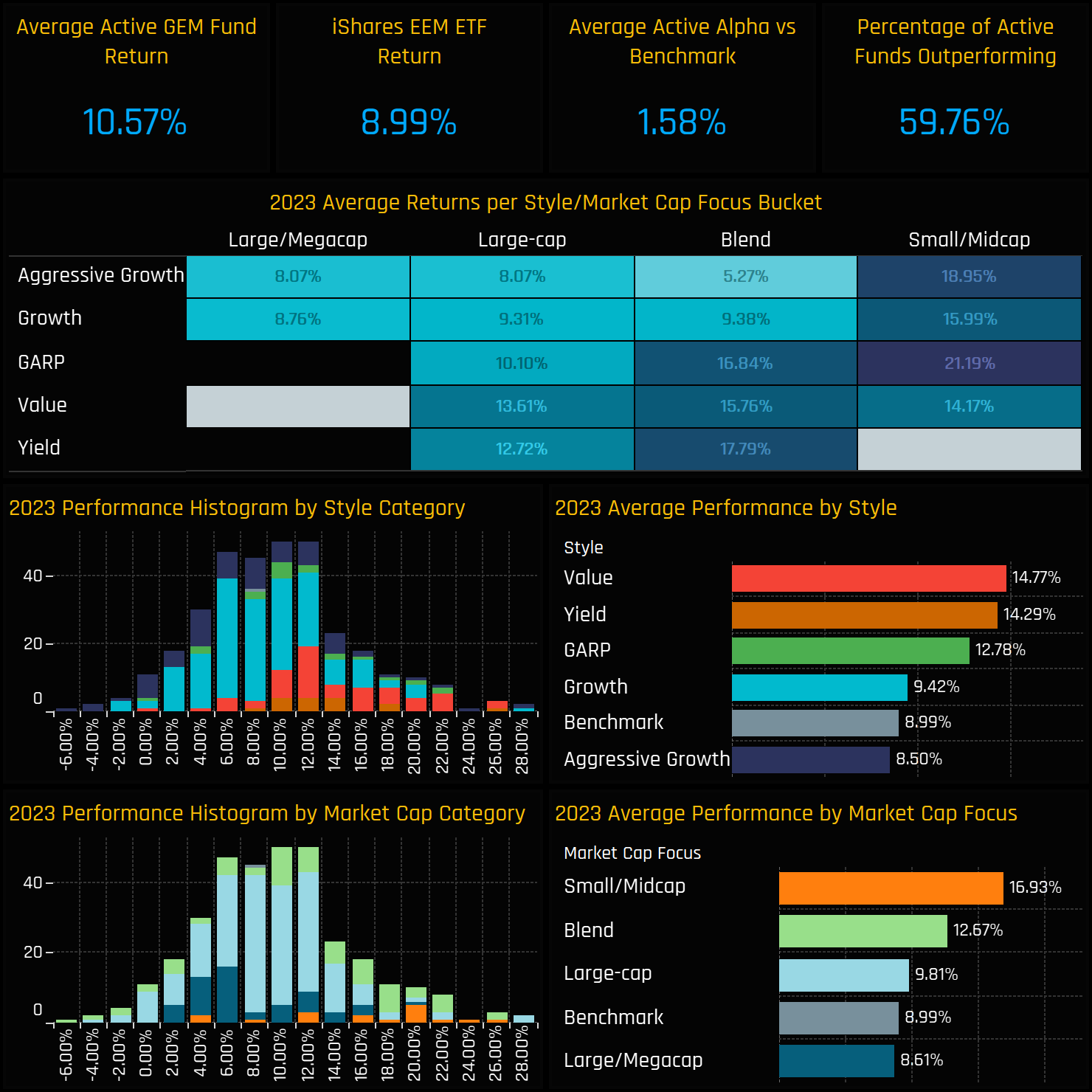

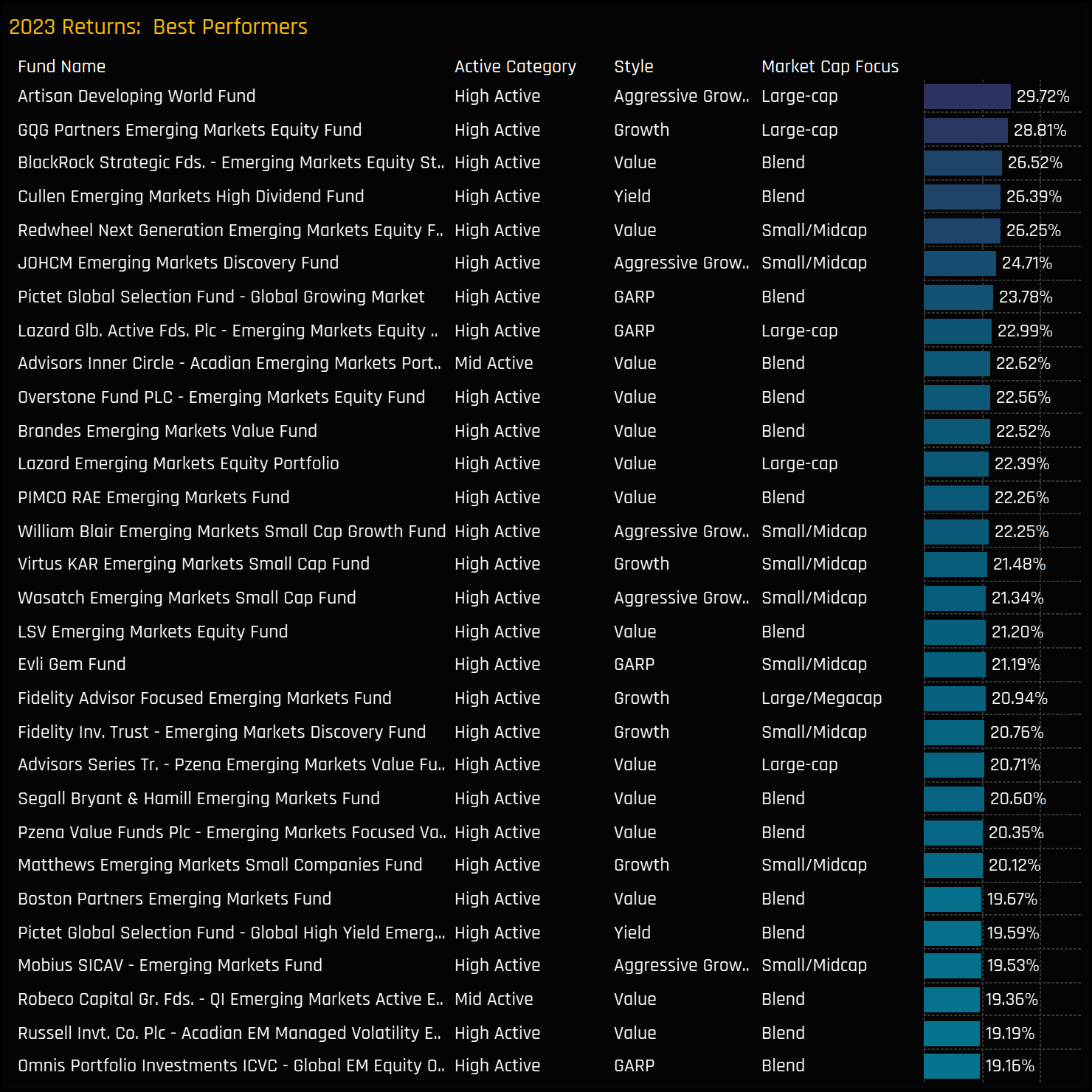

Active EM funds had a good 2023. Average fund returns came in at a healthy 10.57%, ahead of the iShares MSCI Emerging Markets ETF by +1.58%, with 59.8% of funds outperforming. Broken down by Style, Value and Yield funds had the best year, averaging 14.77% and 14.29% respectively, with Aggressive Growth funds the only group to underperform the iShares MSCI EM return. From a Market Cap perspective, Small/Midcap funds were ahead by some margin, with 16.9% average returns compared to 8.6% for Large/Megacap. Across all funds, the core of the return distribution was between 6% and 12% on the year.

{kind=link}