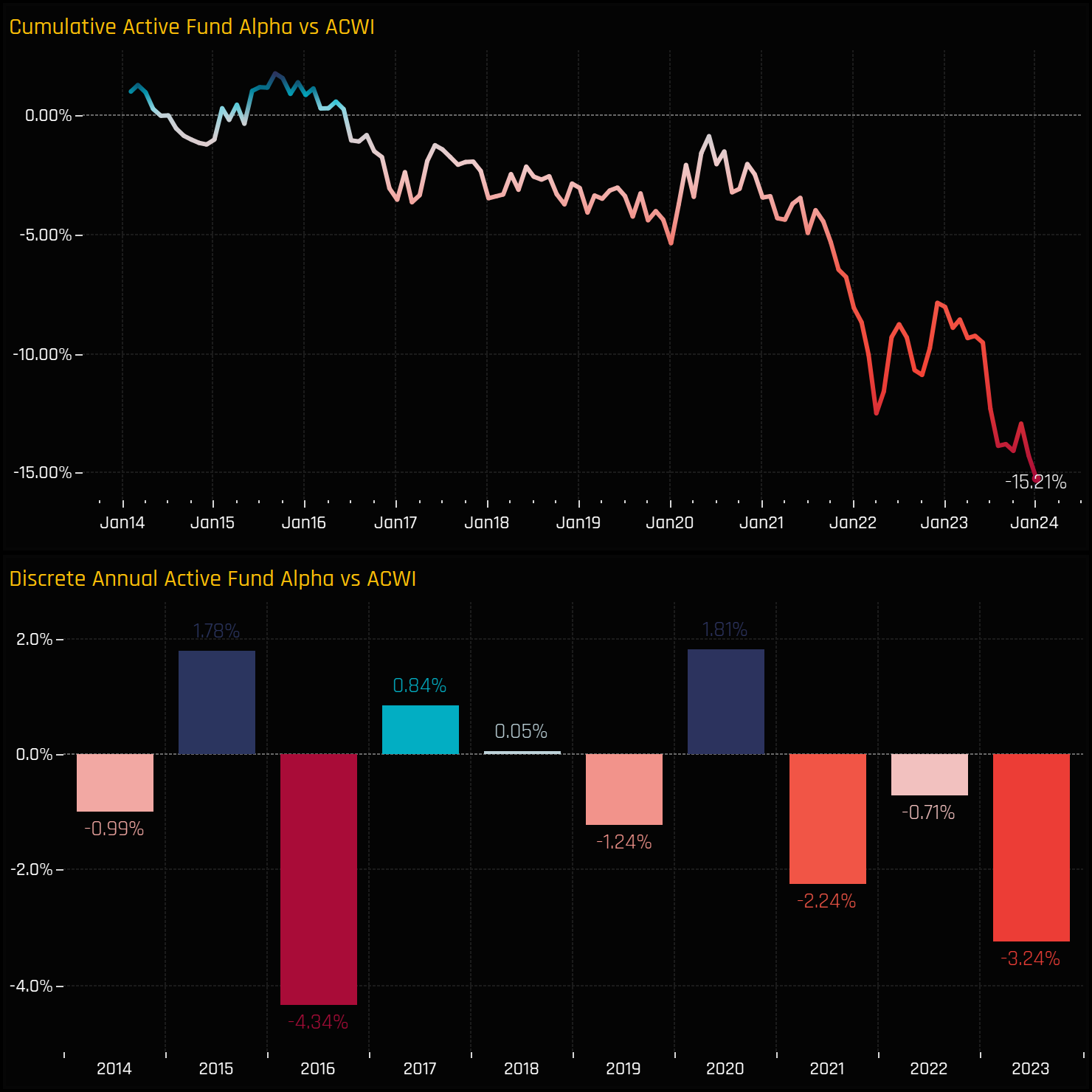

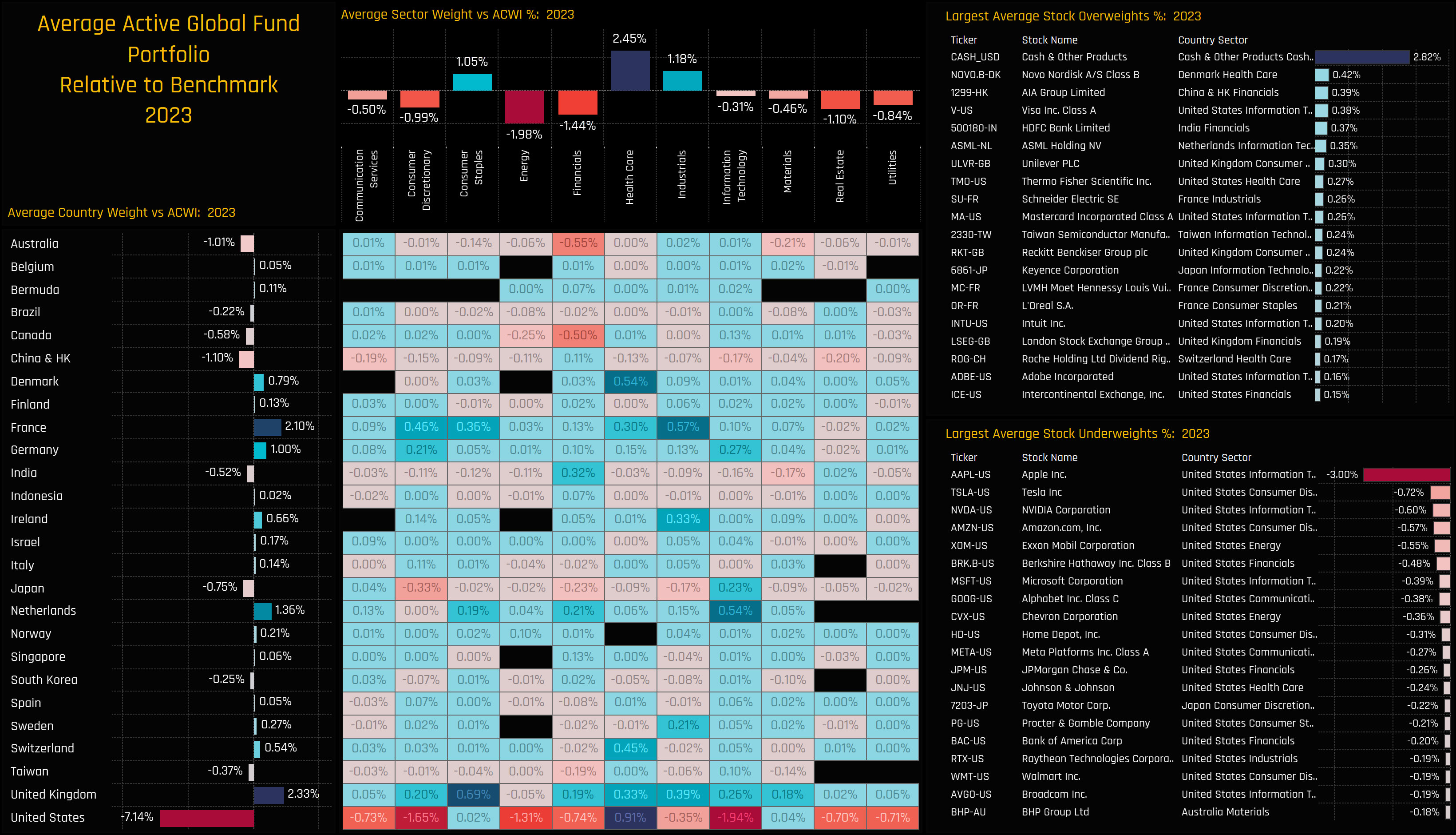

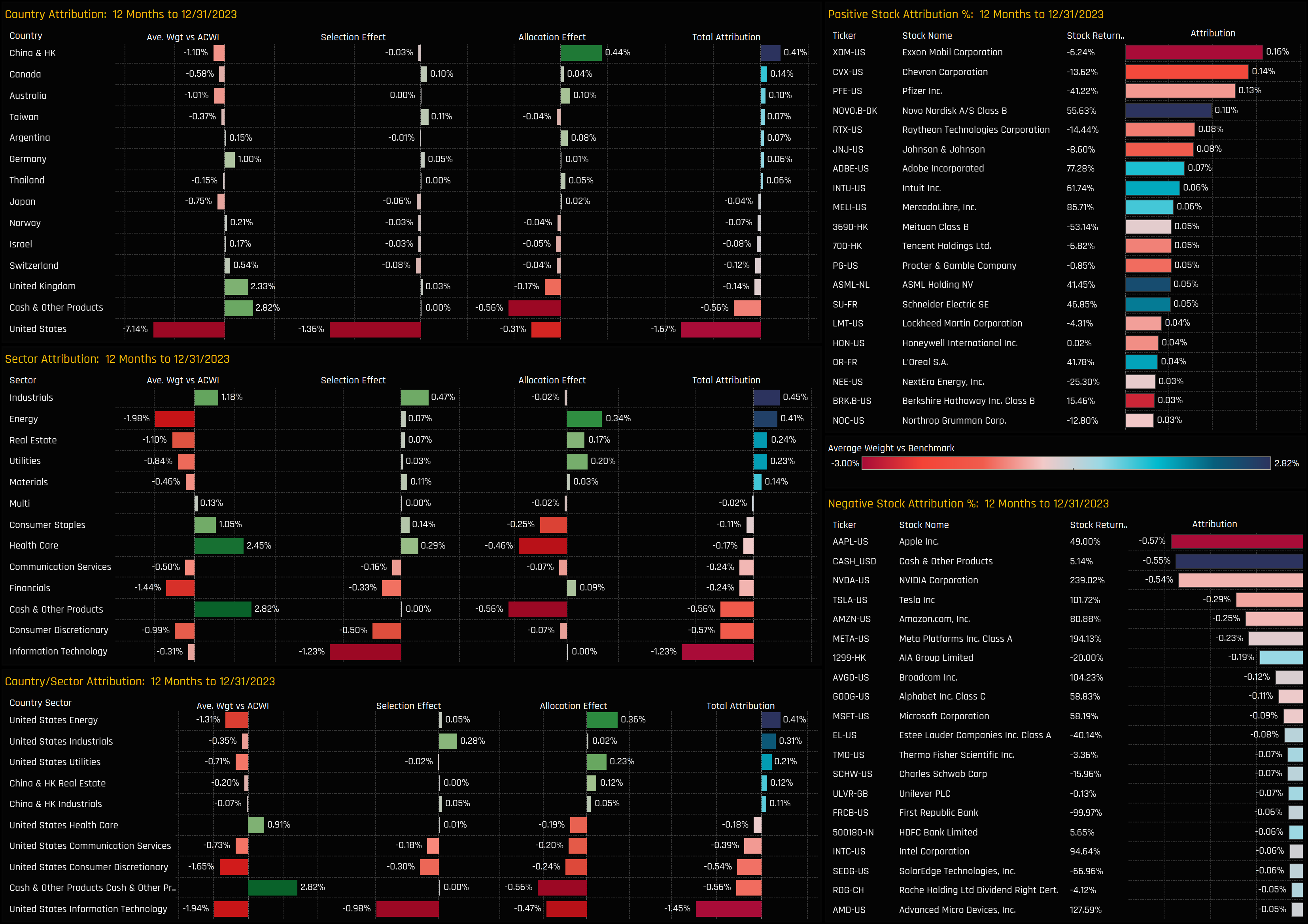

Our attribution analysis compares this portfolio against a benchmark represented by the SPDRs MSCI ACWI ETF. Consistent with the overall fund underperformance in 2023, the portfolio lagged by -1.67%. A critical factor in last year’s underperformance was positioning in the United States. The underweight position in the U.S. market dragged on relative returns, and poor stock selection further exacerbated the issue. A detailed summary of the key factors contributing to this underperformance is provided below.

{kind=link}