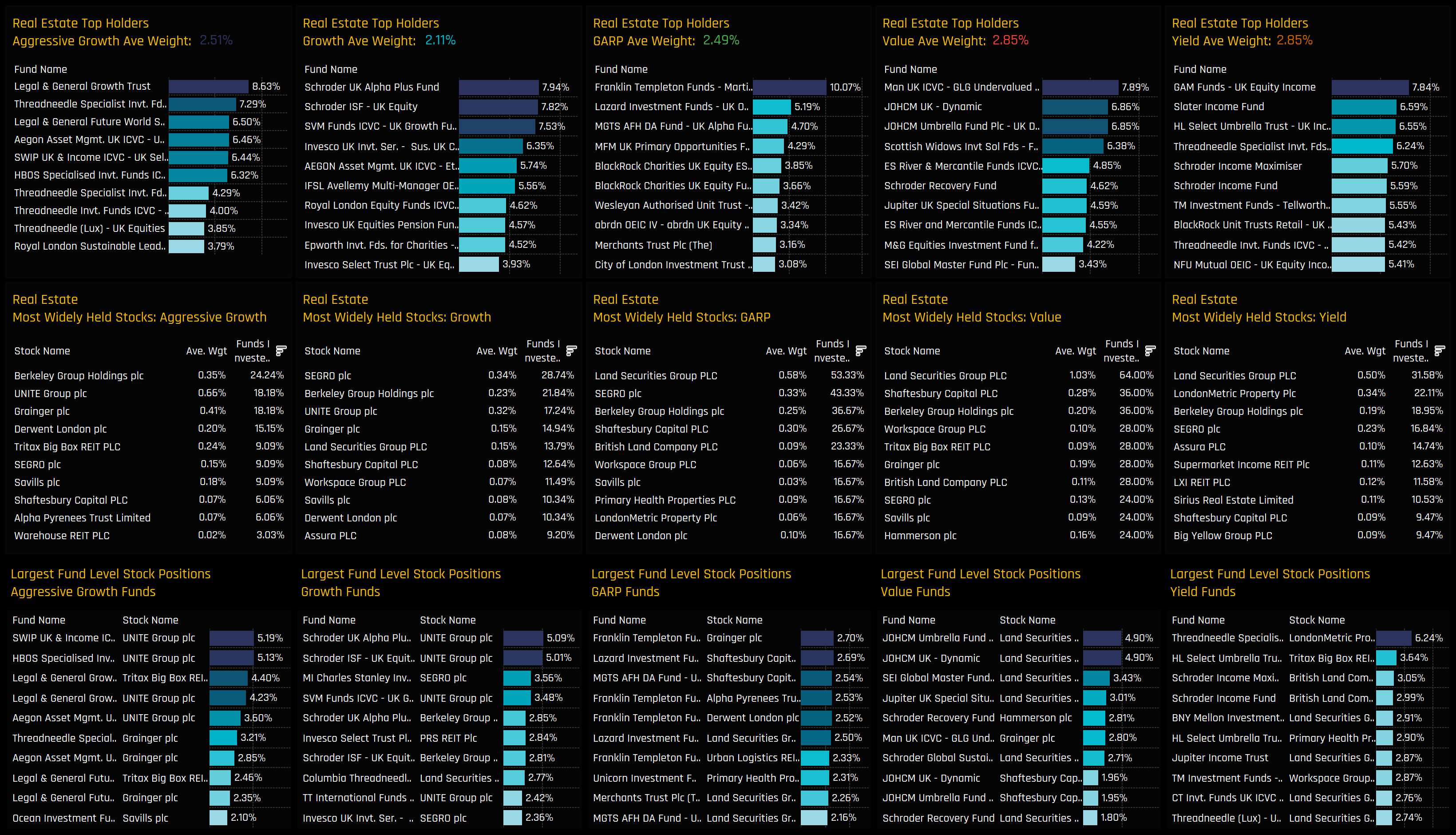

Scroll down to view the major stock holdings in the Real Estate sector, split by fund style. Click on the link below for a more granular look at Real Estate positioning among UK active equity funds.

• Investment levels vary significantly across the UK investible universe, with some stocks being widely held while others are scarcely owned, and these ownership levels fluctuate monthly.

• Our analysis synthesizes current and historical data on fund positioning with recent manager activity to accurately assess sentiment for each stock within our UK coverage.

• We spotlight 10 stocks that not only sit at the extreme ends of their historical position ranges, but have also experienced notable shifts in fund ownership in recent months.

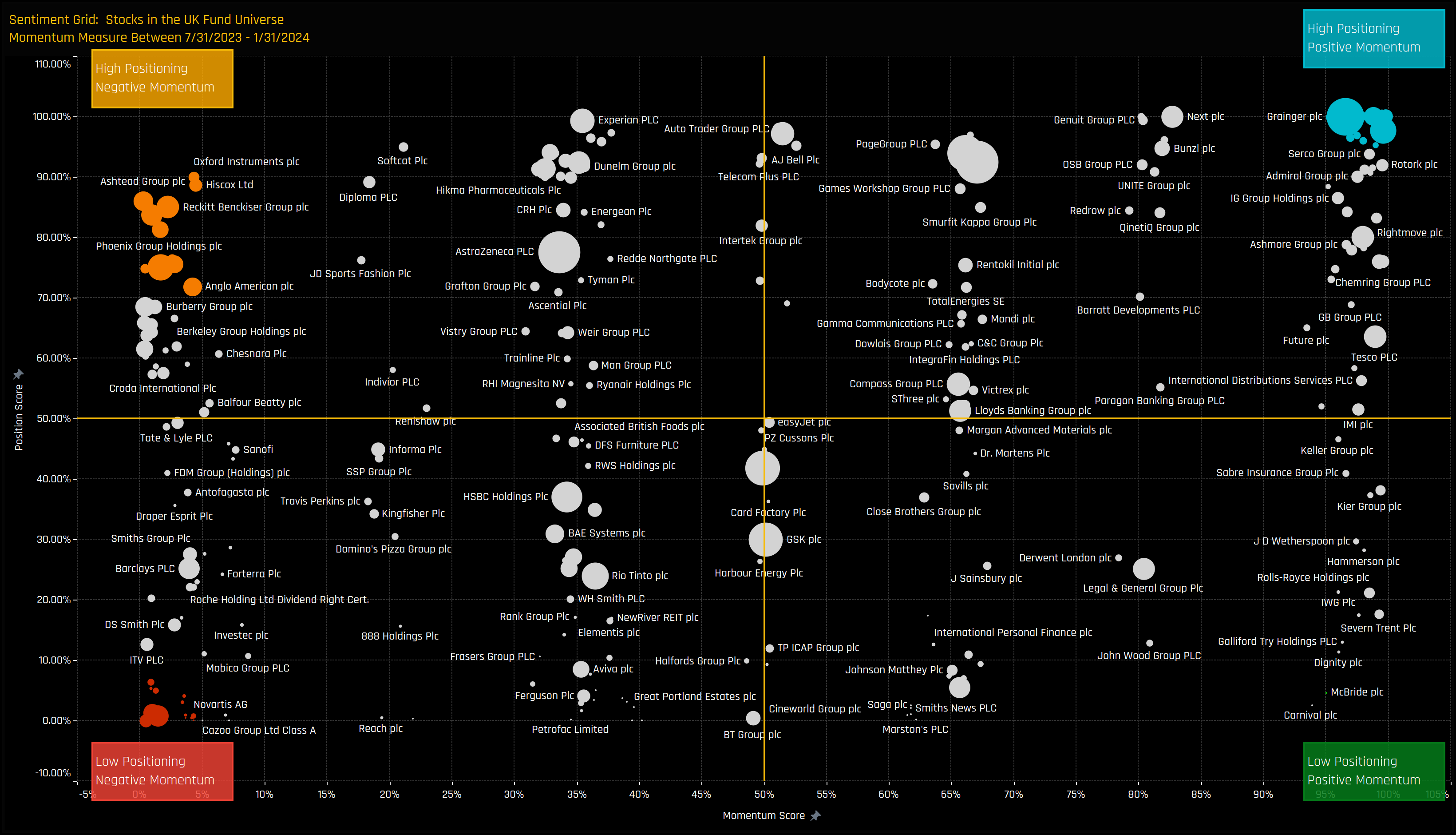

Stock Sentiment

The Sentiment Grid below is designed to visualize the interplay between current fund positioning, long-term fund positioning and shorter-term fund manager activity for all stocks in the UK fund active universe. The Y-axis shows the ‘Position Score’, a measure of current positioning in each stock compared to its own history going back to 2012 on a scale of 0-100%. It takes in to account the percentage of funds invested in each stock versus history, the average fund weight versus history and the percentage of funds overweight the benchmark versus history. The higher the number, the more heavily a stock is owned by active UK managers compared to its own history.

The X-Axis shows the ‘Momentum Score’, a measure of fund manager activity for each stock between 07/31/2023 and 1/31/2024 on a scale of 0% (maximum negative activity) to 100% (maximum positive activity). The Momentum Score takes in to account the change in the percentage of funds invested in each stock over the period, the change in average weight and the change in the percentage of funds overweight. The chart also highlights the companies at the extreme ends of each quadrant by colour, which will shall explore in more detail below.

