Singapore Financials: Surging Higher

China Technology: Stalling Sentiment

Asian Restaurant Boom

Singapore Financials: Surging Higher

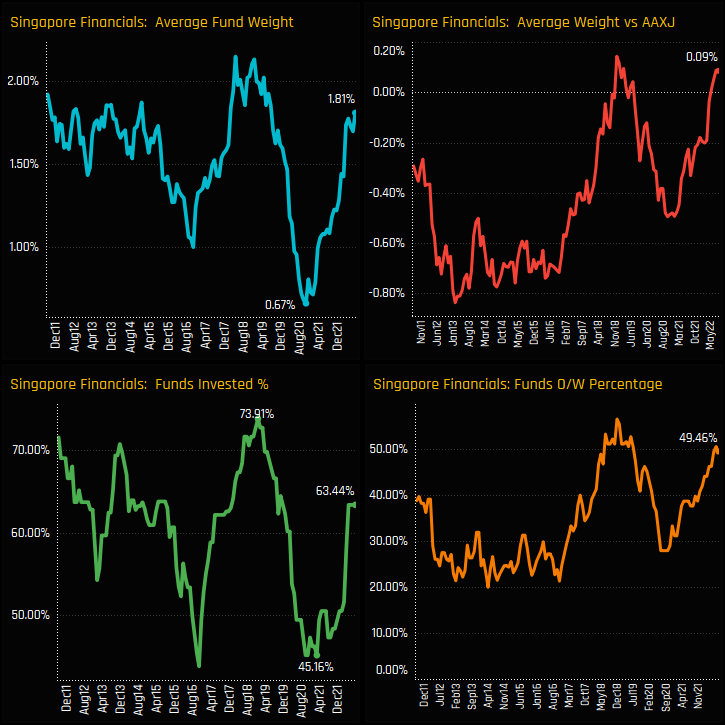

Allocations in Singapore Financials continue their cyclical turnaround. From a low of 0.67% in early 2021, average holding weights have soared to 1.81%, closing in on the highs of 2%+ through 2018 with managers moving from underweight to overweight in the process. This has been an active rotation, with the percentage of managers exposed to the sector increasing from 45.2% in 2021 to 63.4% today.

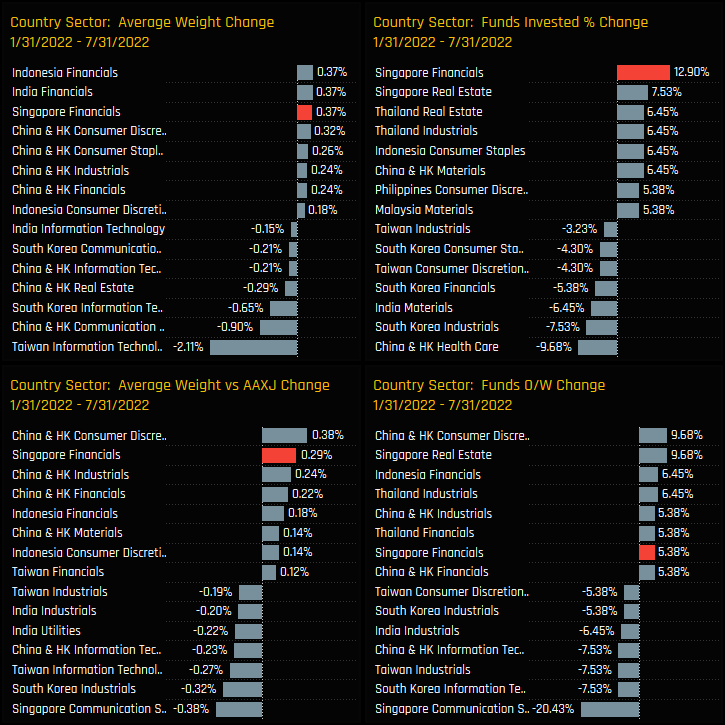

Versus sector peers, Singapore Financials have been one of the key beneficiaries of manager rebalancing over the last 6-months, with a 12.9% increase in funds invested the most of any country sector, and all 4 measures of ownership moving higher.

Fund Holdings, Style & Activity

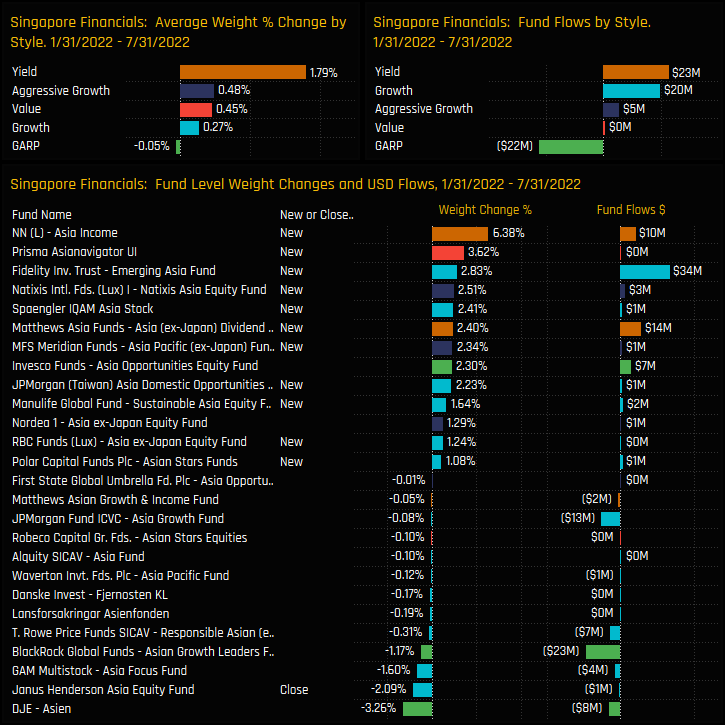

The chart below shows the fund level detail behind the aggregate increases in exposure. Activity between the filing dates of 01/31/2022 and 07/31/2022 is hugely skewed to the buy side, led by opening positions from NN Asia Income (+6.38%) and Prisma Asianavigator (+3.62%) and a mixture of funds from different style groups adding exposure over the period.

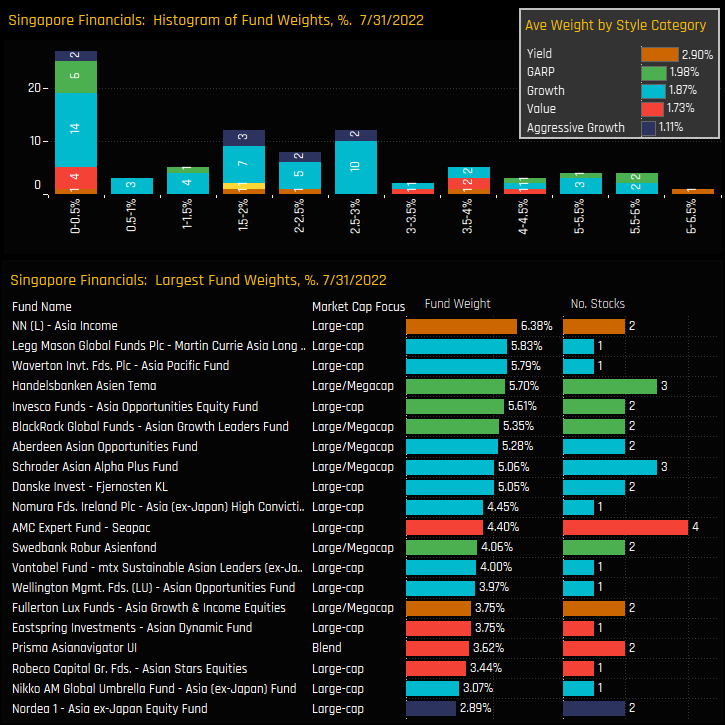

Split by Style, Yield managers are the largest allocators with an average weight of 2.90%, whilst Aggressive Growth are the lowest on 1.11%.. Those that do have exposure tend to hold over 1.5% with a decent base of investors who hold >5% allocations. The overall averages are dragged down by the 27% of funds who hold no exposure at all.

