19 December

GEM Insights

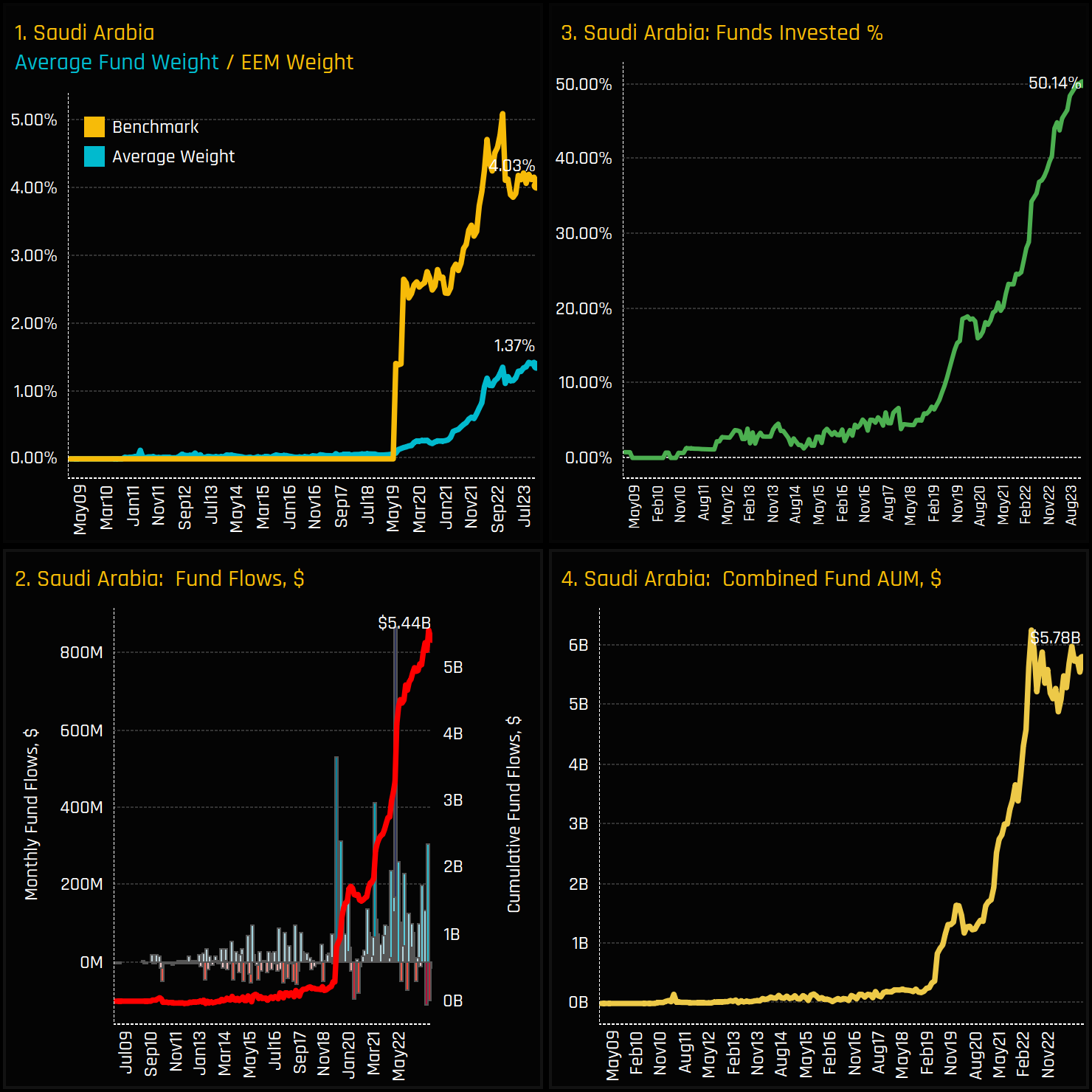