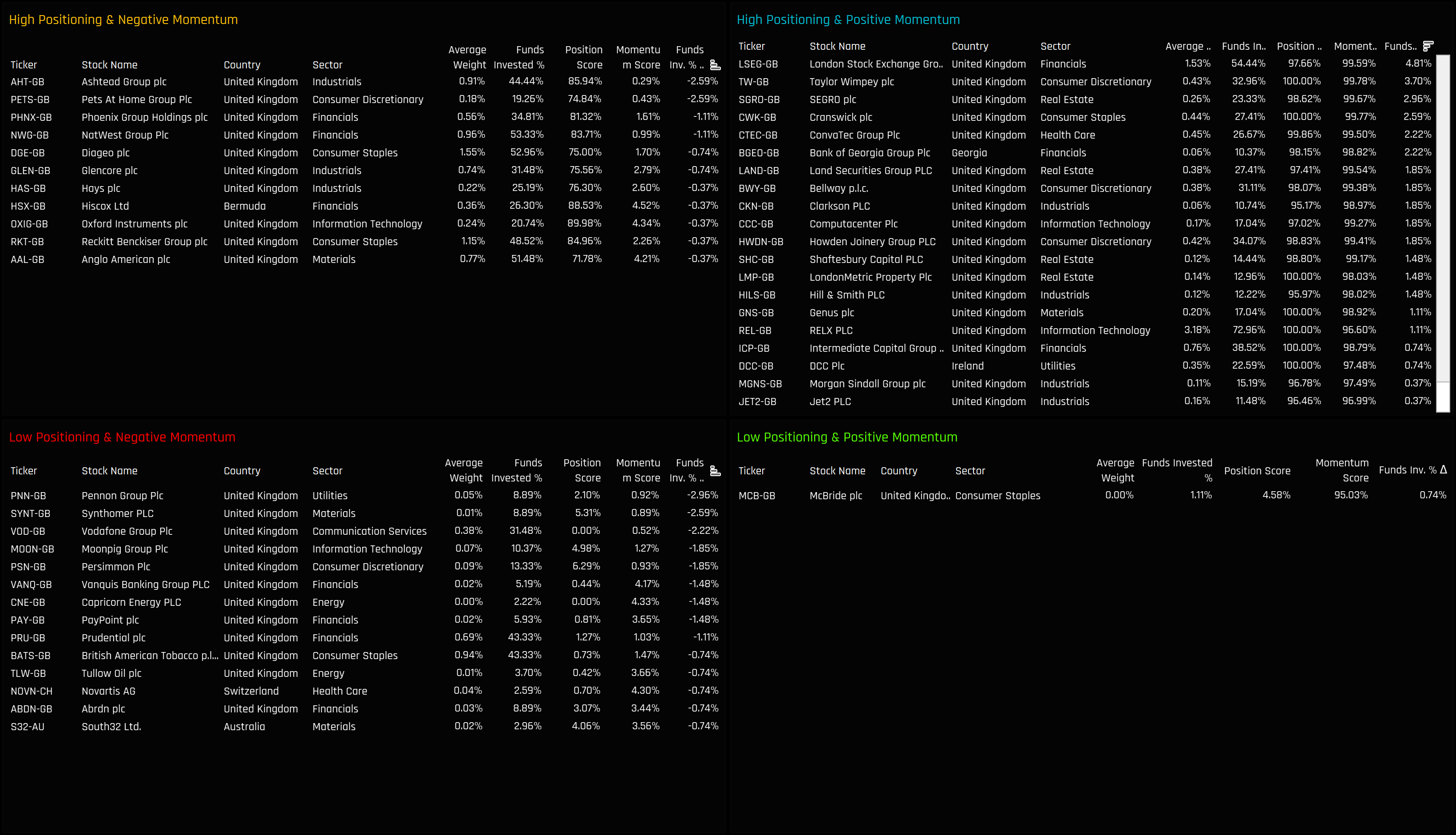

Extreme Stocks

The tables below list the stocks in the extreme corners of each quadrant. The screening methodology is as follows:

