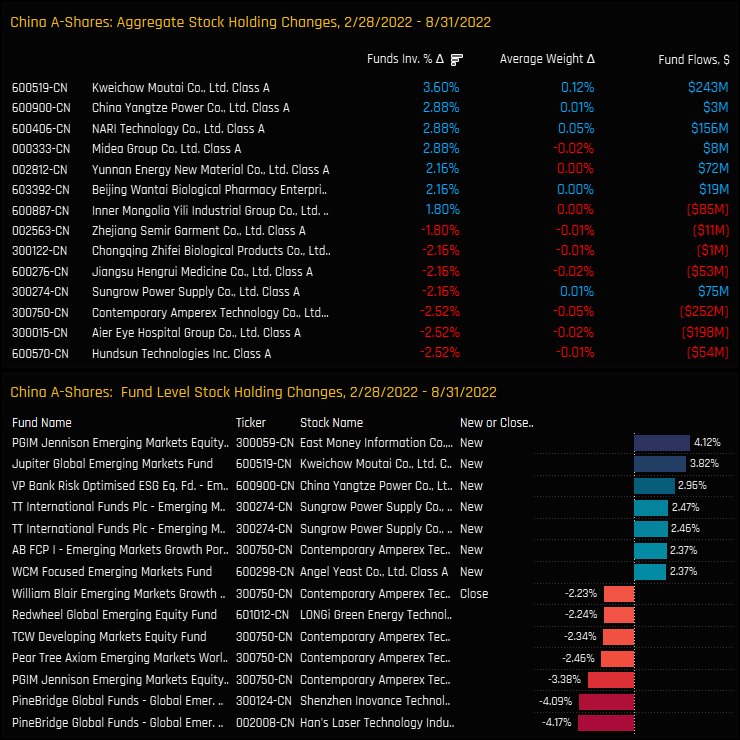

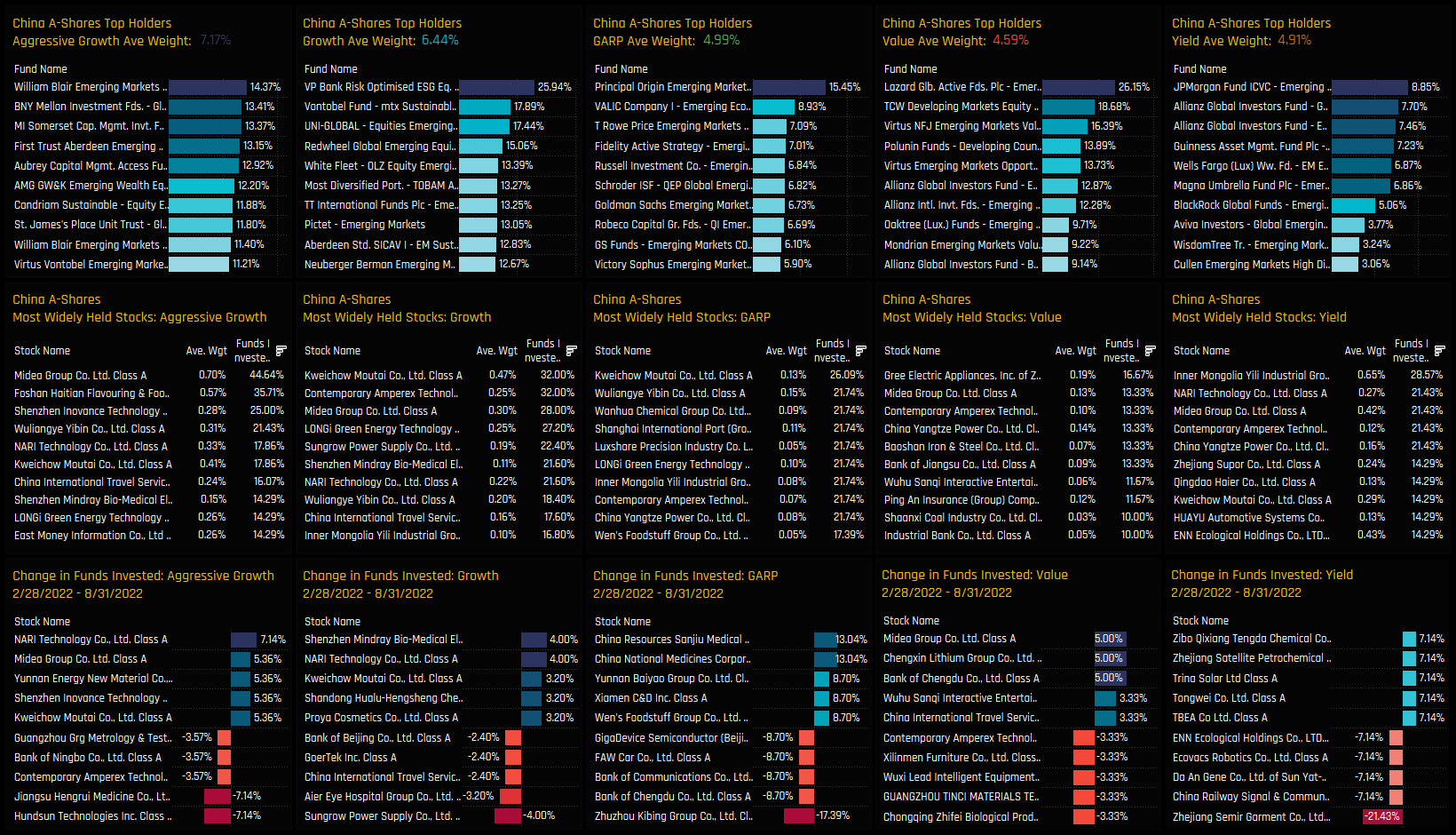

Split by Style, Midea Group is a top 3 holding for Aggressive Growth, Growth, Yield and Value investors, though largely avoided by GARP. Yield investors prefer Inner Mongolia Yili Industries by some margin, whilst Value funds place a greater weight on Gree Electric Appliances. Shenzhen Inovance Technology and Foshan Haitian Flavouring are well held by Aggressive Growth managers, but avoided elsewhere.

{kind=link}