Stock Holdings & Activity

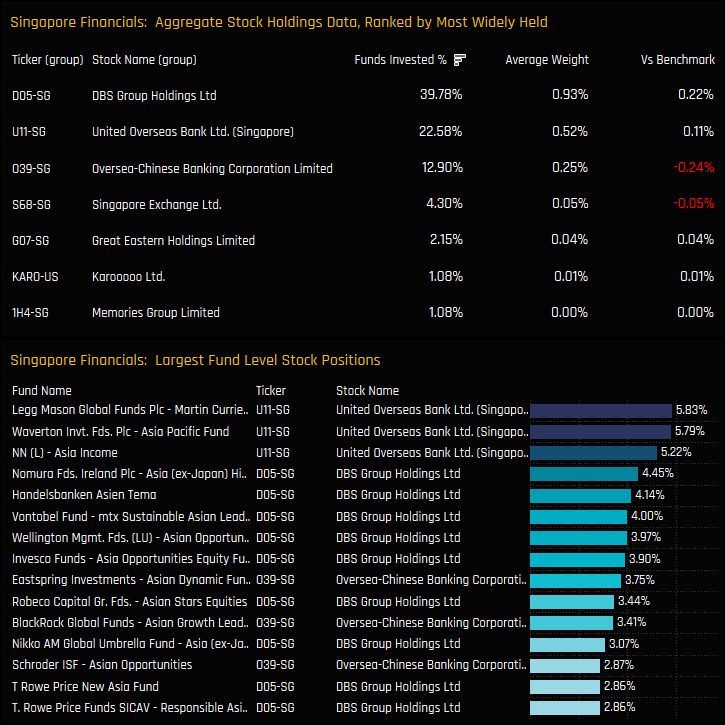

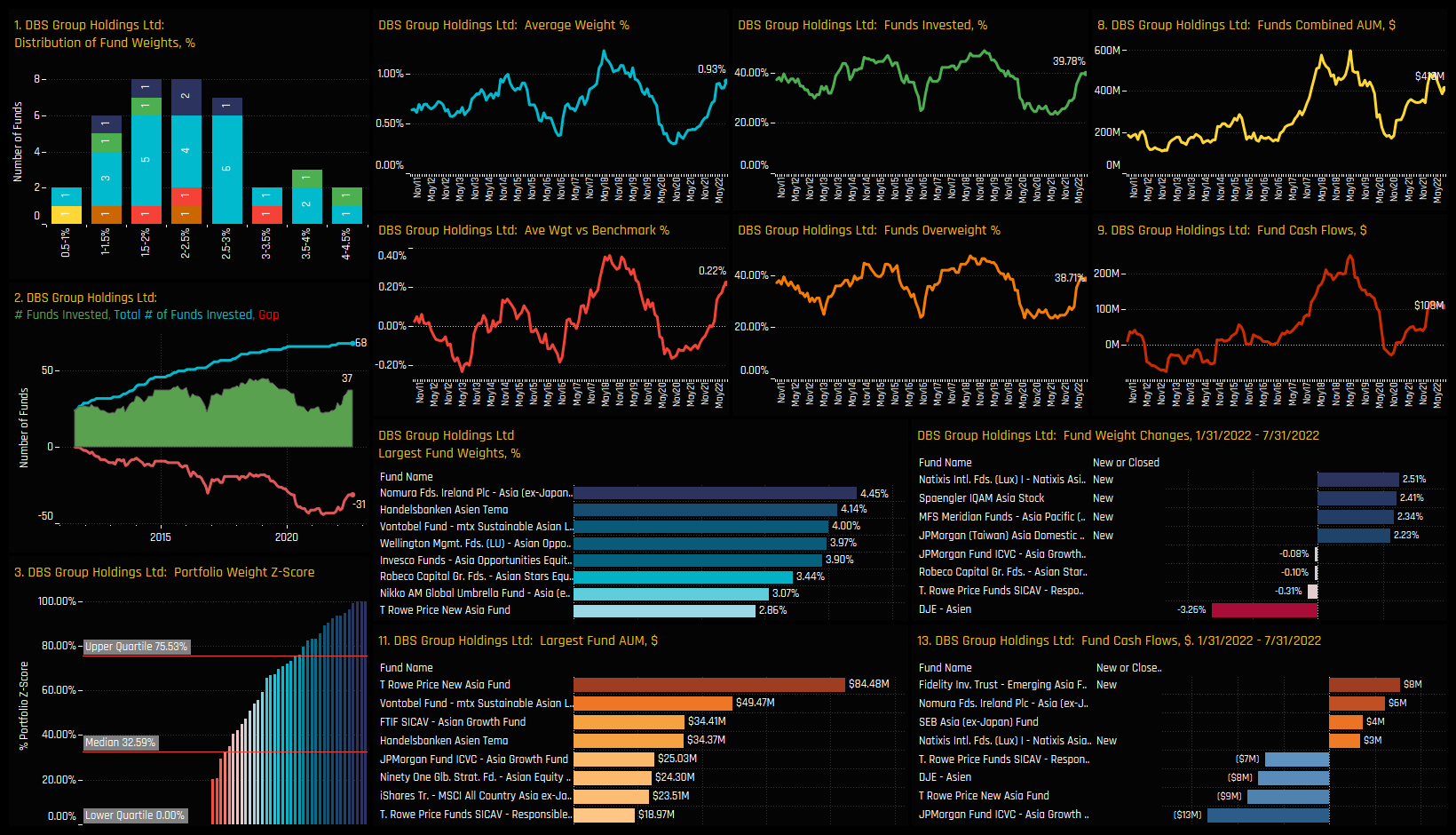

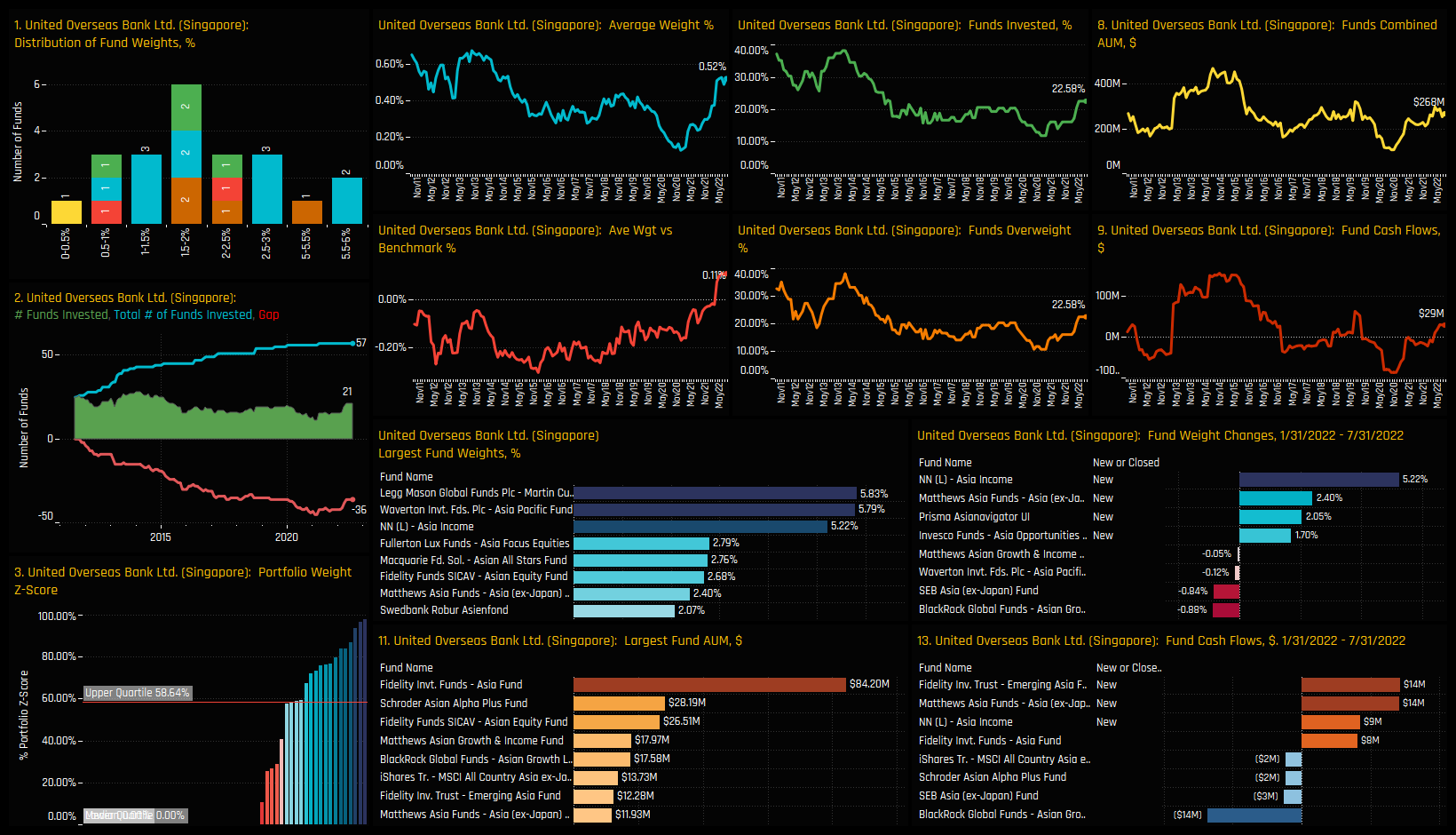

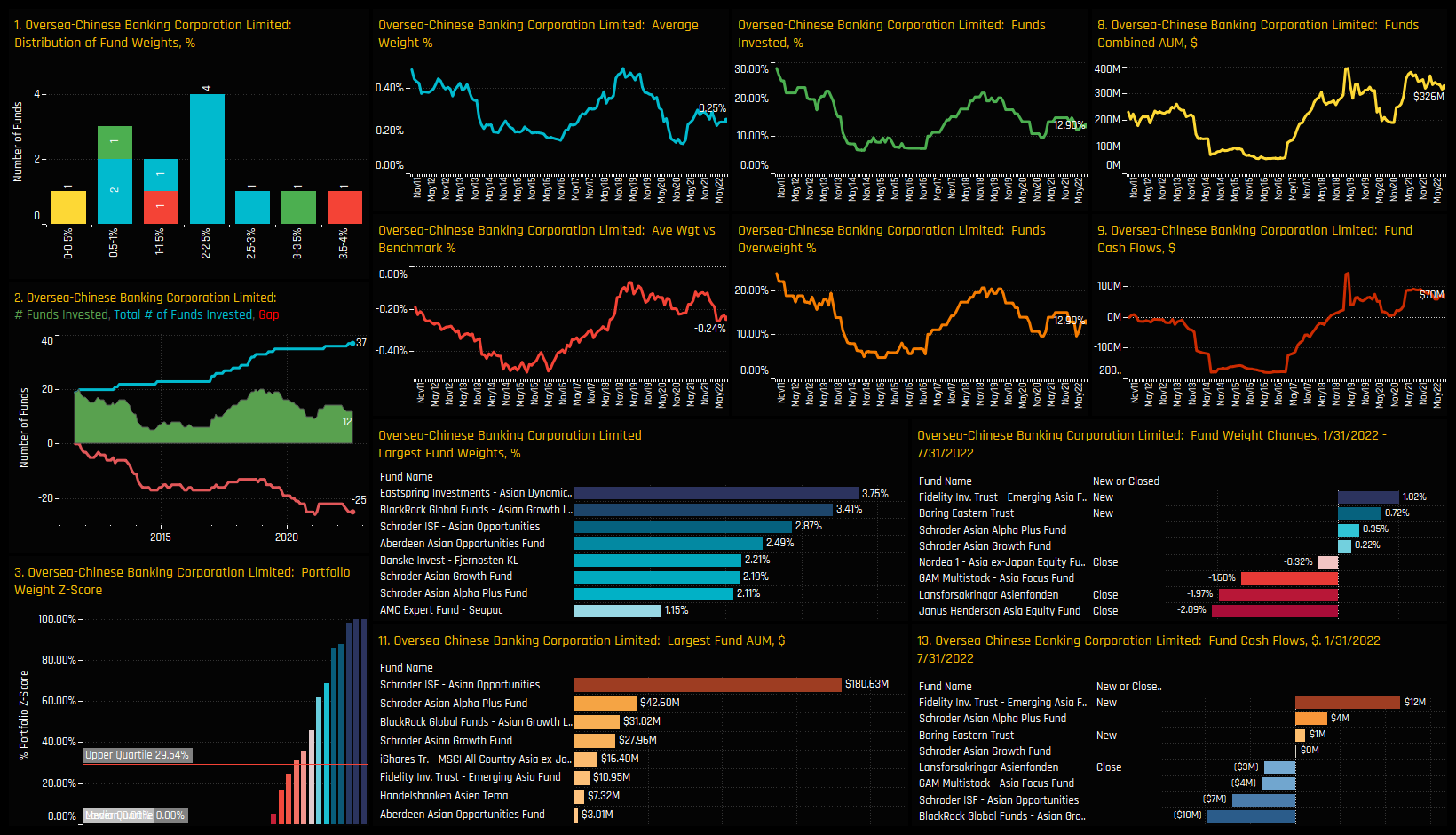

The active Singapore Financials stock universe is comprised of 7 companies, but the top 3 account for the lion’s share of allocations. DBS Group Holdings is the most widely held stock, owned by 39.8% of funds at an average weight of 0.93%, followed by United Overseas Bank Ltd (22.6% of funds) and Oversea-Chinese Banking Corp (12.9%). United Overseas Bank occupies the top 3 high conviction single fund positions, led by Legg Mason (5.83%), Waverton Asia Pacific (5.79%) and NN Asia Income (5.22%).

Activity over the last 6-months shows strong ownership growth in both DBS Group Holdings and United Overseas Bank Ltd, with +10.75% and +6.45% of managers opening positions respectively. Both stocks also account for the largest increases in individual fund level positions across a host of managers. Singapore Exchange also saw ownership rise, whilst Oversea-Chinese Banking Corp saw Landforsakringar Asienfonden and Janus Henderson close out positions over the period.

Conclusions