High Positioning & Negative Momentum: Position Score > 70%. Momentum Score < 5%

High Positioning & Positive Momentum: Position Score > 95%. Momentum Score > 95%

Extreme Stock Focus

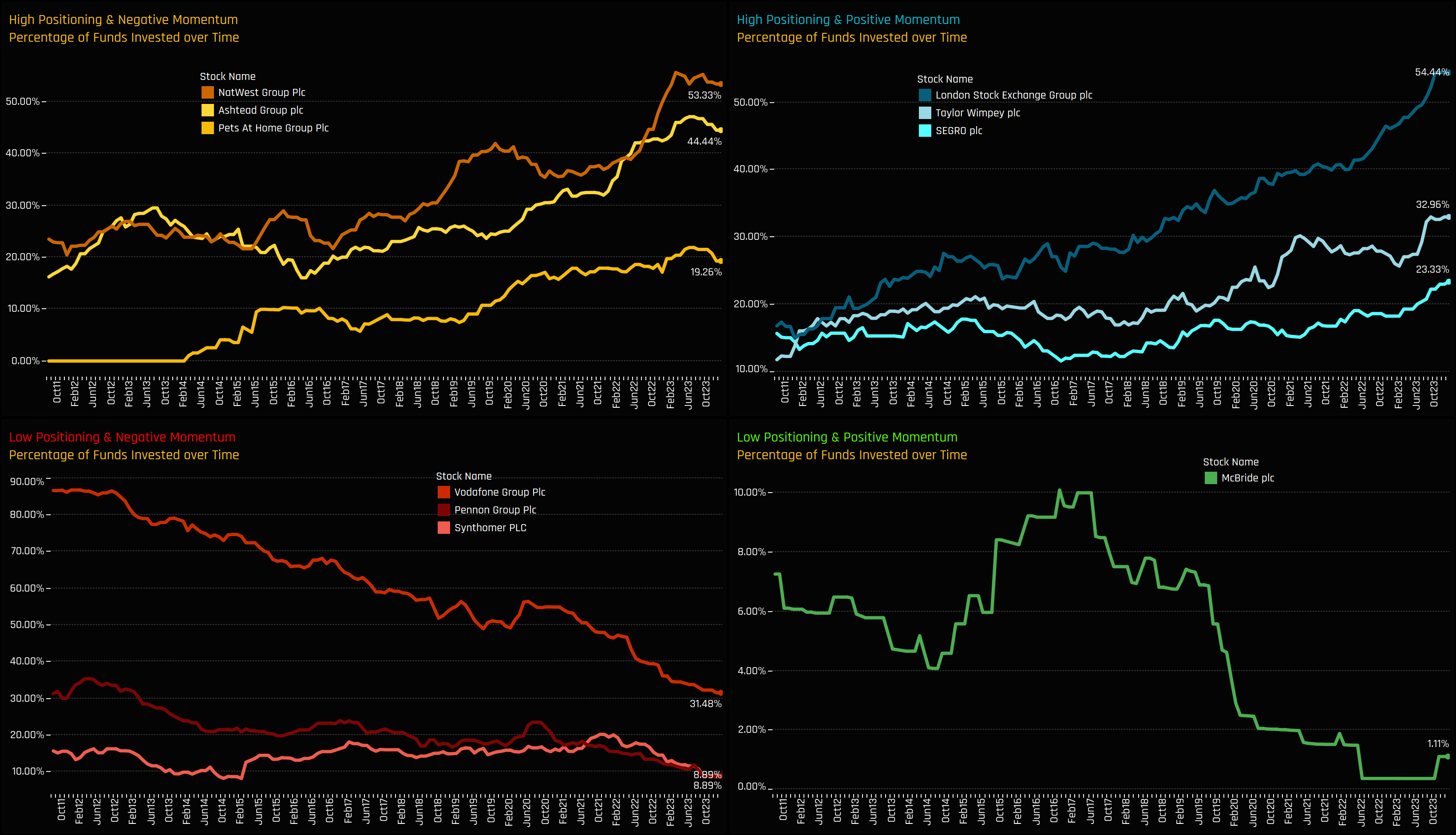

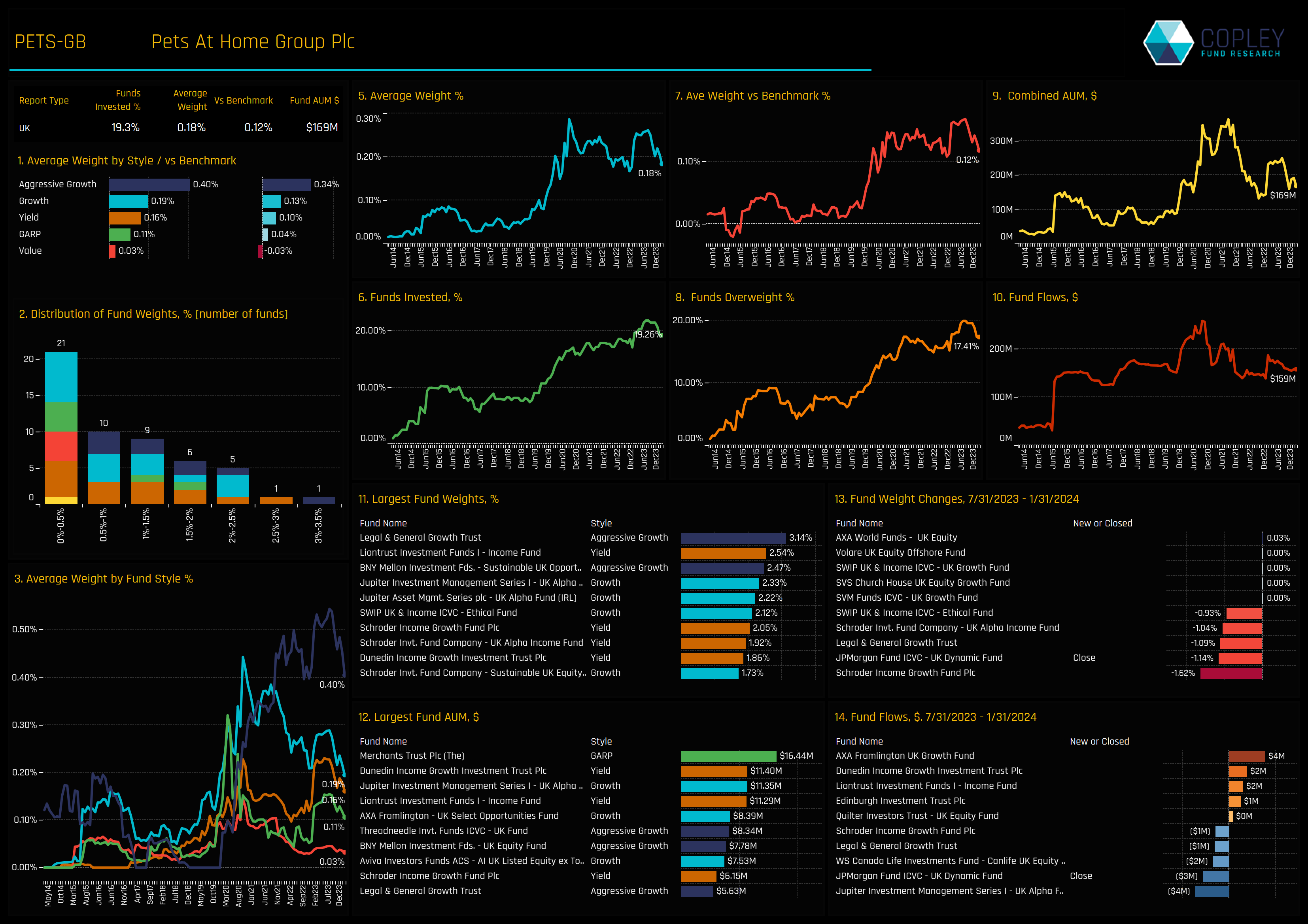

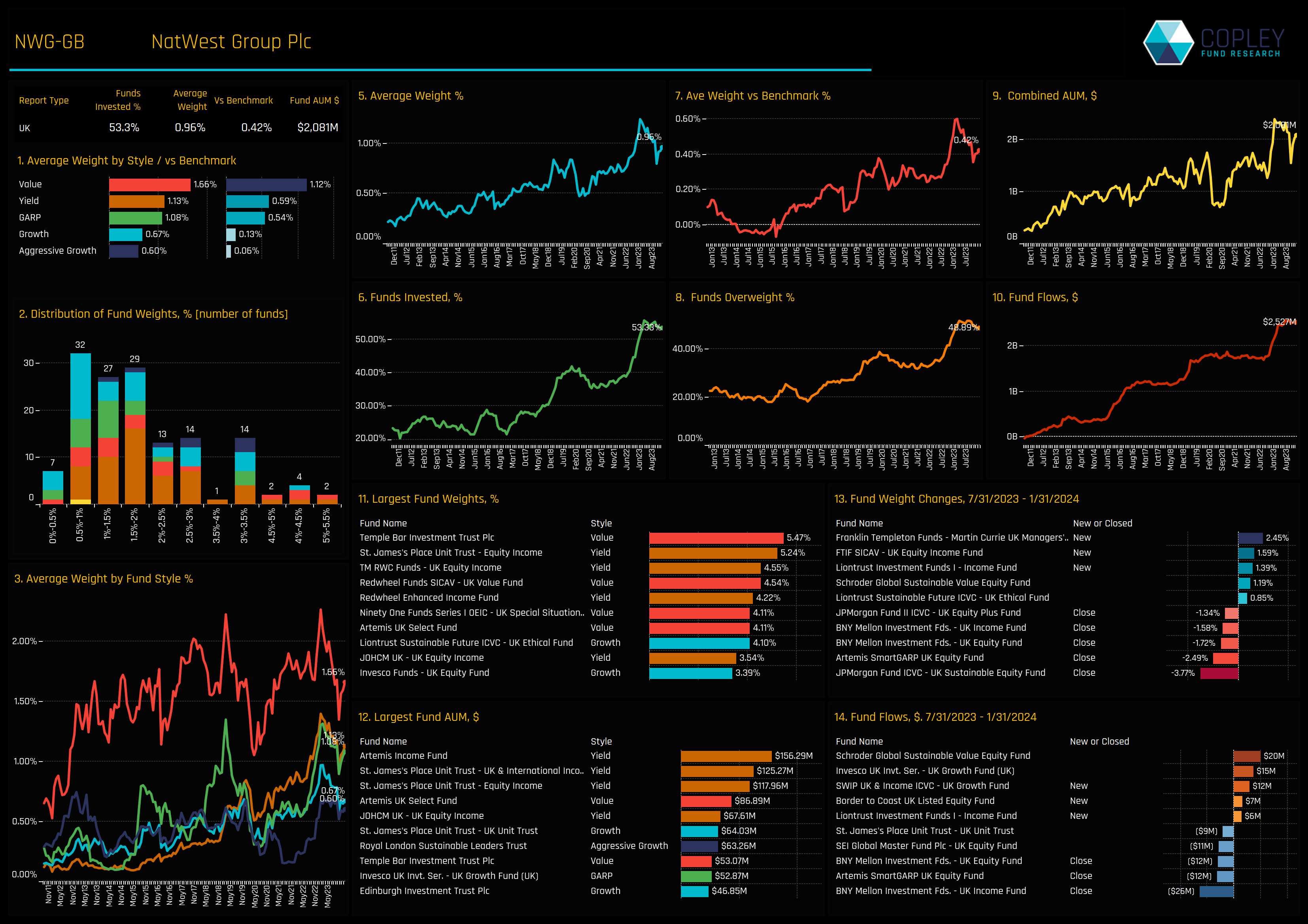

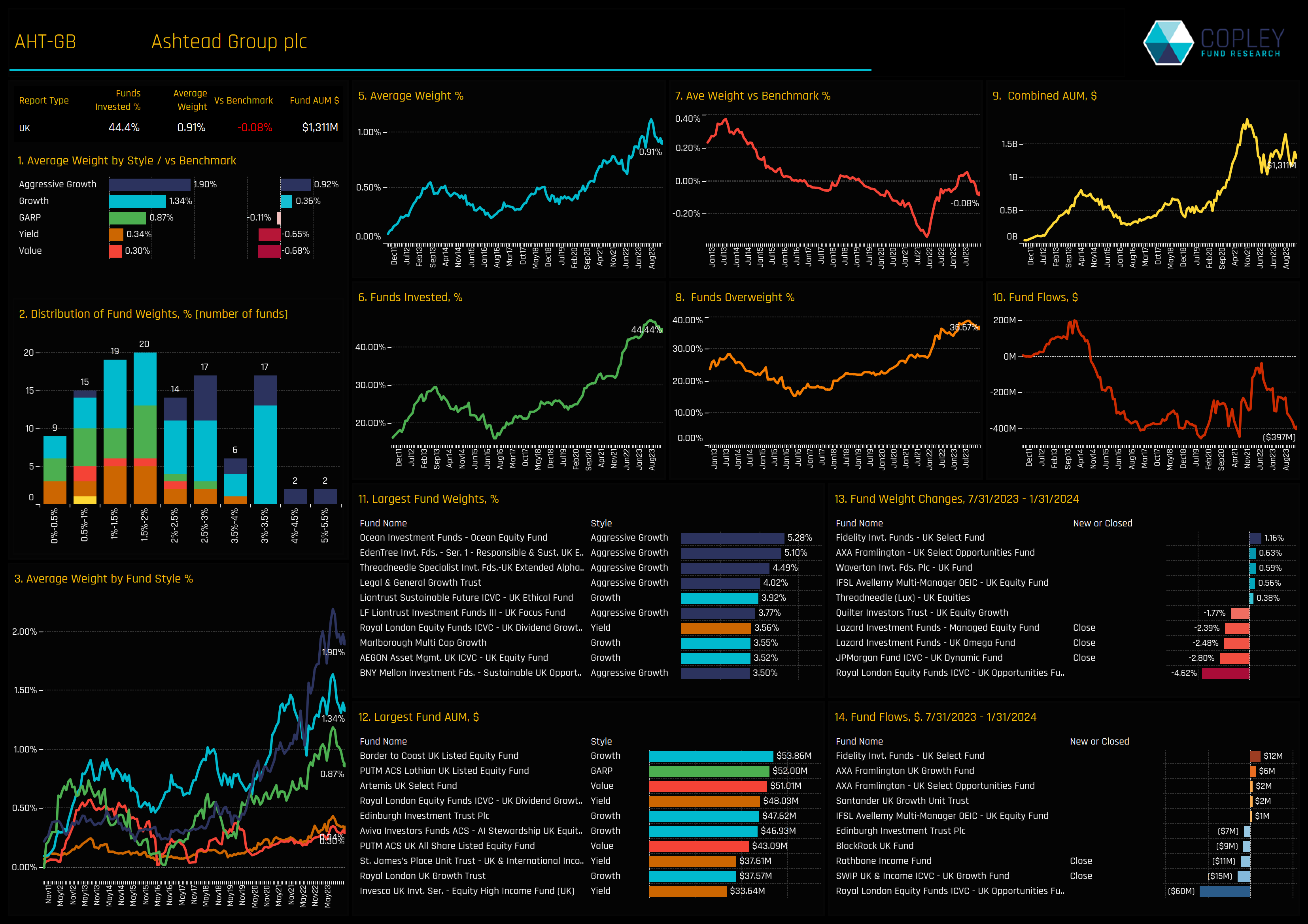