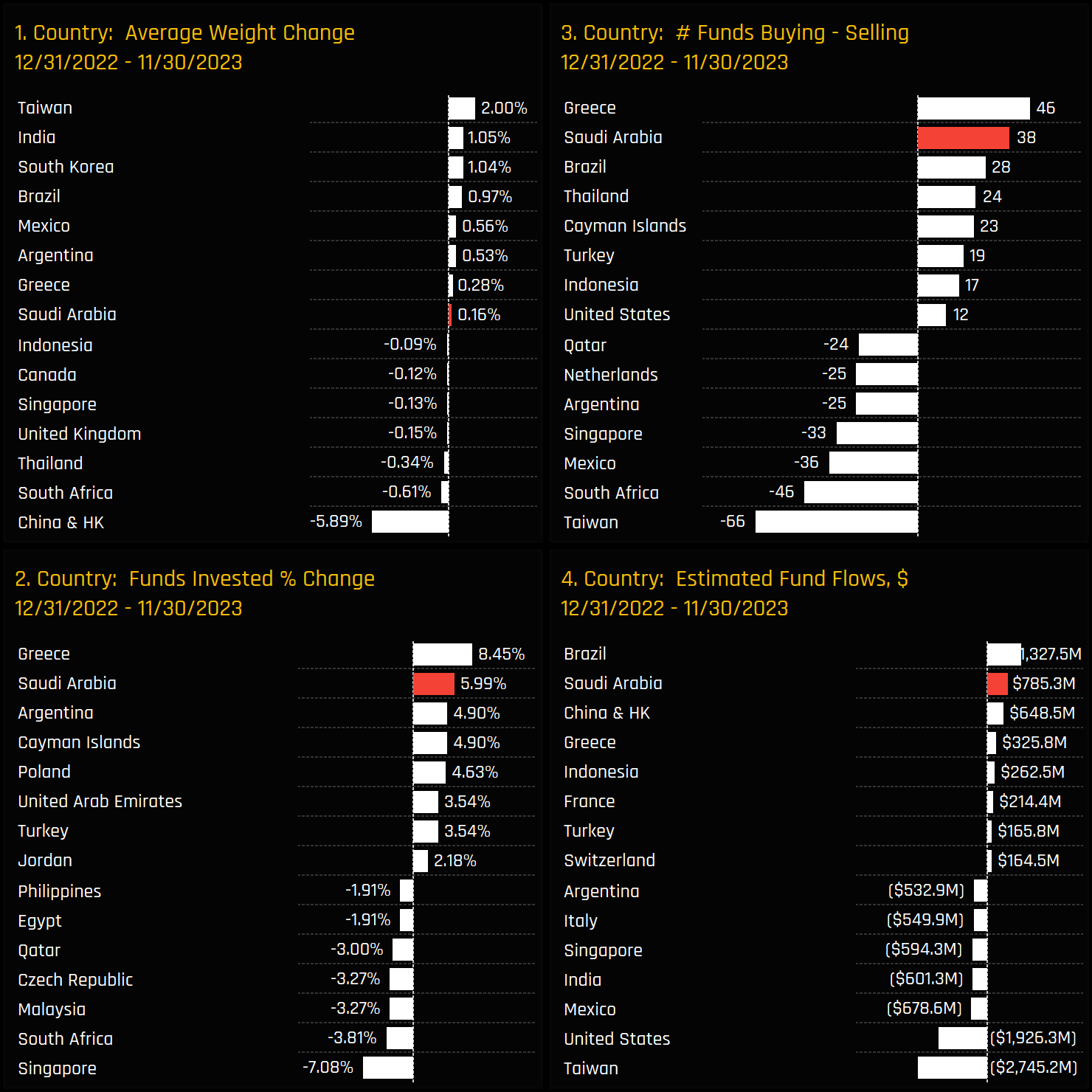

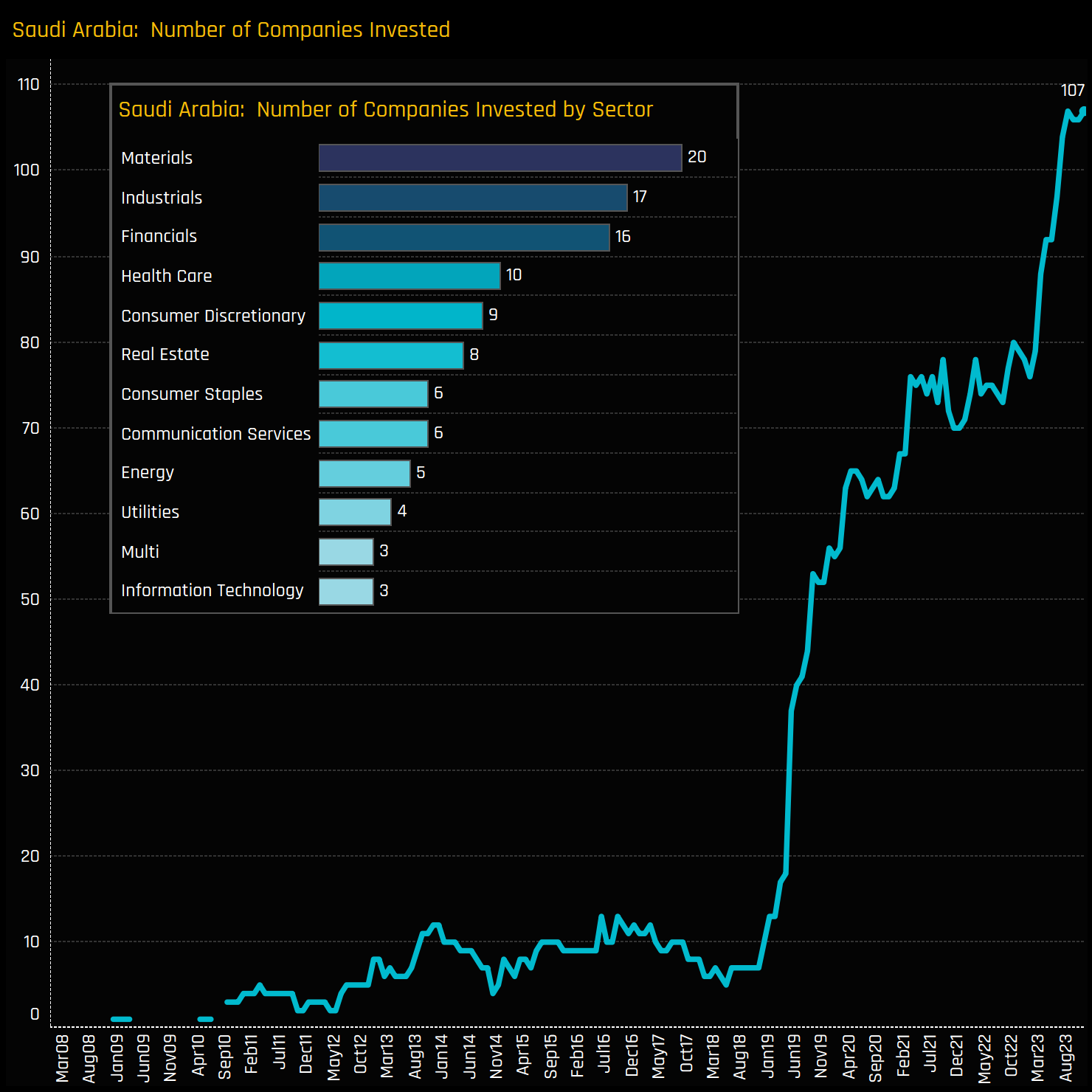