Sentiment in the Singapore Financials sector has seen a huge reversal. Allocations have recovered at an incredible rate after a decline between 2019 and 2021 that left allocations at record lows.

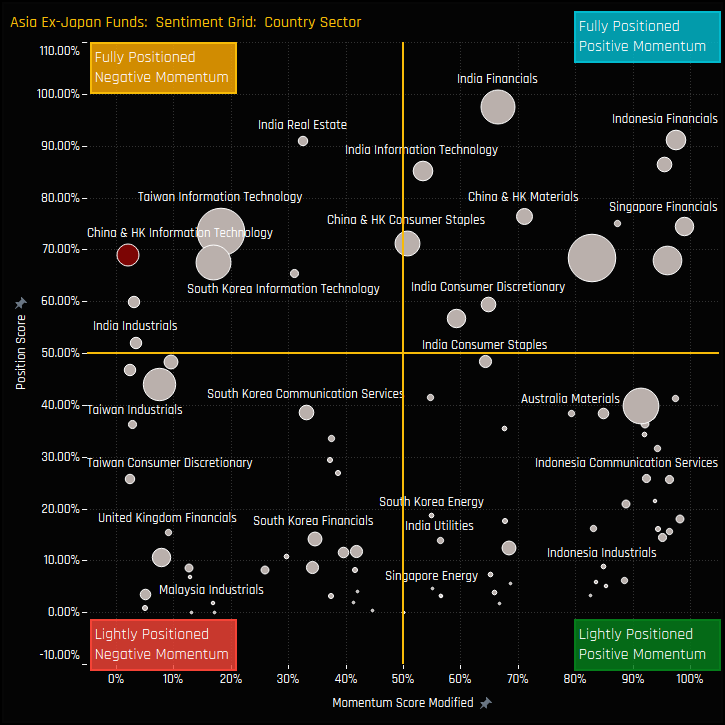

The chart to the right shows where current positioning in each country/sector sits versus history going back to 2011 on a scale of 0-100% (y-axis), against a measure of fund activity for each sector between 01/31/2022 and 07/31/2022 (x-axis). The momentum measure is the most bullish across all country/sectors, yet positioning is some way from the all-time highs.

Versus sector peers, Singapore Financials are way down the pecking order. They are the 14th largest country/sector allocation and the 4th largest country level Financials exposure, behind China & HK, India and Indonesia (see PDF, page 3). Undoubtedly, there is plenty of room for Singapore Financials to play a greater role in Asia Ex-Japan active portfolios.

See below for more ownership information on DBS Group Holdings, United Overseas Bank Ltd and Oversea-Chinese Banking Corp. Please click on the link below for the extended report on Singapore Financials exposure among active Asia Ex-Japan funds.