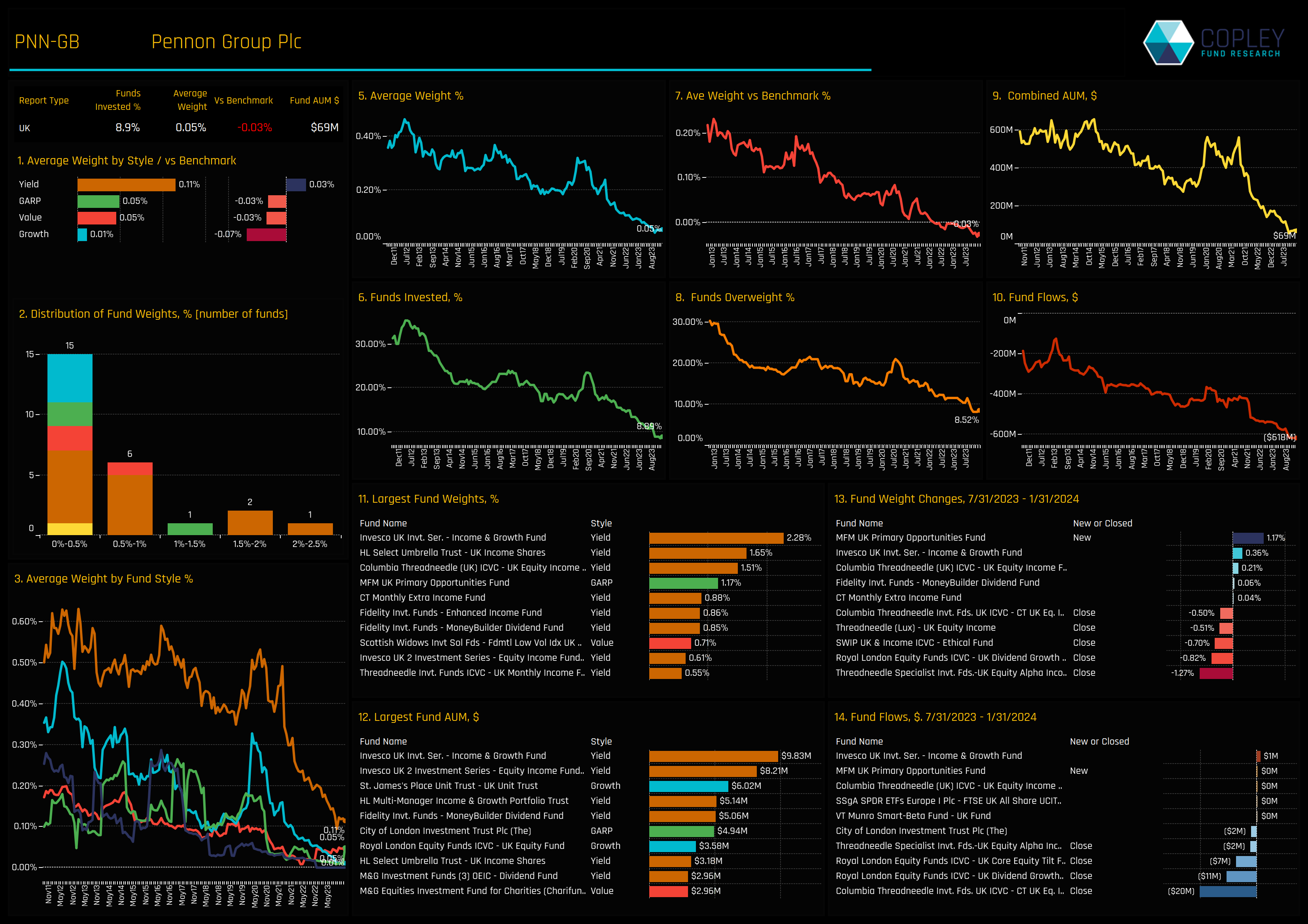

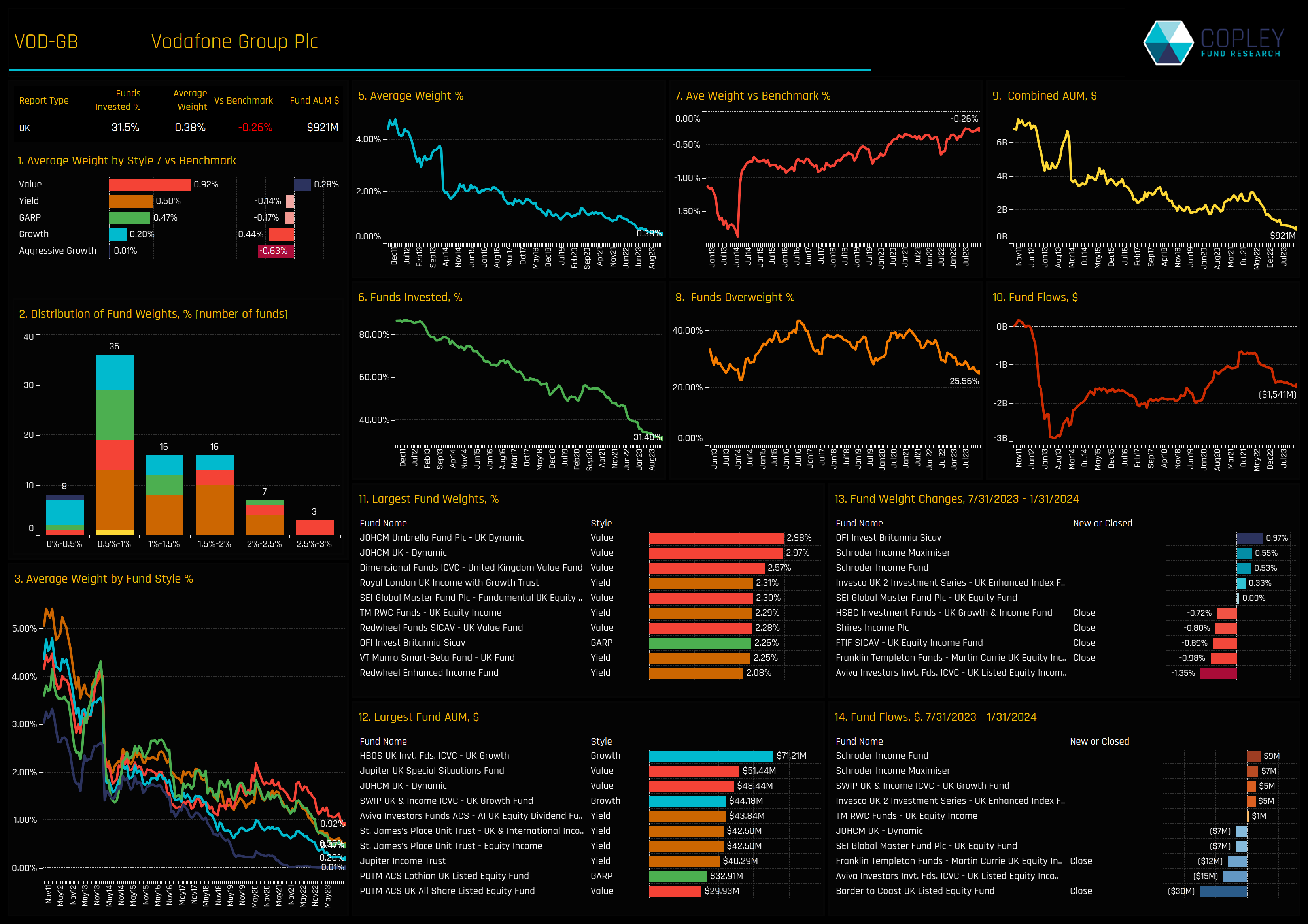

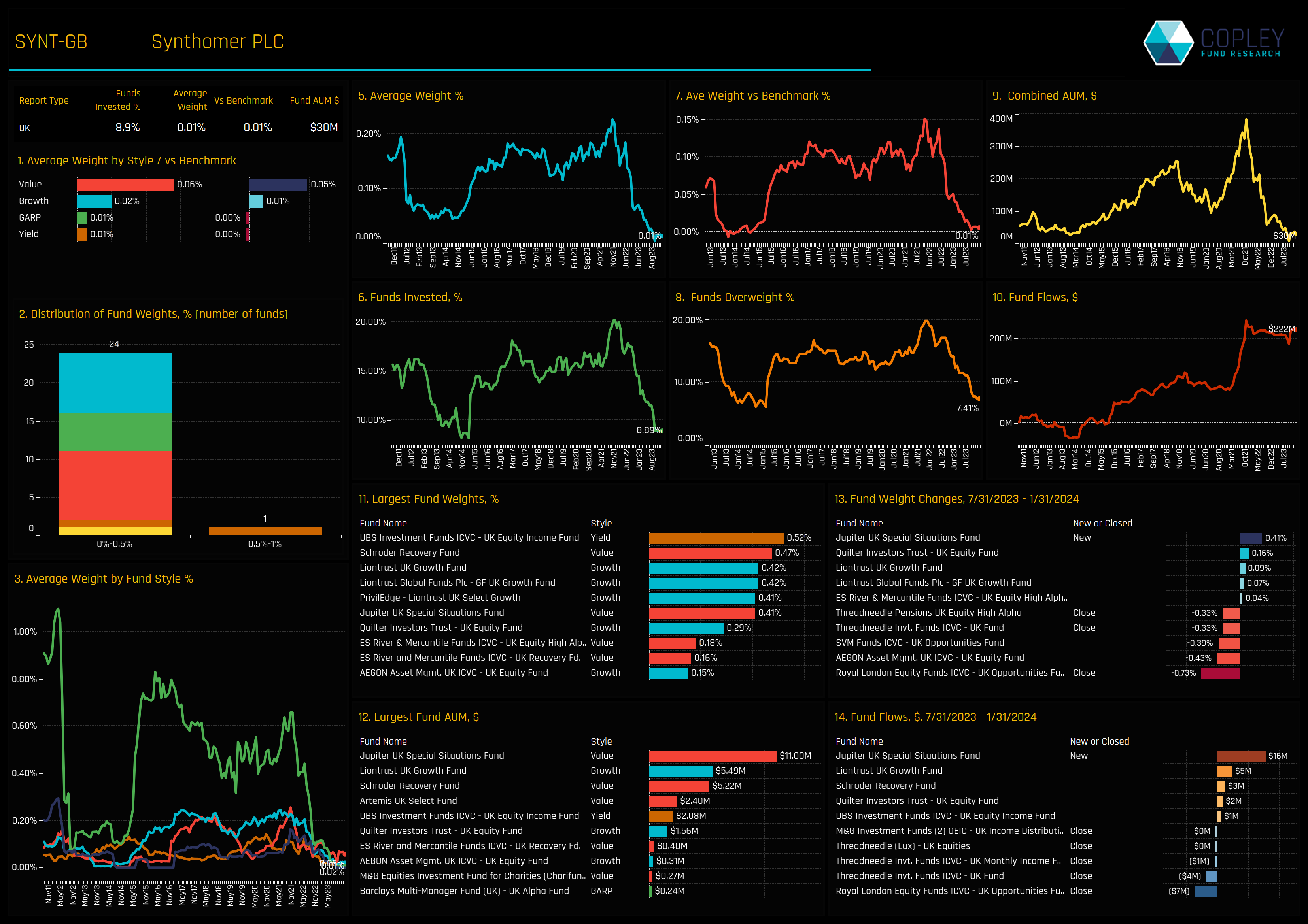

The following charts illustrate the proportion of active funds invested in the top 3 stocks within each of the 4 categories. This visualization provides an additional perspective on how the Sentiment Grid works. The top-left chart reveals a downturn in holdings for NatWest Group, Ashtead Group and Pets At Home Group following a sustained period of growth. In contrast, the bottom-left chart illustrates a consistent decrease in fund investment in Vodafone, Pennon Group and Synthomer plc, with recent sell-offs driving ownership to a 13-year low.

