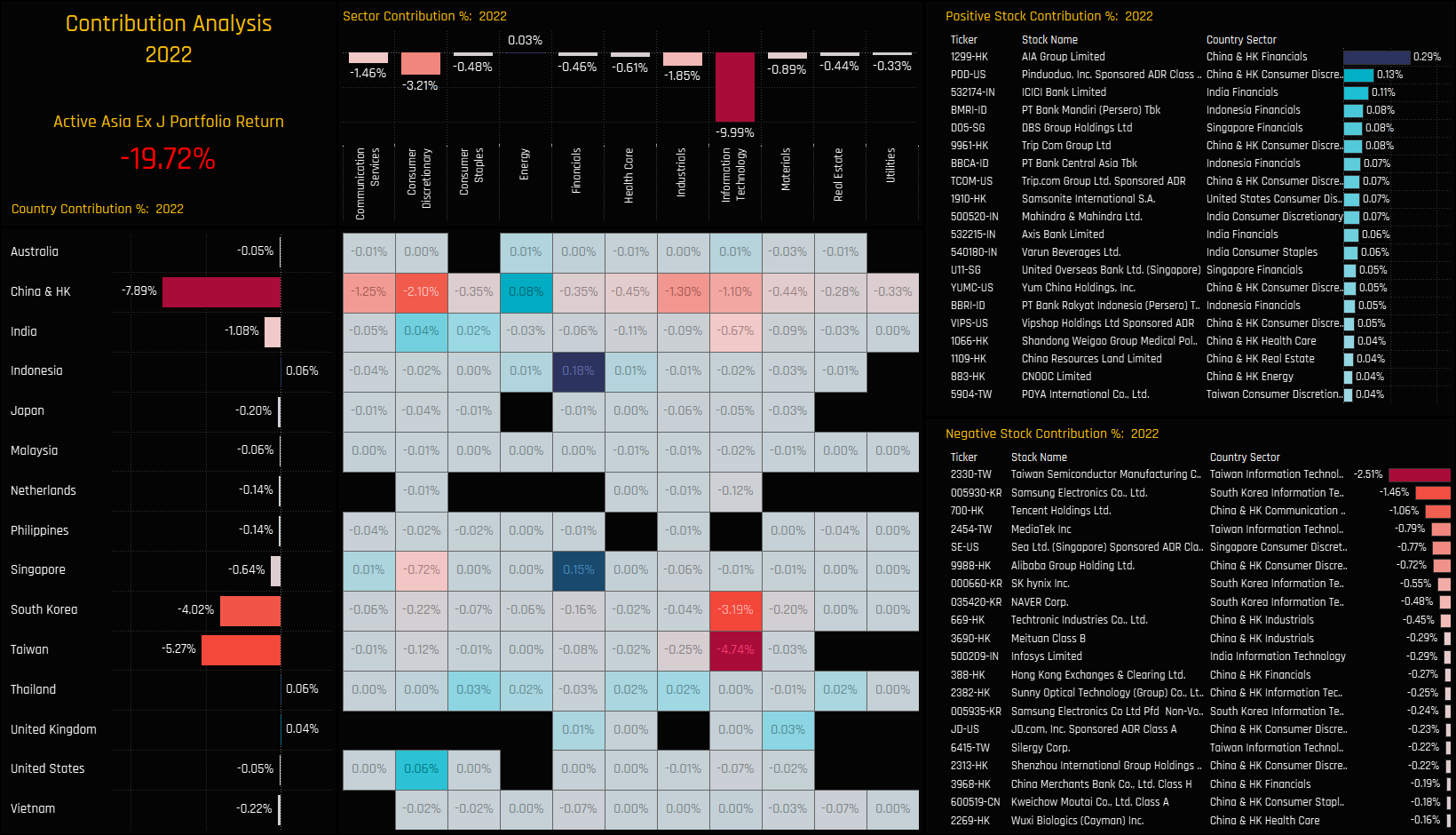

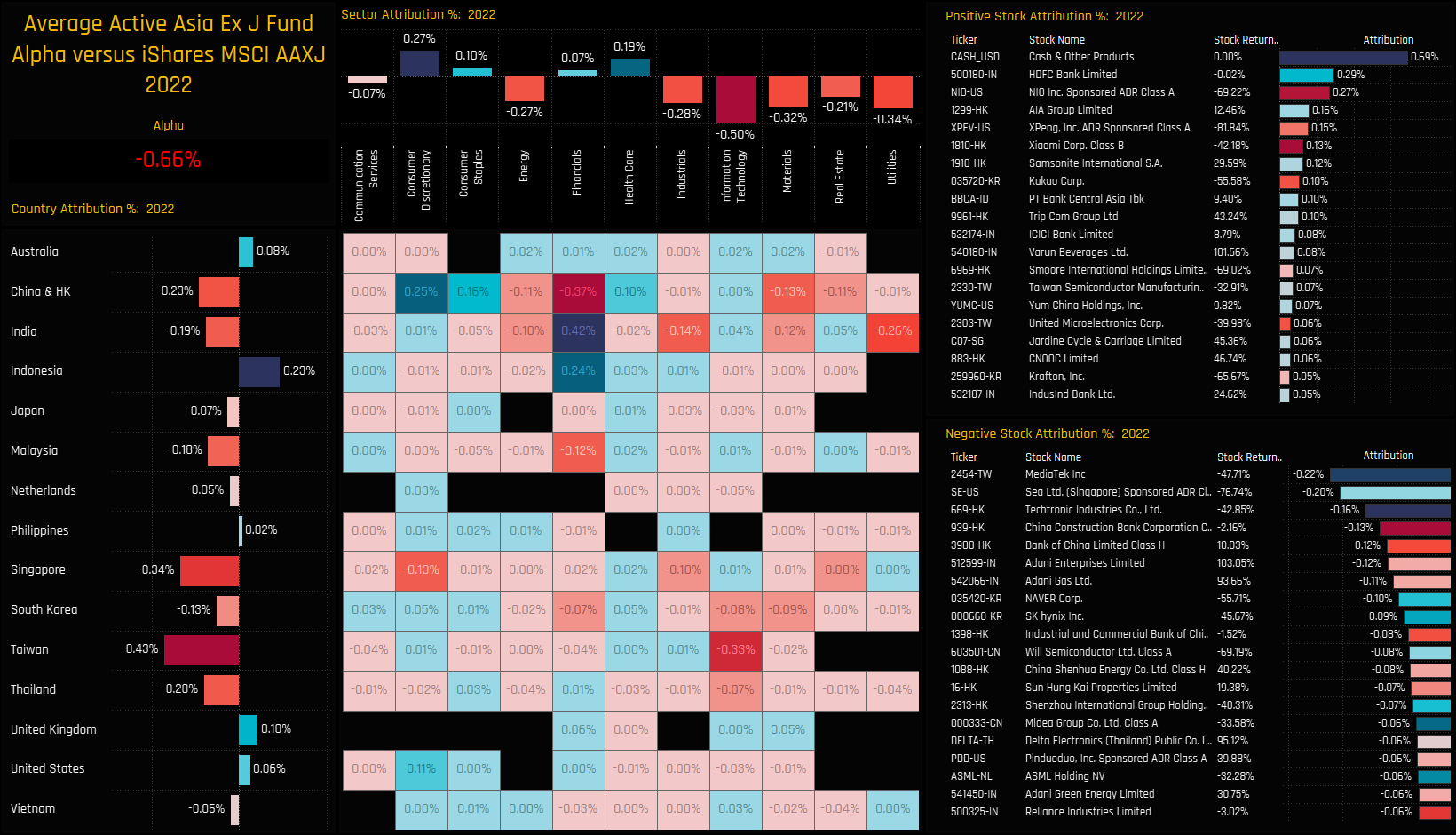

We now look at the drivers behind last year’s absolute and relative performance. We do this by creating a portfolio based on the average allocations of the 91 active strategies in our analysis. This theoretical portfolio, with no fees and based on monthly holding observations returned -19.72% on the year. On a country level, -7.9% of that was driven by China & HK holdings and a further -9.3% from Taiwan and South Korea combined. On a sector level, all sectors except Energy produced negative returns on the year, led by Tech (-9.99%), Consumer Discretionary (-3.21%) and Industrials (-1.85%). On a stock level, TSMC was the major drag on performance, contributing -2.52% in negative returns for the portfolio, in addition to Samsung Electronics (-1.46%) and Tencent Holdings (-1.06%).

{kind=link}