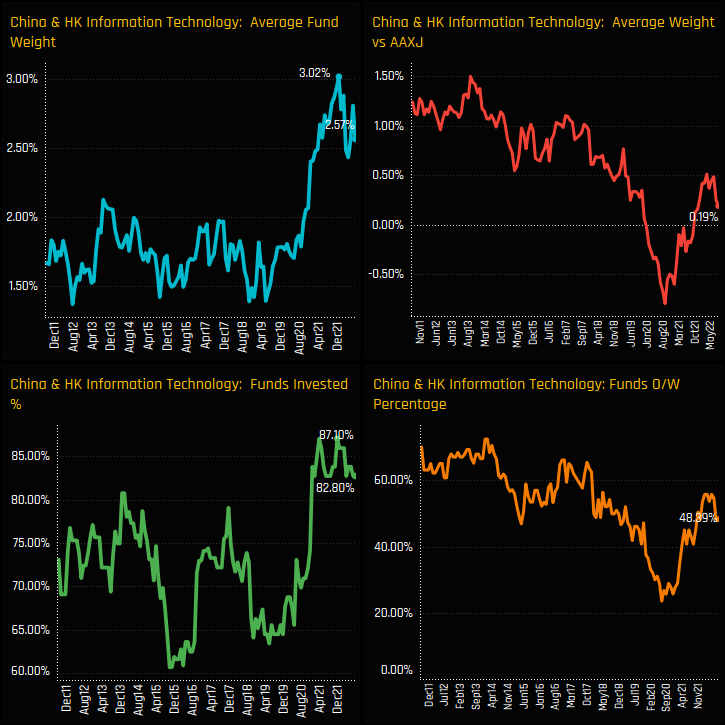

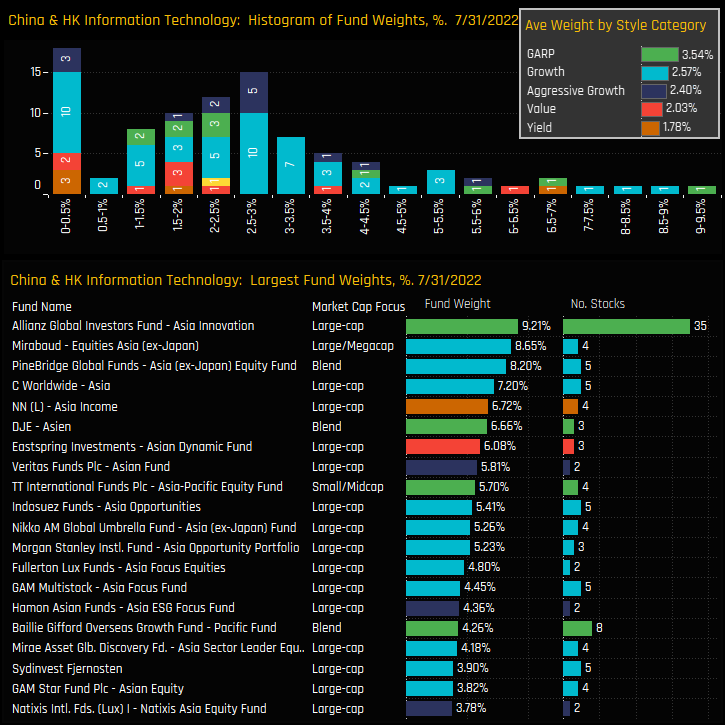

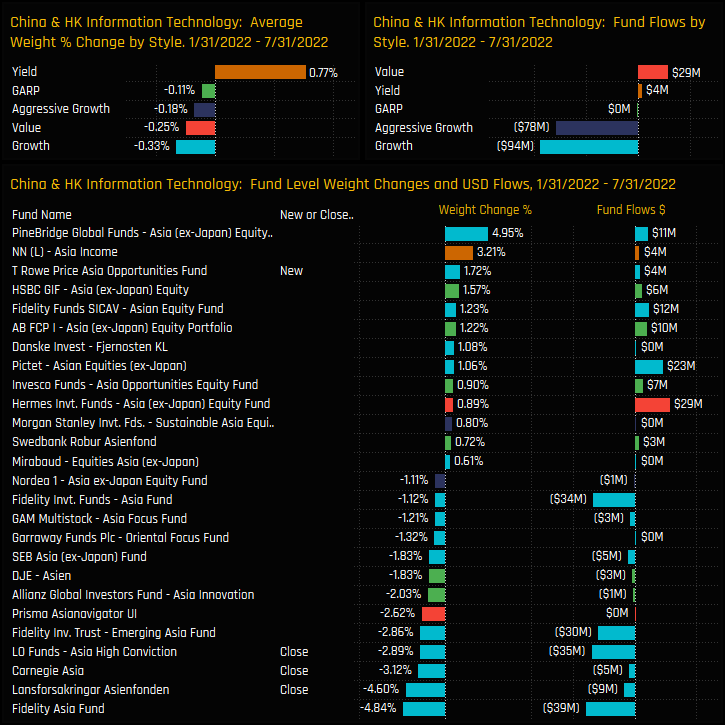

Active Asia Ex-Japan managers appear to be reassessing their exposure towards the China & HK Technology sector. Average weights have fallen from a peak of 3.02% towards the end of last year to 2.57% today, with the percentage of funds invested falling in unison from 87.1% to 82.8%. This isn’t a full-scale reversal, but certainly a sign that the bullish run between 2019 and 2021 has come to an end, for now.

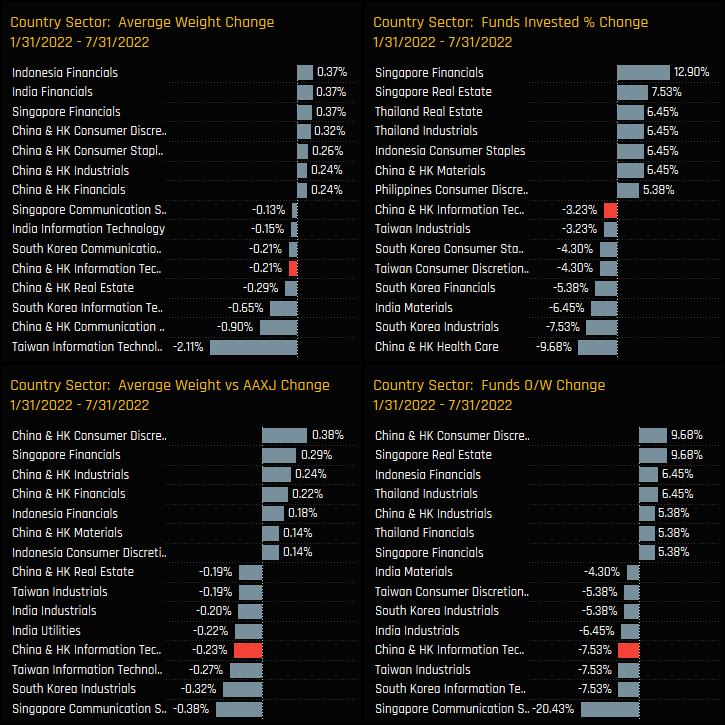

Evidence of this active consolidation can be seen in the charts below, which shows the change in ownership levels for all country/sectors in the Asian universe. Declines in China & HK Tech were captured across the board, with 3.23% of the managers in our analysis closing exposure and 7.5% moving from overweight to underweight.

Fund Holdings & Style

Those funds that do have exposure are clustered around the 1% – 4% level, with a tail to the upside that stretches to 9.21% for the Allianz Asia Innovation Fund. GARP investors are particularly well exposed, with Yield and Value further down the spectrum, on average.

Fund level changes over the last 6-month highlight the imbalance between buyers and sellers in the sector. Closures were led by Landforsakringar Asienfonden (-4.6%), Carnegie Asia (-3.12%) and LO Asia High Conviction (-2.89%), with all Style groups save for Yield seeing allocations decrease.