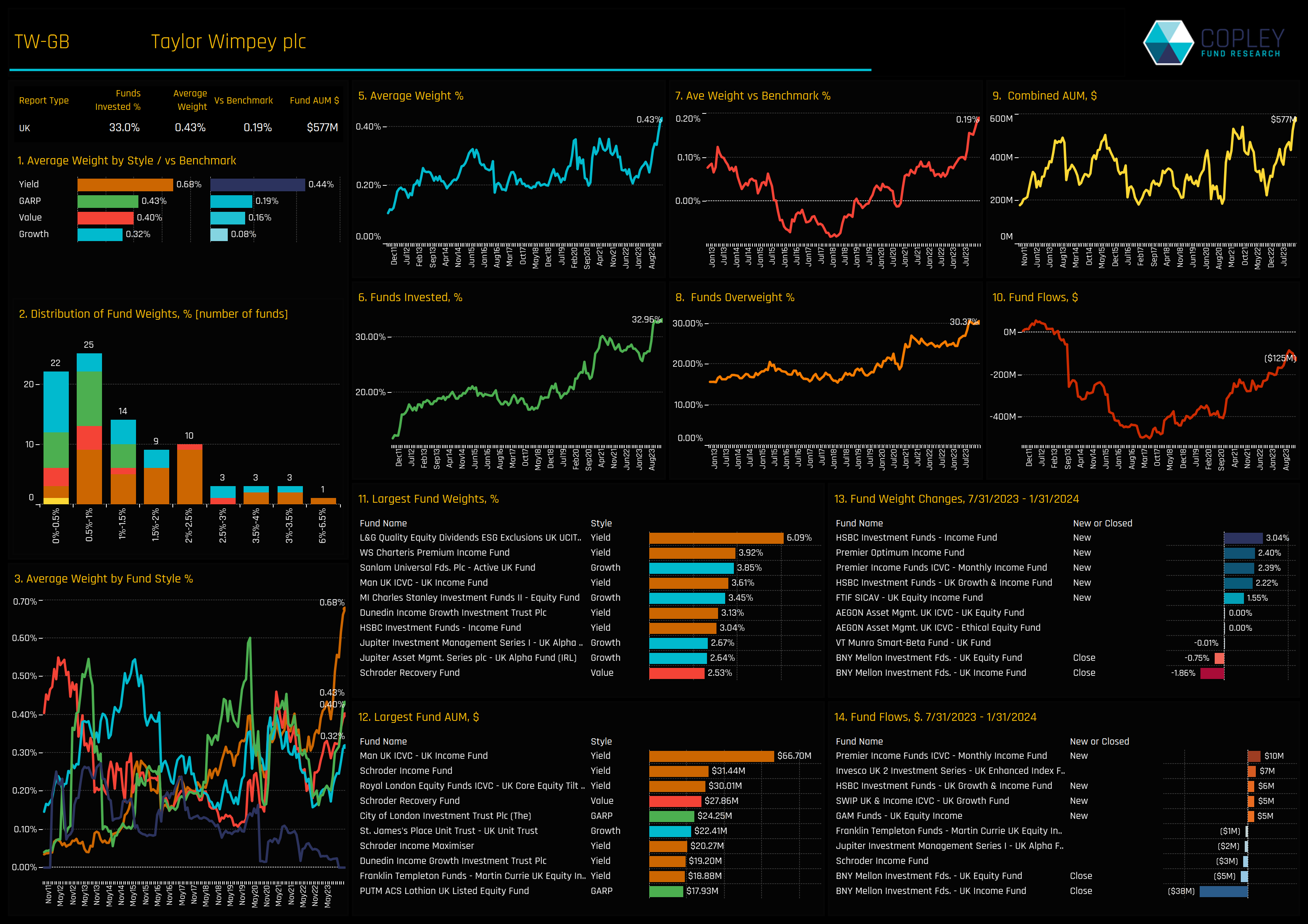

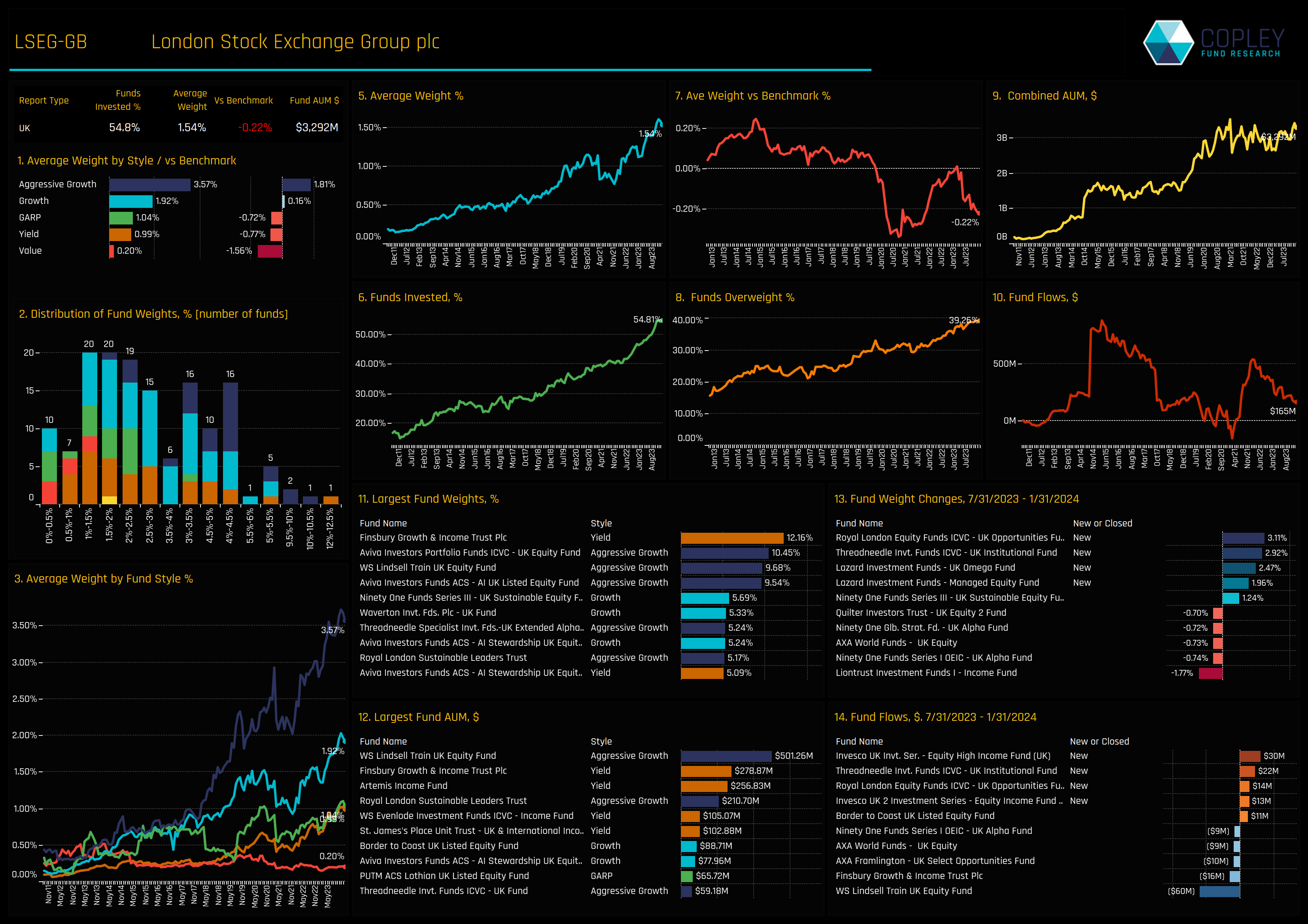

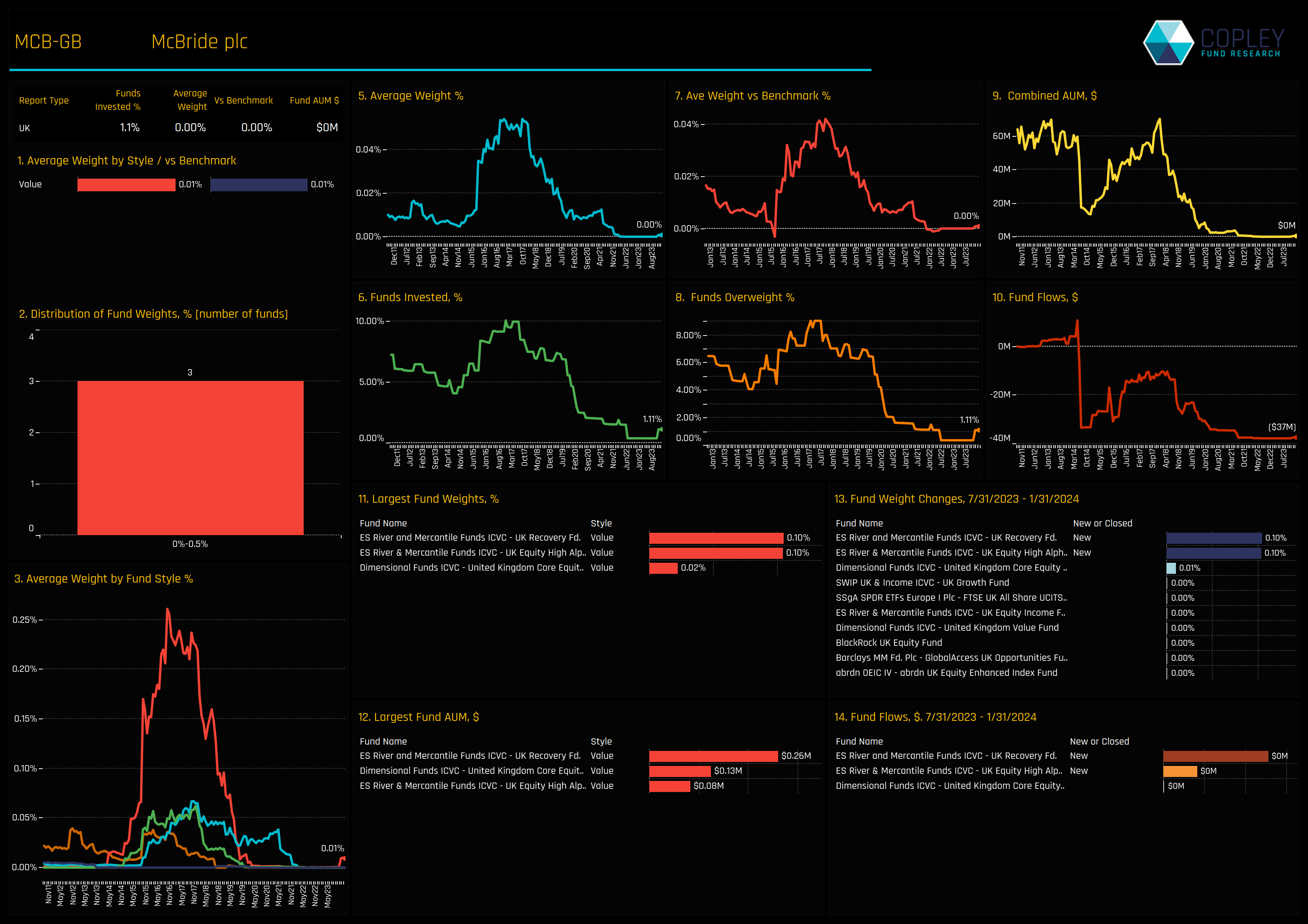

Focusing on the bottom right chart, we see McBride plc positioned at the lower extremes of its ownership history, though a small uptick has occurred more recently. The top right chart indicates that LSE Group, Taylor Wimpey and SEGRO plc have reached record levels of ownership after months of increasing fund engagement. More in-depth profiles of these 10 key stocks from the extremes of our Sentiment Grid are detailed in the charts below.

