24 November

Emerging Markets

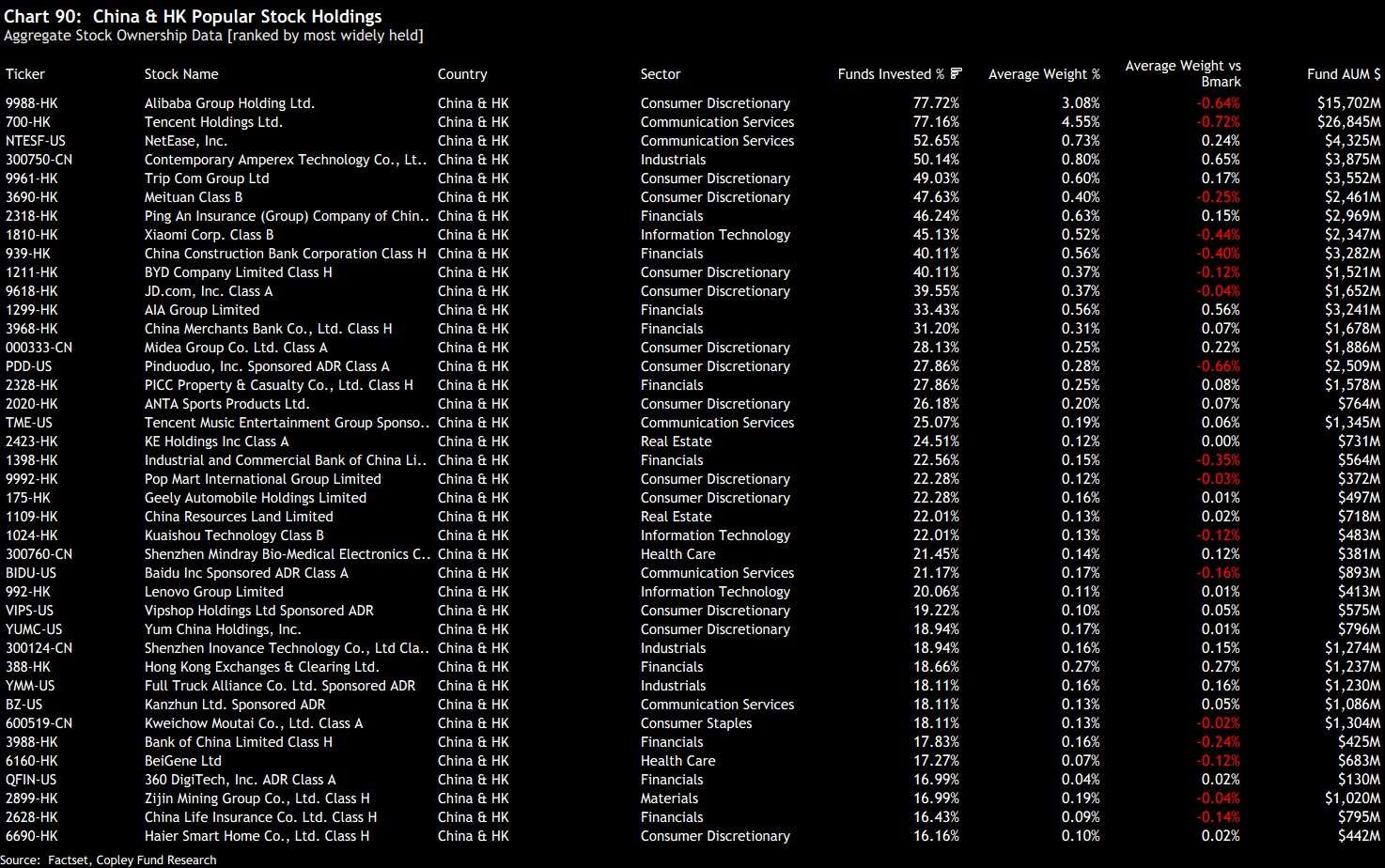