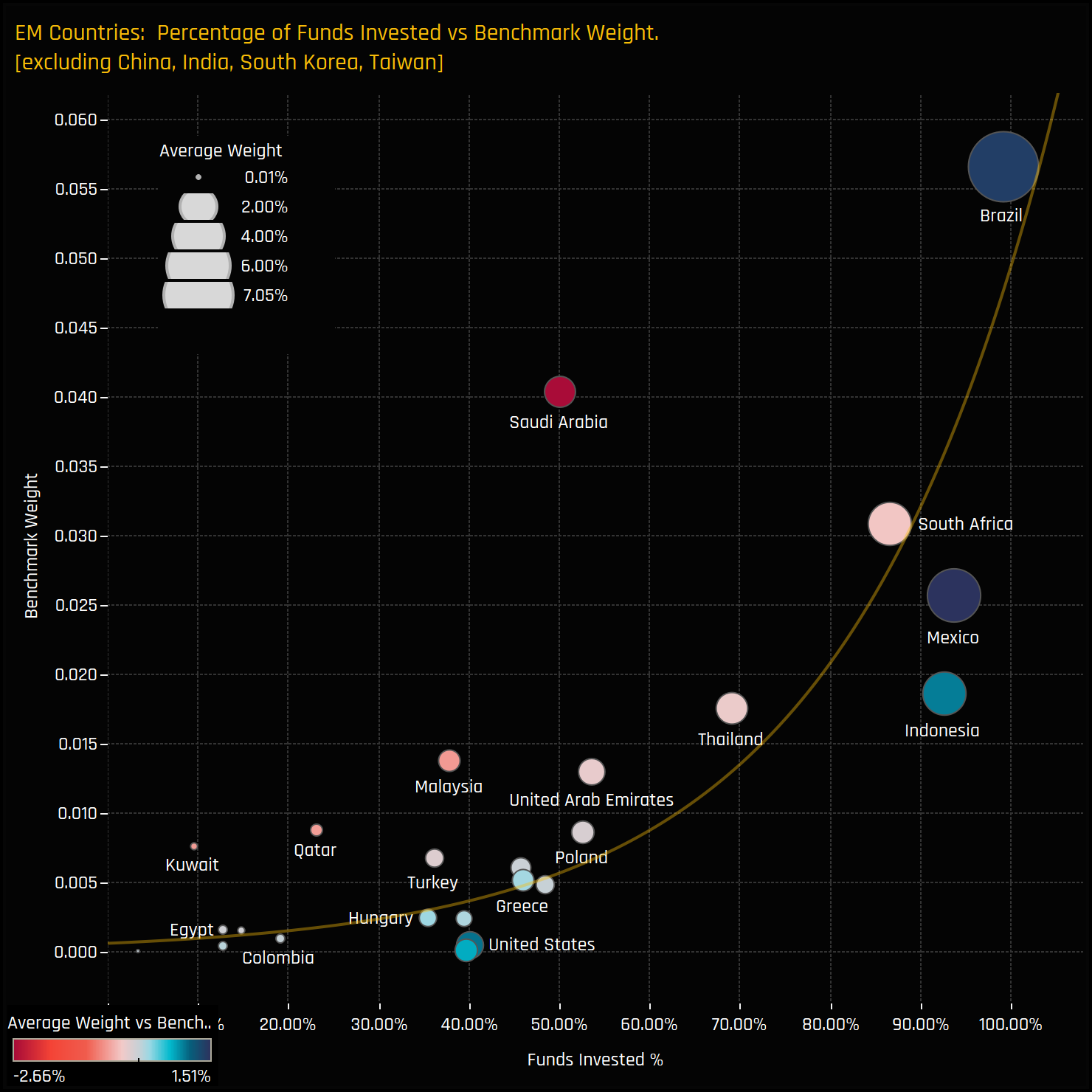

Saudi Arabia Special Report: A Tipping Point in EM Equity Allocations

- Steve Holden

- 0 Comments

Related Posts

{kind=link}