Stock Holdings & Activity

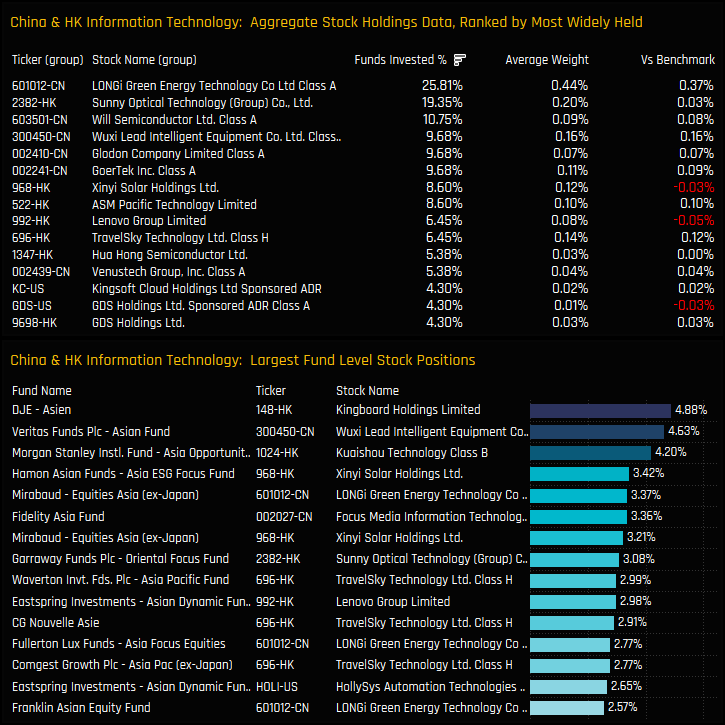

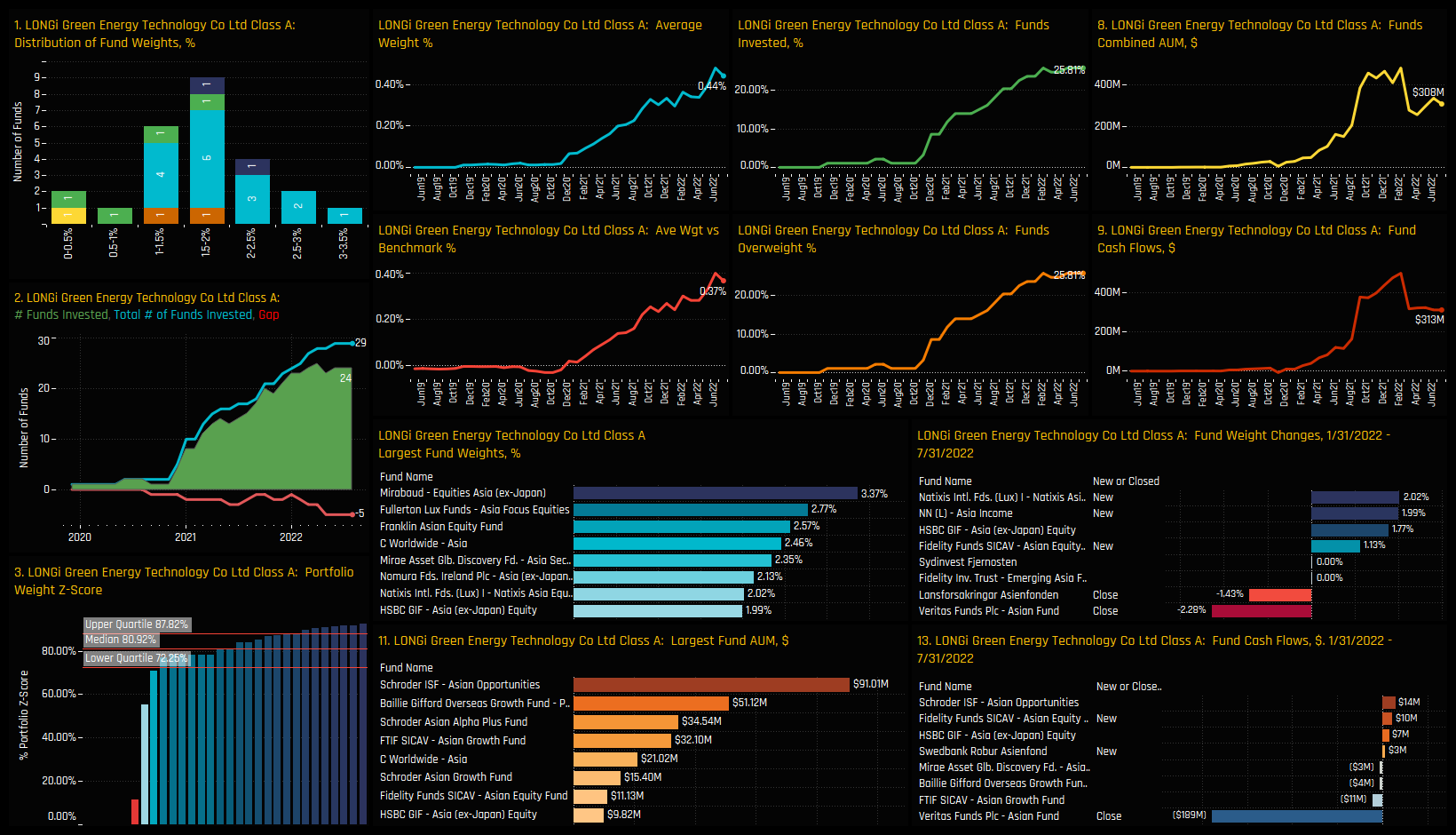

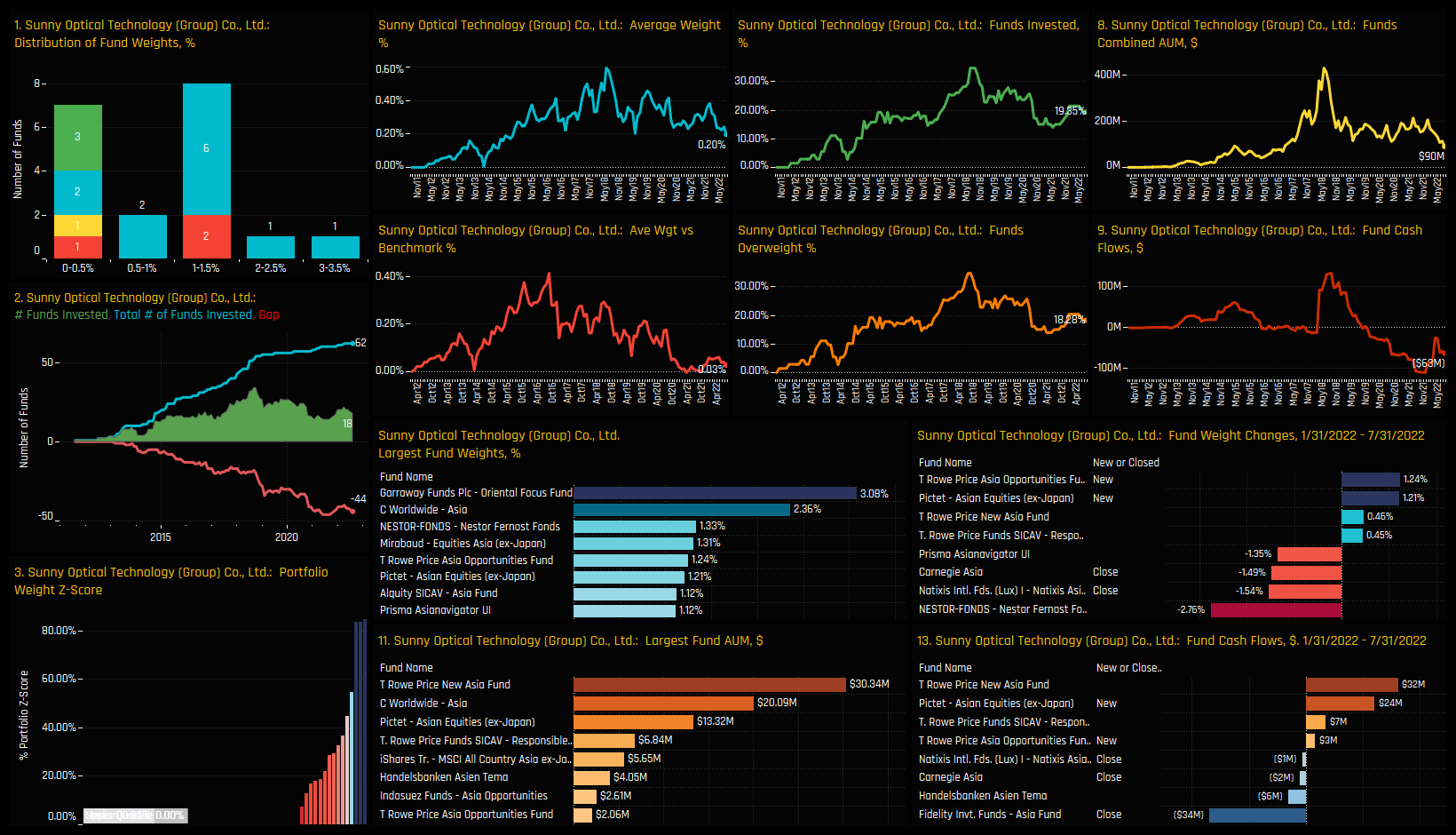

On a stock level, LONGi Green Energy Technology and Sunny Optical Technology are the most widely held stocks in the sector, held by 25.8% and 19.35% of managers respectively. After those 2, allocations are spread across a dozen or so stocks with similar ownership profiles. Interestingly, the higher conviction fund positions are taken up by stocks outside of the top 2, led by DJE Asien in Kingboard Holdings Limited (4.88%) and Veritas Asian Fund in Wuxi Lead Intelligent Equipment (4.63%).