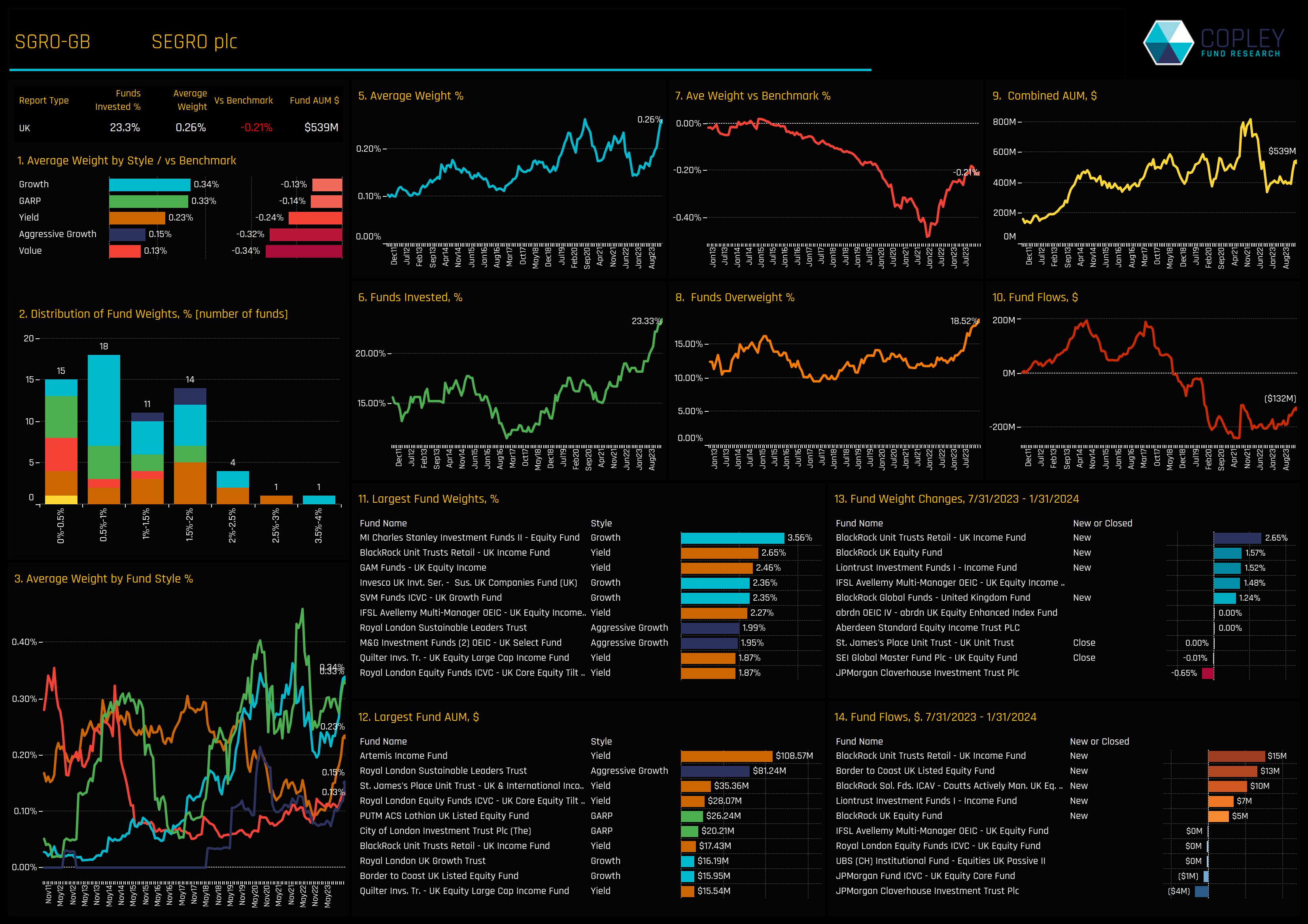

Stock Profile: SEGRO plc

Stock Profile: Taylor Wimpey plc

Stock Profile: London Stock Exchange Group plc

Stock Profile: Pets At Home plc

Stock Profile: Natwest Group plc

Stock Profile: Ashtead Group plc

Stock Profile: Pennon Group plc

Stock Profile: Vodafone Group plc

Stock Profile: Synthomer plc

Stock Profile: McBride plc

270 UK Equity Funds, AUM $190bn

UK Fund Stock Activity Data

The latest stock activity data for UK equity funds over the last 6-months.

