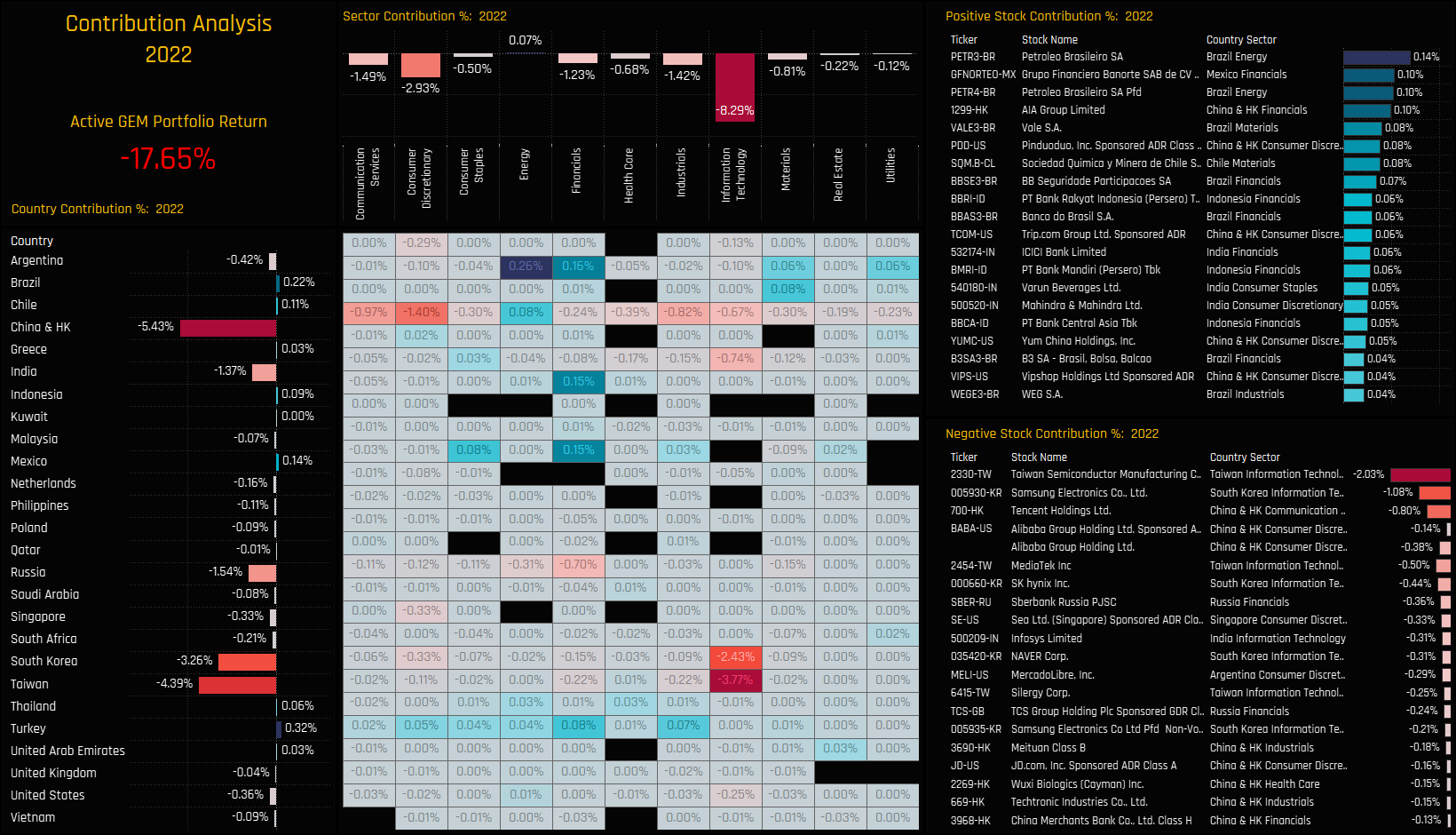

We now look at the drivers behind last year’s absolute and relative performance. We do this by creating a portfolio based on the average allocations of the 276 active strategies in our analysis. This theoretical portfolio, with no fees and based on monthly holding observations returned -17.65% on the year. On a country level, -5.43% of that was driven by China & HK holdings followed by Taiwan (-4.39%) and South Korea (-3.26%). Russia contributed -1.54%. On a sector level, all sectors except Energy produced negative returns on the year, led by Tech (-8.29%), Consumer Discretionary (-2.93%) and Communication Services (-1.49%). On a stock level, the major stock winners came from South America, India and ASEAN, with Petrobras, Grupo Financiero Banorte and PT Bank Rakyet contributing positively over the year. The big detractors were large holdings in underperformers TSMC, Samsung Electronics, Tencent and Alibaba Group Holdings.

{kind=link}