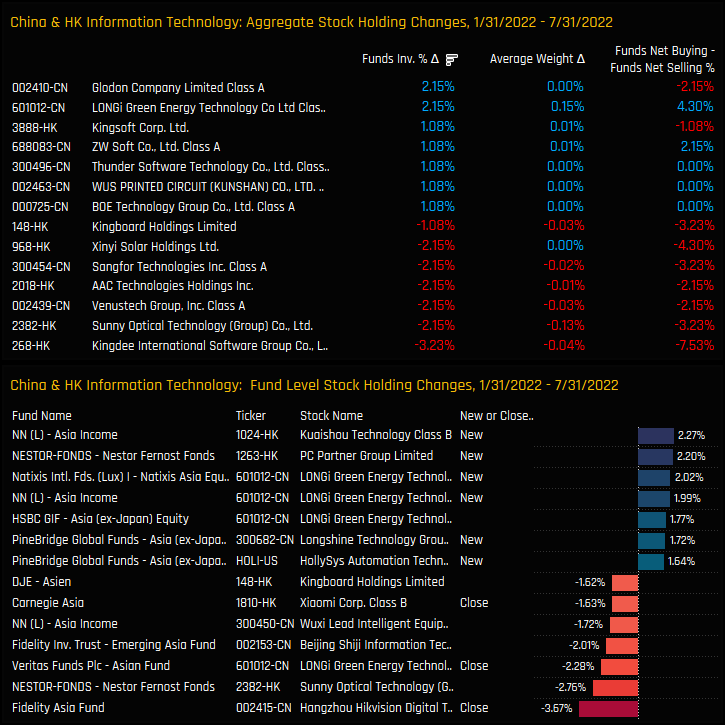

Stock activity between 01/31/2021 and 07/31/2022 wasn’t entirely one directional, though again skewed to the sell side. Key holding LONGi Green Energy Technology captured an increase in funds invested of +2.15%, whilst Sunny Optical Technology saw the opposite. Kingdee International Software Group saw ownership fall the most, losing investment from -3.23% of the funds in our analysis over the period.

Conclusions

China & HK Technology allocations are in a state of consolidation. Whilst not a total reversal or exodus, we can say with certainty that the bull run between 2019 and 2021 has taken a breather, and ownership levels are stalling for many names in the sector.

The same Sentiment Grid as in the previous insight highlights the differing fortunes of the China & HK Technology sector versus Singapore Financials. Both are at similar levels on the positioning scale (higher end of the range/off the highs), but China Technology is on the far left, indicative of managers scaling back exposure versus other sectors in the Asian universe.

The fact that Taiwan Technology and South Korea Technology are at similar placements on the Grid suggests that this is part of a broader sector move, yet China & HK Technology appears to be bearing the brunt.

See below for more ownership information on LONGi Green Energy Technology and Sunny Optical Technology. Please click on the link below for the extended report on China Technology exposure among active Asia Ex-Japan funds.

Stock Profile: LONGi Green Energy Technology

Stock Profile: Sunny Optical Technology Co

Click on the link below for the latest data report on China Technology positioning among active Global funds.

