20 February

GEM Insights

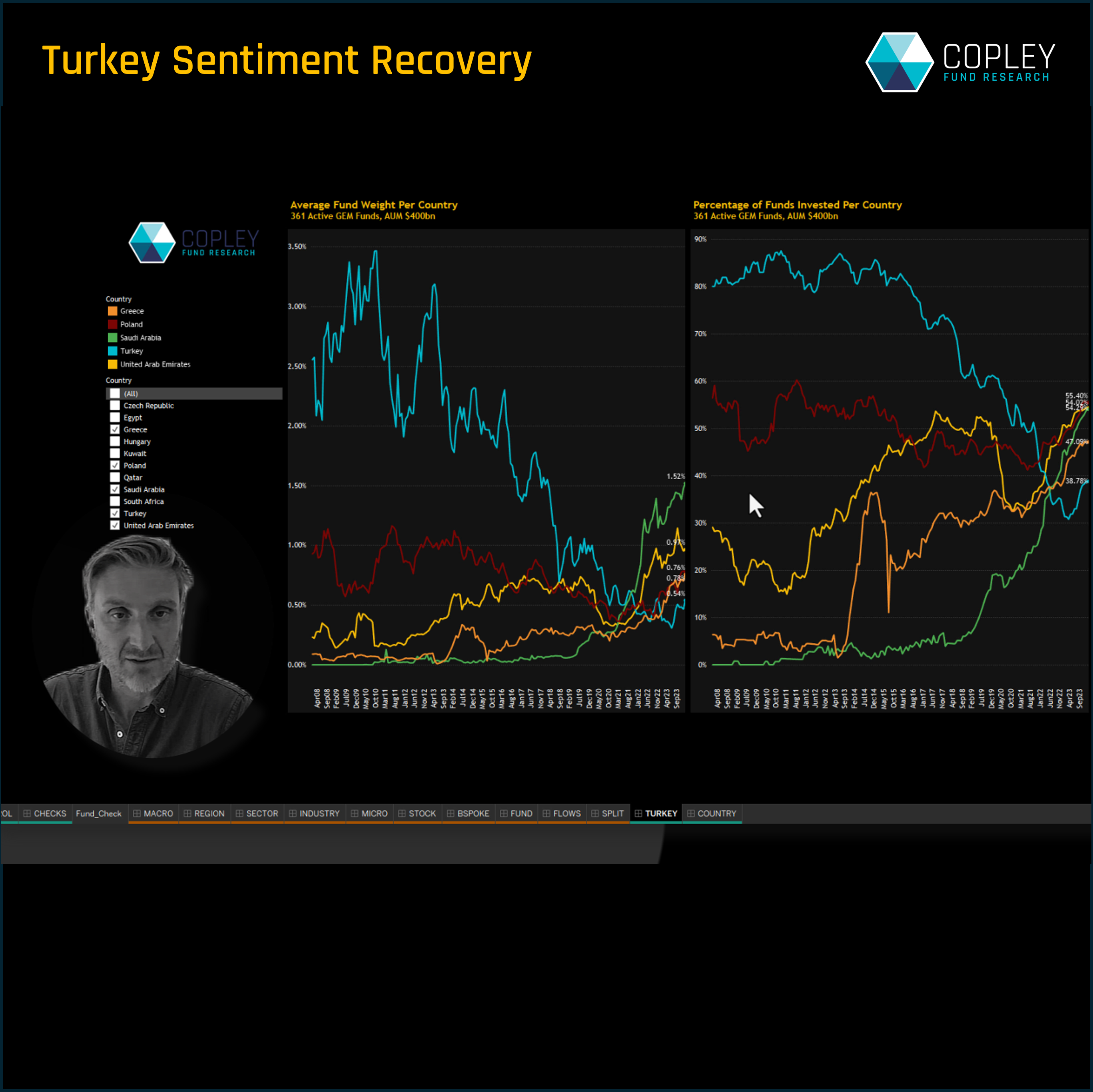

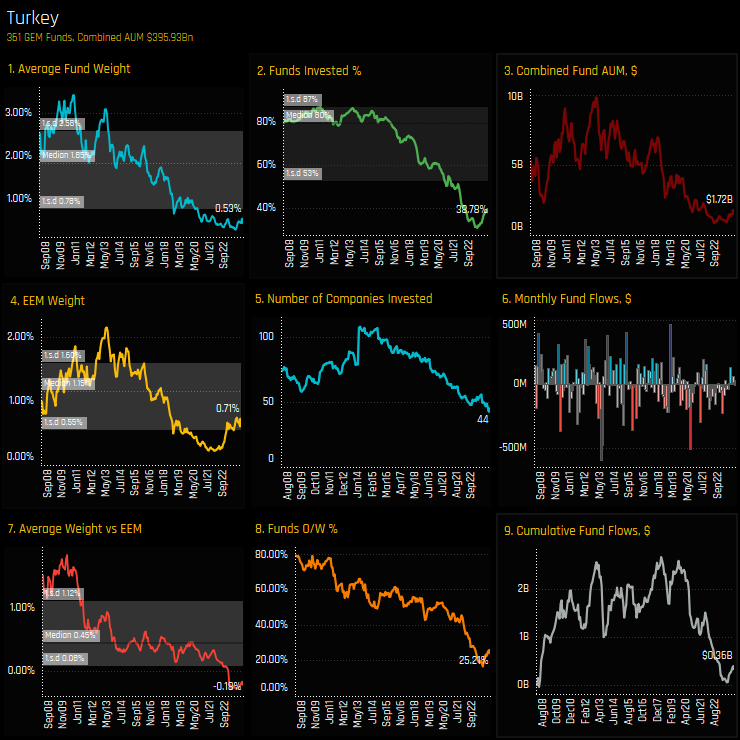

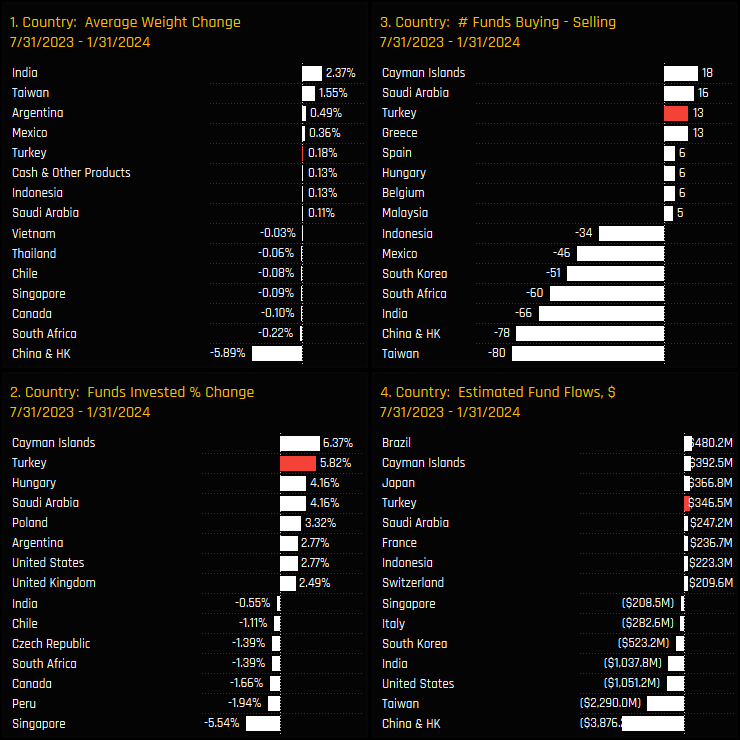