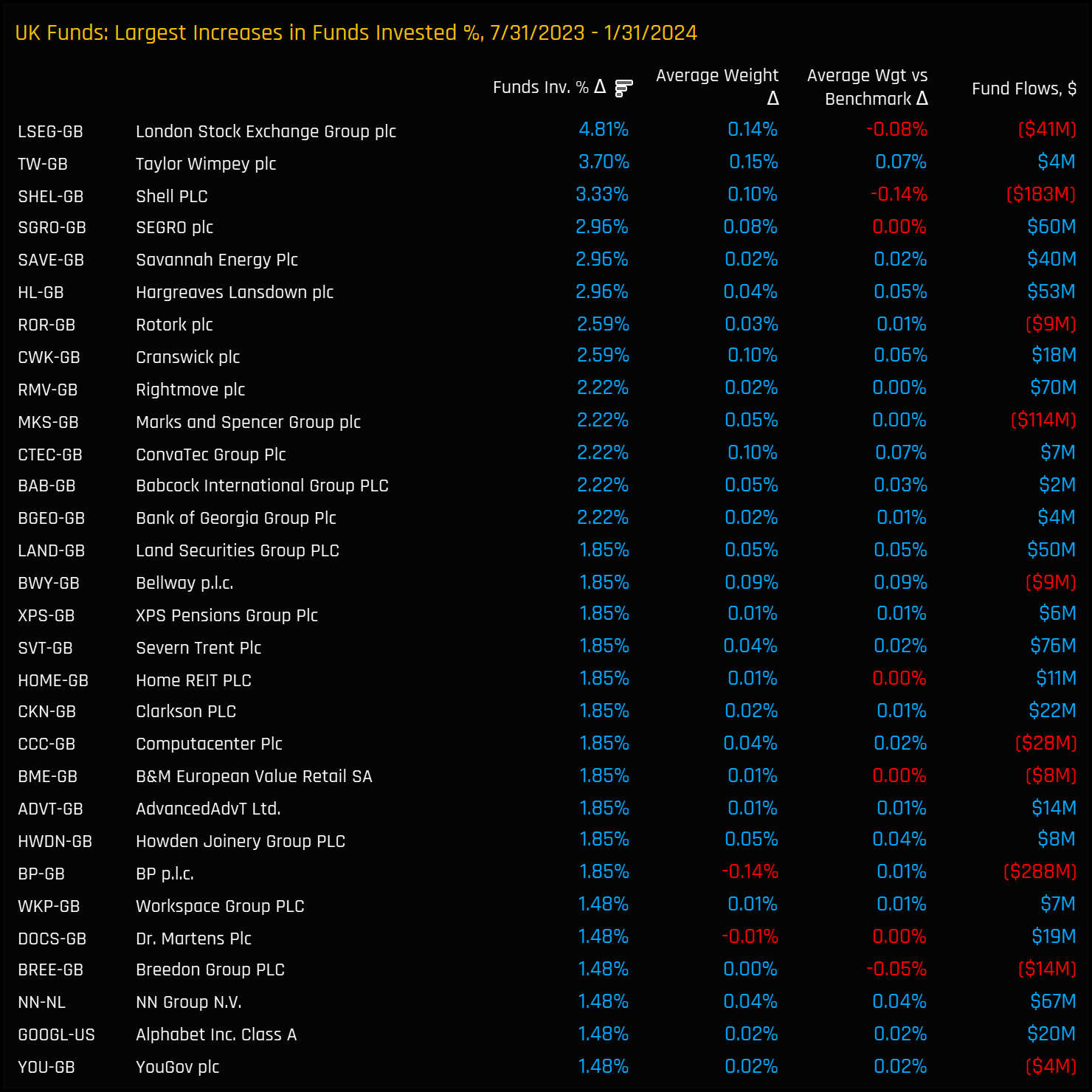

Largest Aggregate Increases in Ownership

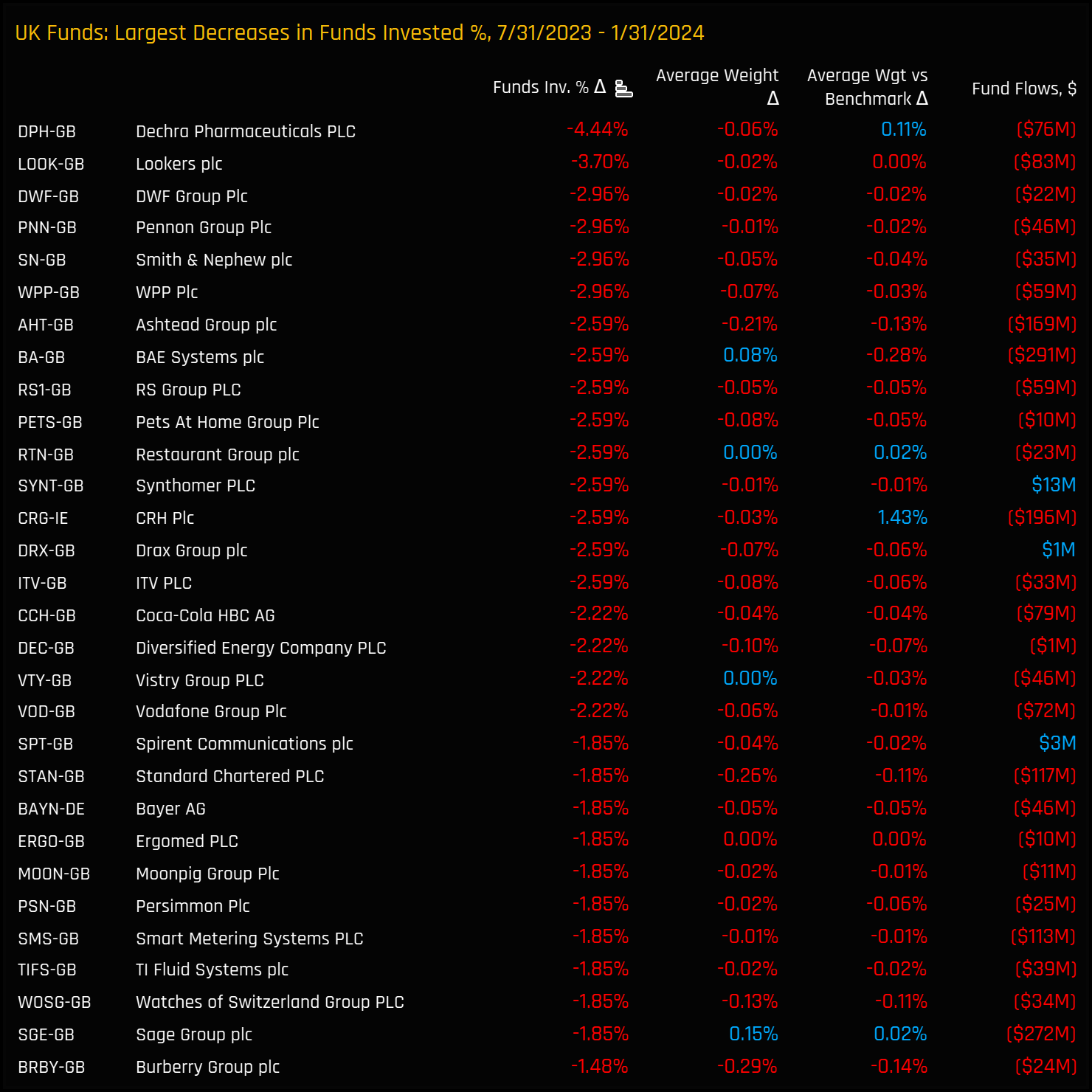

Largest Aggregate Decreases in Ownership

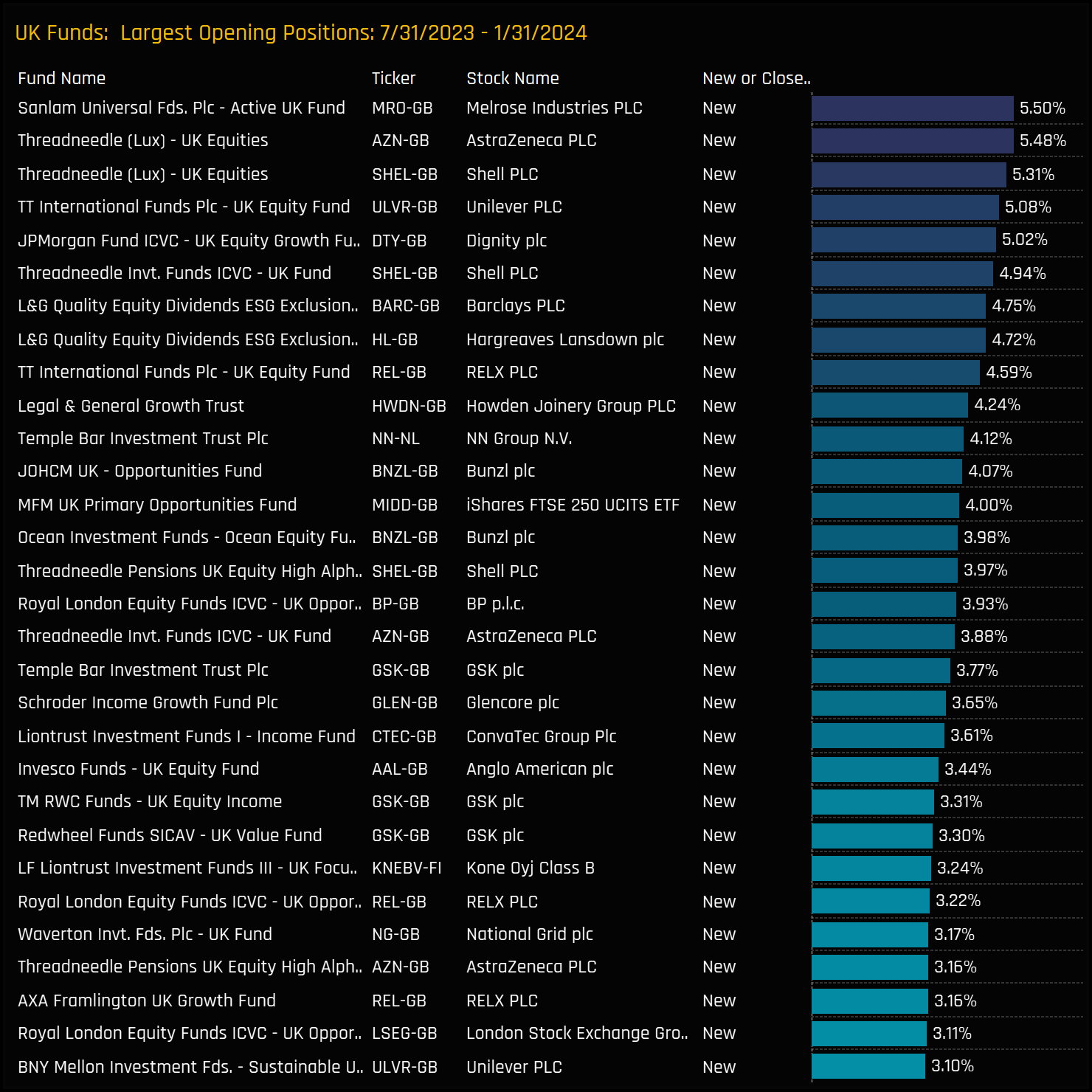

Largest Fund Level New Positions

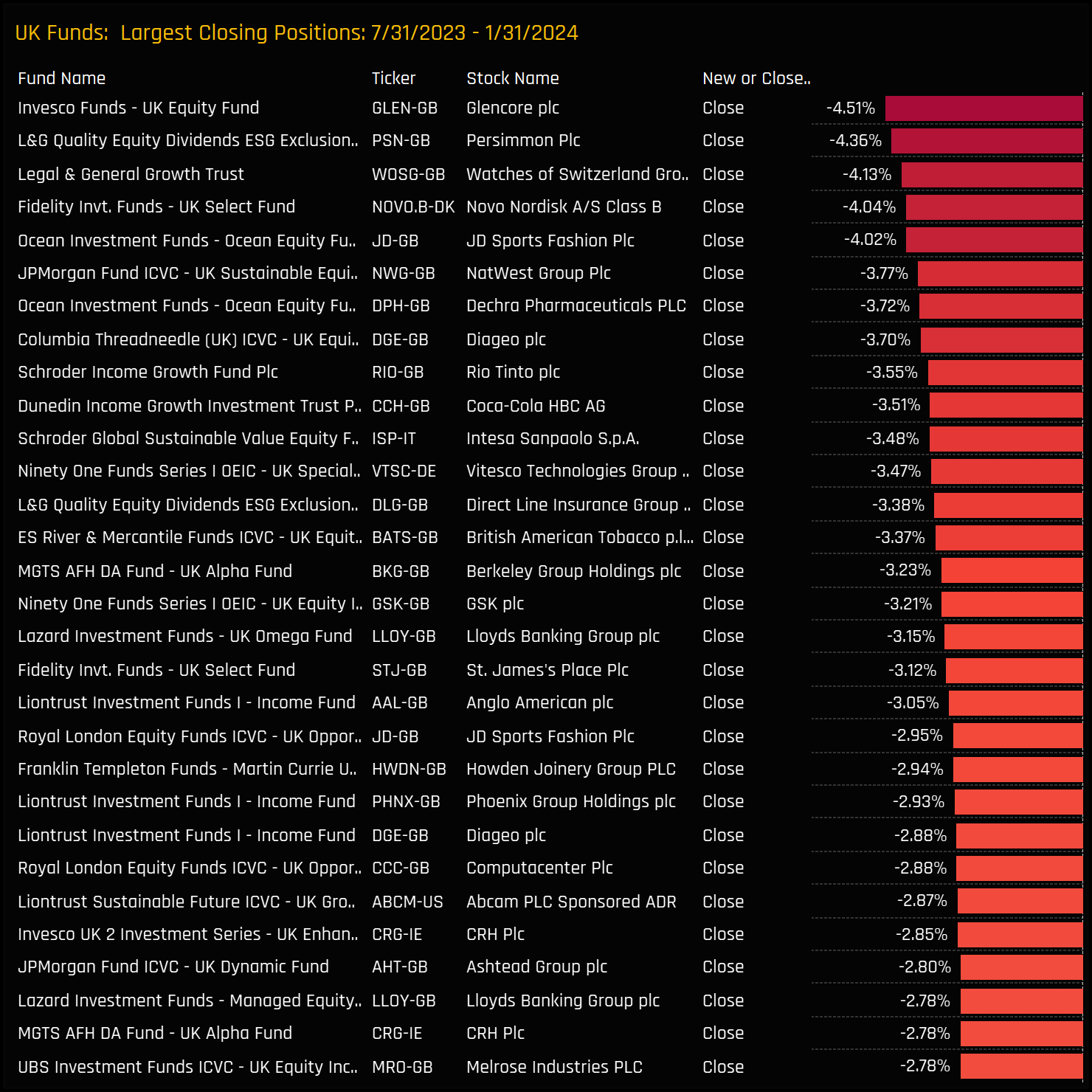

Largest Fund Level Closed Positions

270 UK Equity Funds, AUM $190bn

UK Equity Fund Positioning Report

Click on the link below for the full data report on fund positioning among the 270 UK funds in our analysis.

For more analysis, data or information on active investor positioning in your market, please get in touch with me on steven.holden@copleyfundresearch.com

{kind=link}