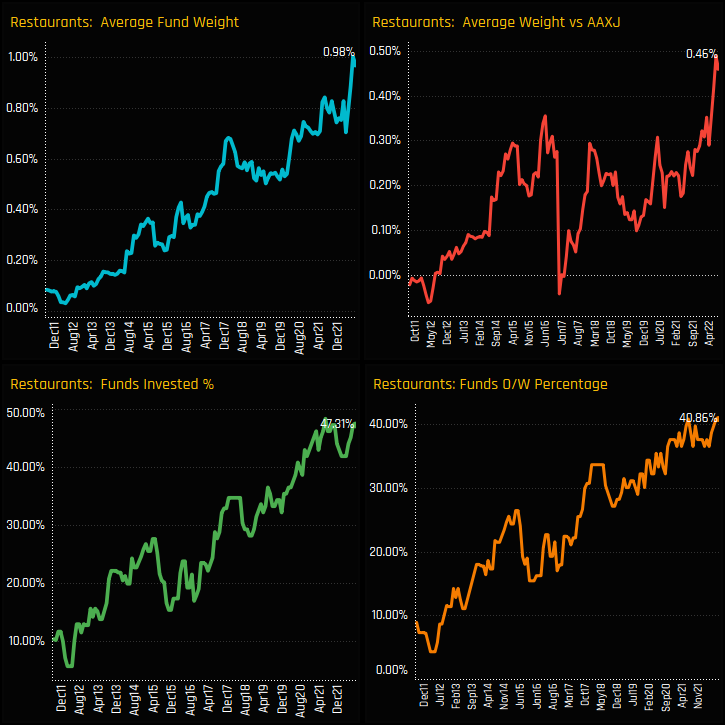

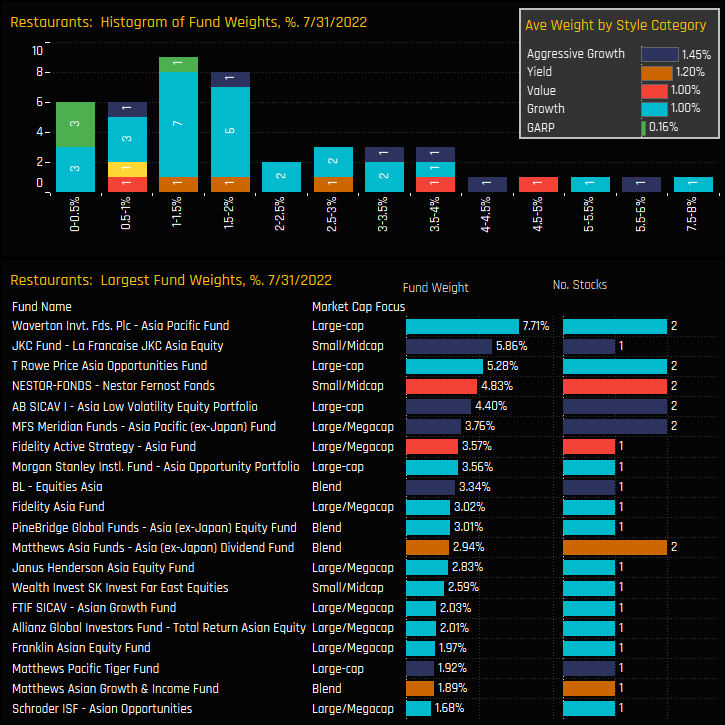

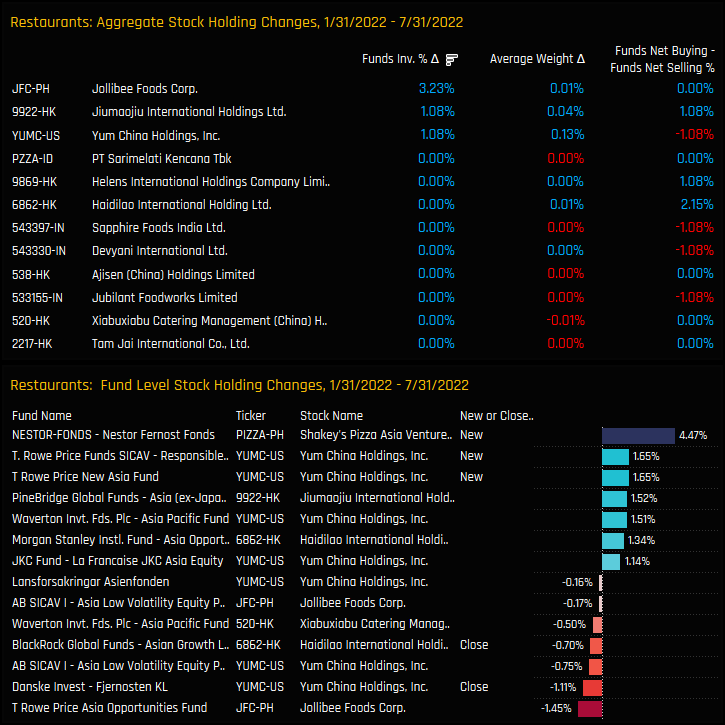

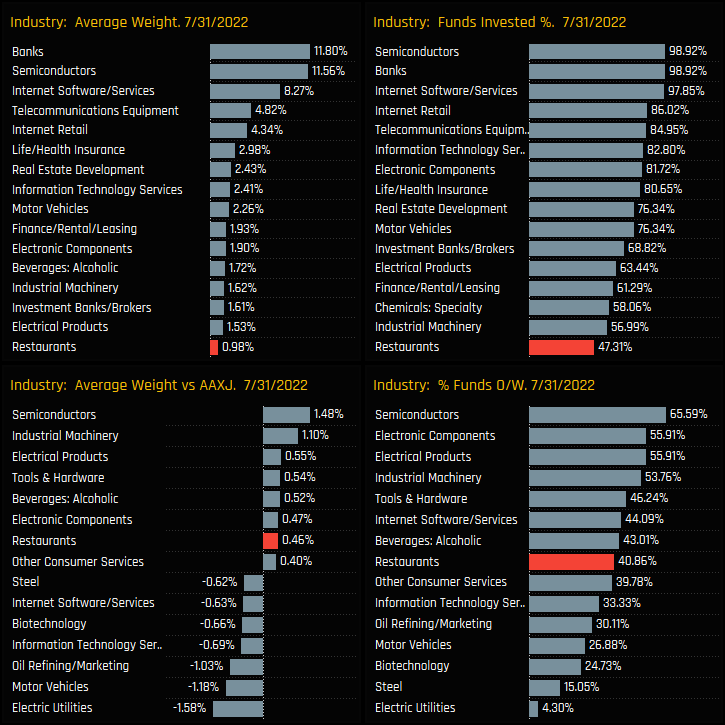

Active fund exposure in the Restaurant industry group has taken a sharp move higher. Average weights stand at 0.98%, a whisker off the all-time high of 1% achieved last month, with the percentage of funds invested moving higher and overweights extending towards all-time highs.

Versus Industry peers, activity among the Asia Ex-Japan managers in our analysis has been favourable towards the Restaurant sector, with all measures of ownership moving higher over the last 6-months. Restaurant stocks captured the 4th largest increase in funds invested and the 6th largest in terms of average weight.

Fund Holdings and Activity

Among holders, the typical fund weight sits below 2%, though the range extends to 7.7% for the Waverton Asia Pacific Fund. All Style groups are well represented among the larger allocations with the exception of GARP managers. A mixture of Aggressive Growth, Growth, Value, Large-cap and Small-cap strategies occupy the top 20 holders.

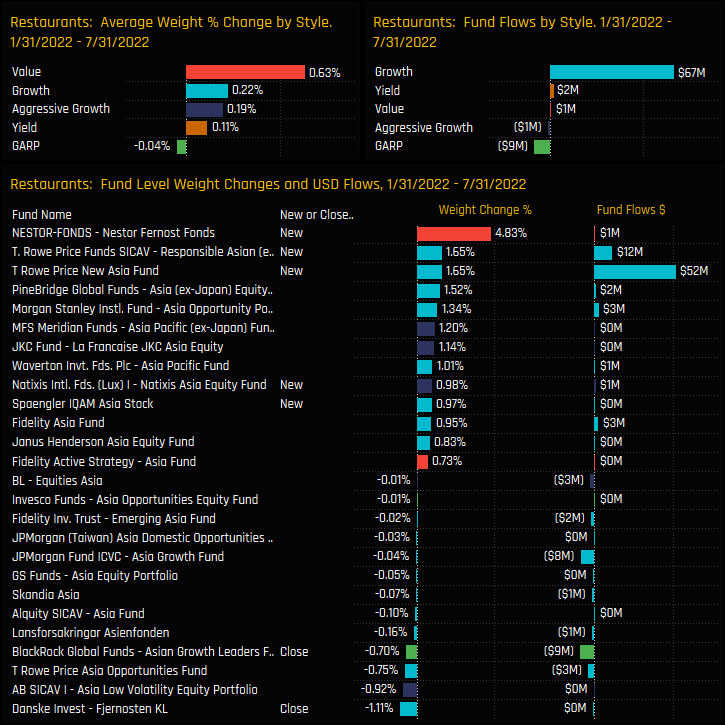

Fund level changes between 01/31/2022 and 07/31/2022 are led by new positions from Nestor Fernost (+4.83%), T Rowe Price Responsible Asia (-1.65%) and T Rowe Price New Asia (+1.65%). All Style groups except GARP saw allocations increase over the period, on average.