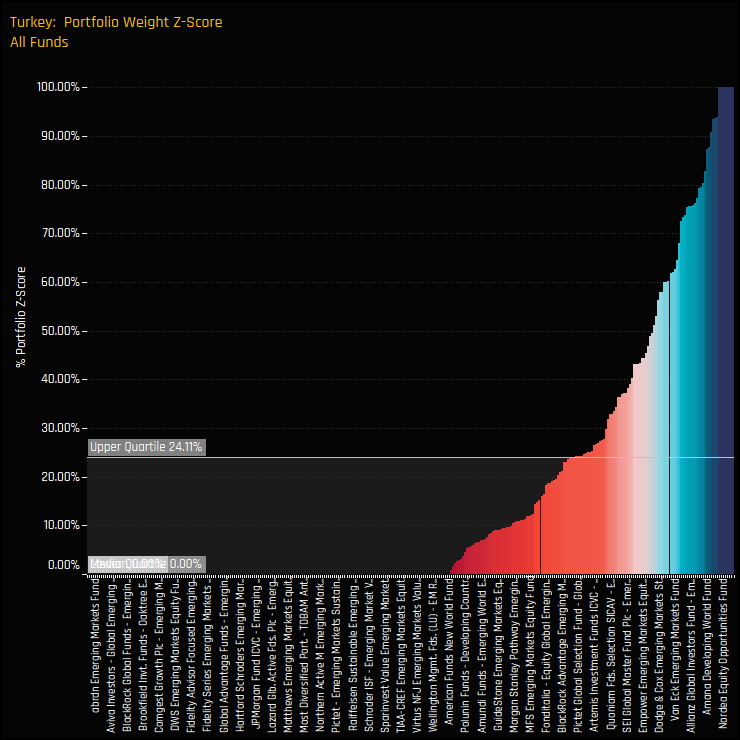

Reassessing Turkey: EM Fund Managers Show Signs of Sentiment Shift

- Steve Holden

- 0 Comments

Related Posts

{kind=link}