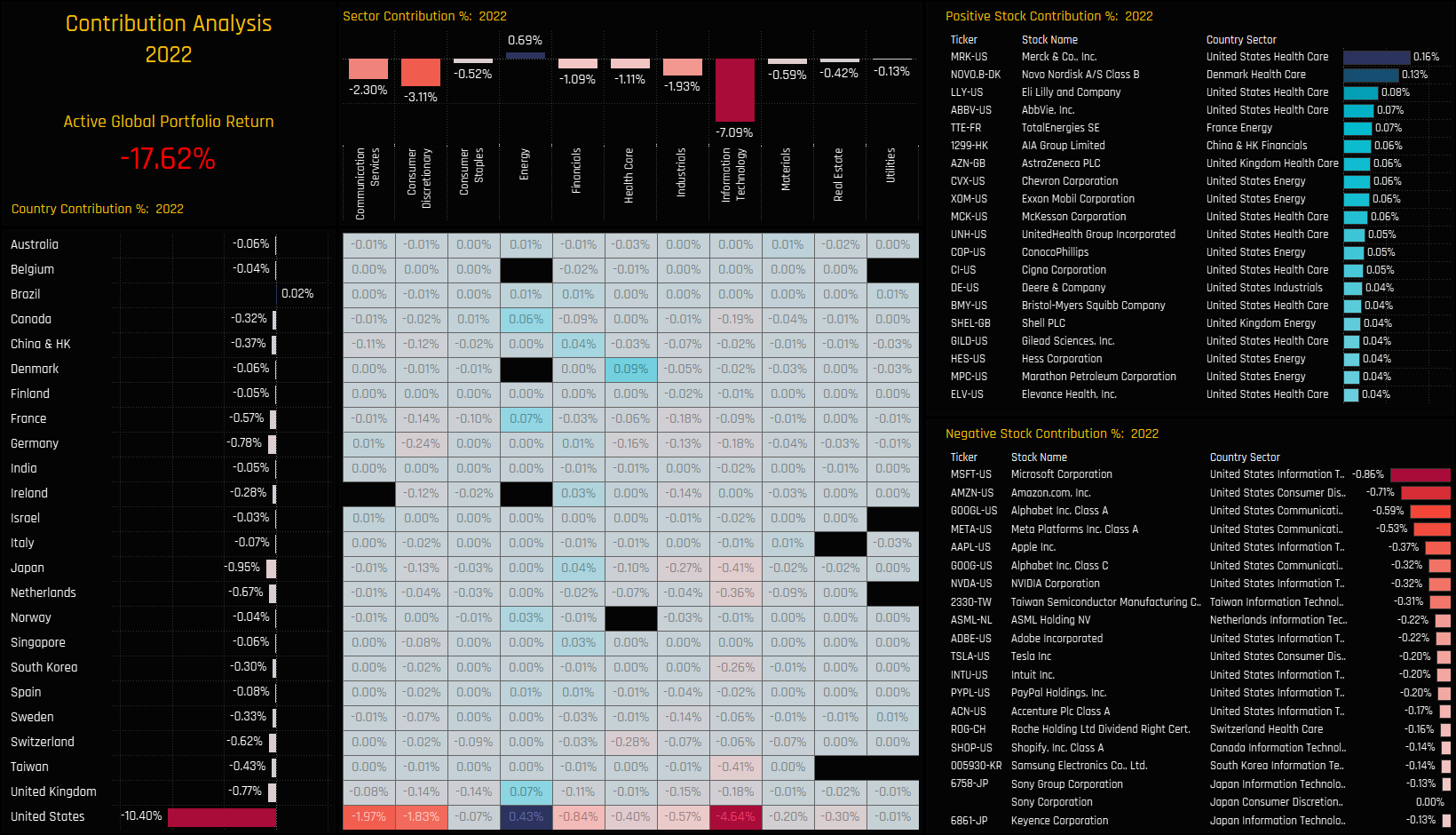

We now look at the drivers behind last year’s absolute and relative performance. We do this by creating a portfolio based on the average allocations of the 359 active strategies in our analysis. This theoretical portfolio, with no fees and based on monthly holding observations returned -17.62% on the year. On a country level, -10.4% of that was driven by US holdings and a further -4.36% from the combined European nations. On a sector level, all sectors except Energy produced negative returns on the year, led by Tech (-7.09%), Consumer Discretionary (-3.11%) and Communication Services (-2.30%). On a stock level, the major stock winners came from the Health Care sector, led by Merck & Co, Novo Nordisk and Eli Lilli and Company, whilst US Megacap stocks provided a severe dent on yearly performance.

{kind=link}