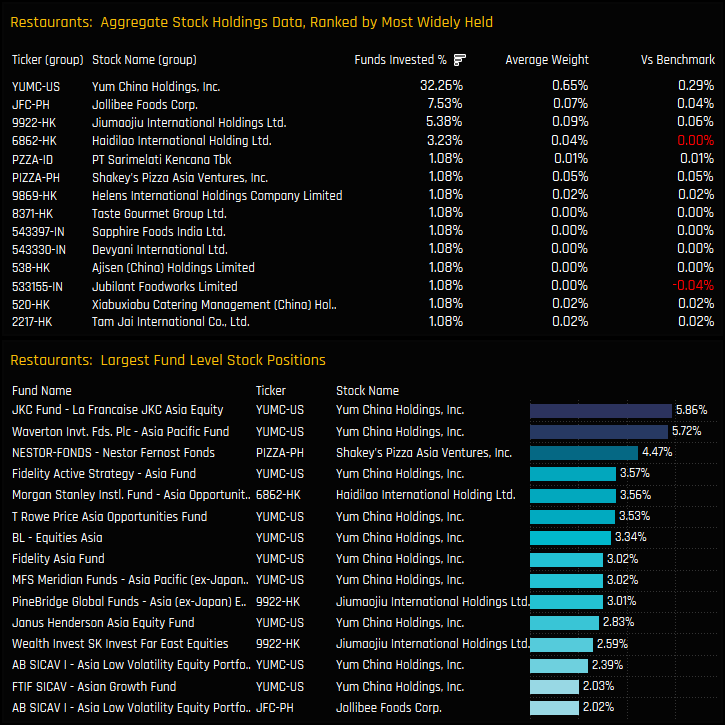

Stock Holdings and Activity

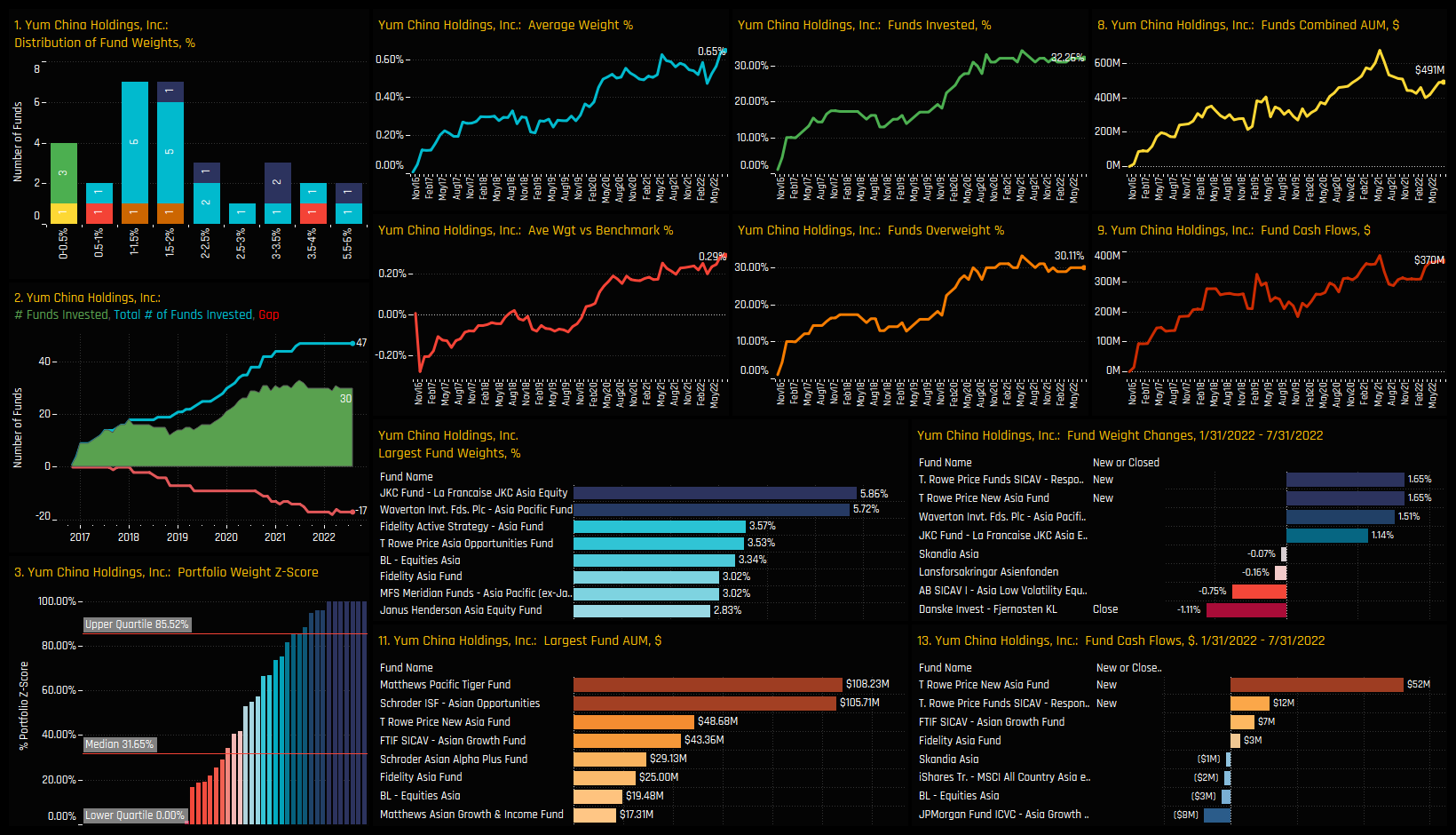

Yum China Holdings dominates the picture on a stock level, held by 32.26% of managers and accounting for a third of total allocations in the industry group. After that, only Jollibee Foods Corp, Jiumaojiu International Holdings and Haidilao International Holdings are held by more than a single fund in our analysis. Nestor Fernost’s 4.47% holding in Shakey’s Pizza Asia Ventures stands out among a sea of high conviction positions in Yum China Holdings, led by JKC Asia Equity (5.86%) and Waverton Asia Pacific (5.72%).

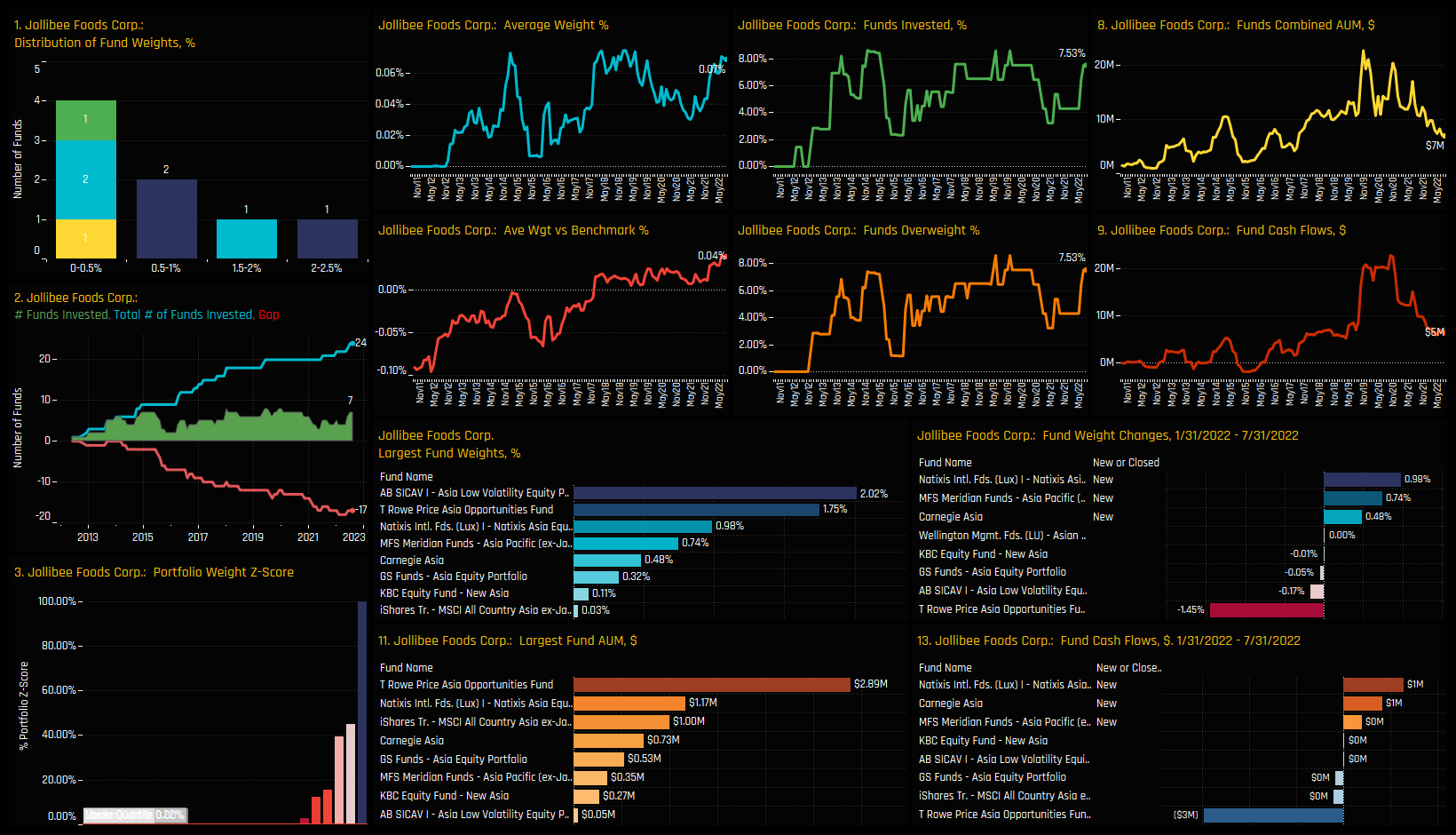

Aggregate fund activity over the last 6-months was mostly positive and led by Jollibee Foods Corp, having captured investment from a further +3.23% of Asian investors. Average weights in Yum China Holdings increased by +0.13%, with the T Rowe Price Responsible Asia and New Asia funds opening positions against Danske Ferjenosten closing.

Conclusions

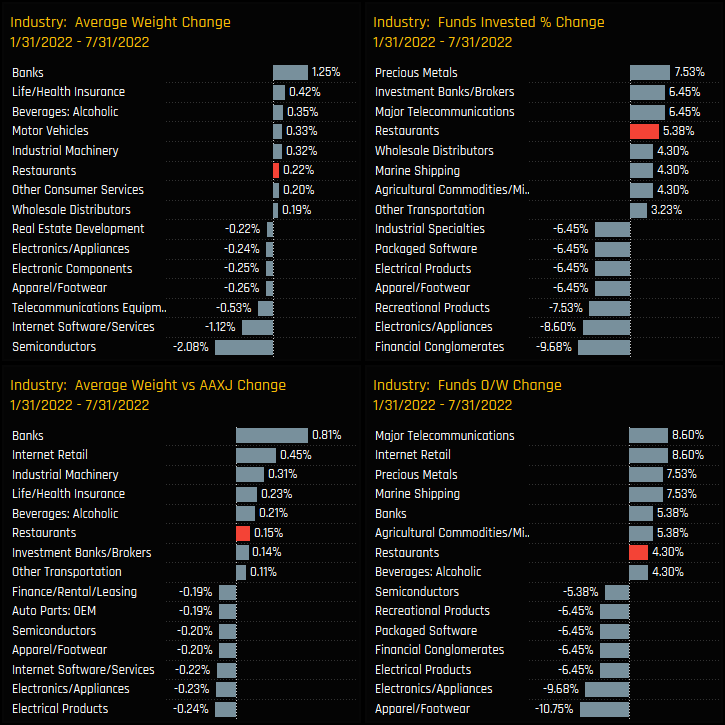

The top 2 charts to the right show Restaurant stocks a long way down the pecking order of industry allocations on an absolute basis, with Financials, Tech and selected Consumer related industries dominating the picture. On a relative basis however, the bottom charts show Restaurants as the 7th largest Industry overweight, a mark of the growing confidence that active investors have placed in the sector.

On a stock level, it feels rather like a bet on a single company rather than an Industry wide trend, with a clear over-reliance on Yum China Holdings as a representation for the whole sector. However, as selected funds buy in to some of the 2nd tier names, led by Jollibee Foods Corp, it suggests that the opportunity set within the sector is widening, and with that an increased potential for exposure to grow further.

Stock Profile: Yum China Holdings, Inc

Stock Profile: Jollibee Foods Corp

Click on the link below for the latest data report on Asian Restaurant positioning among active Global funds.

For more analysis, data or information on active investor positioning in your market, please get in touch with me on steven.holden@copleyfundresearch.com

{kind=link}