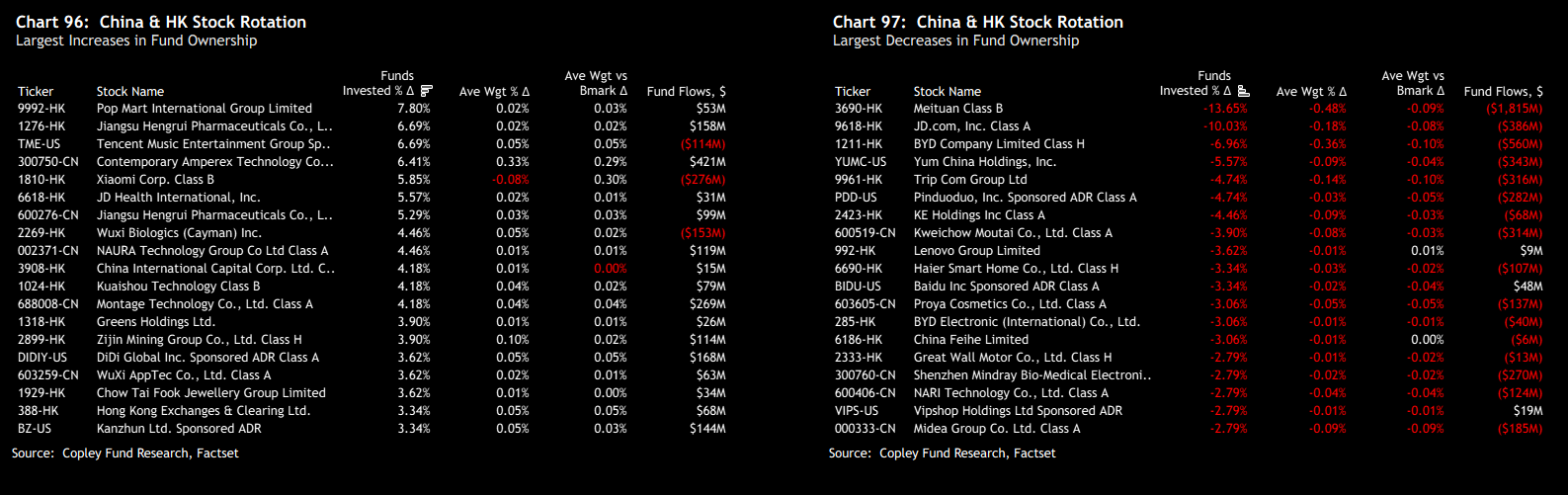

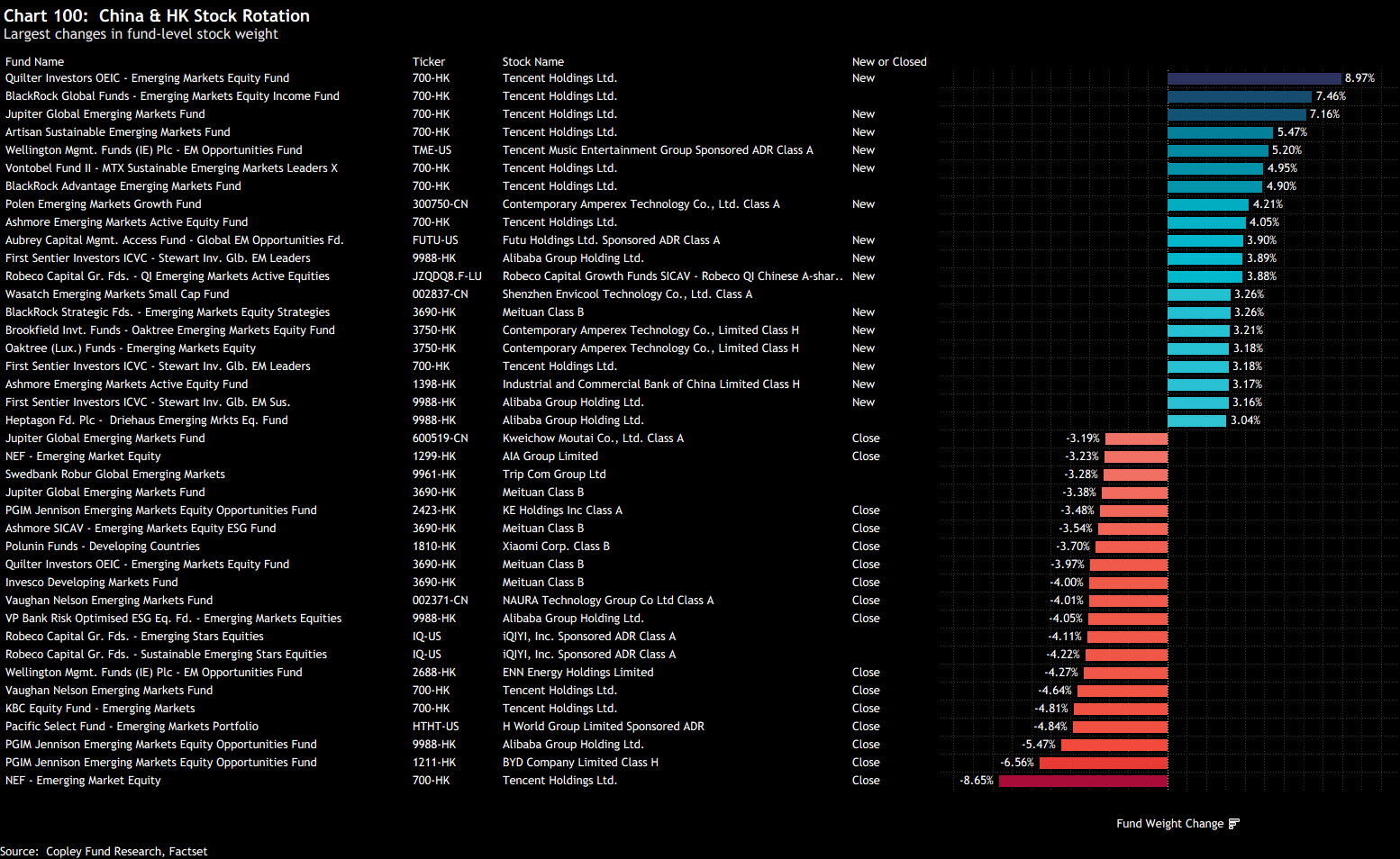

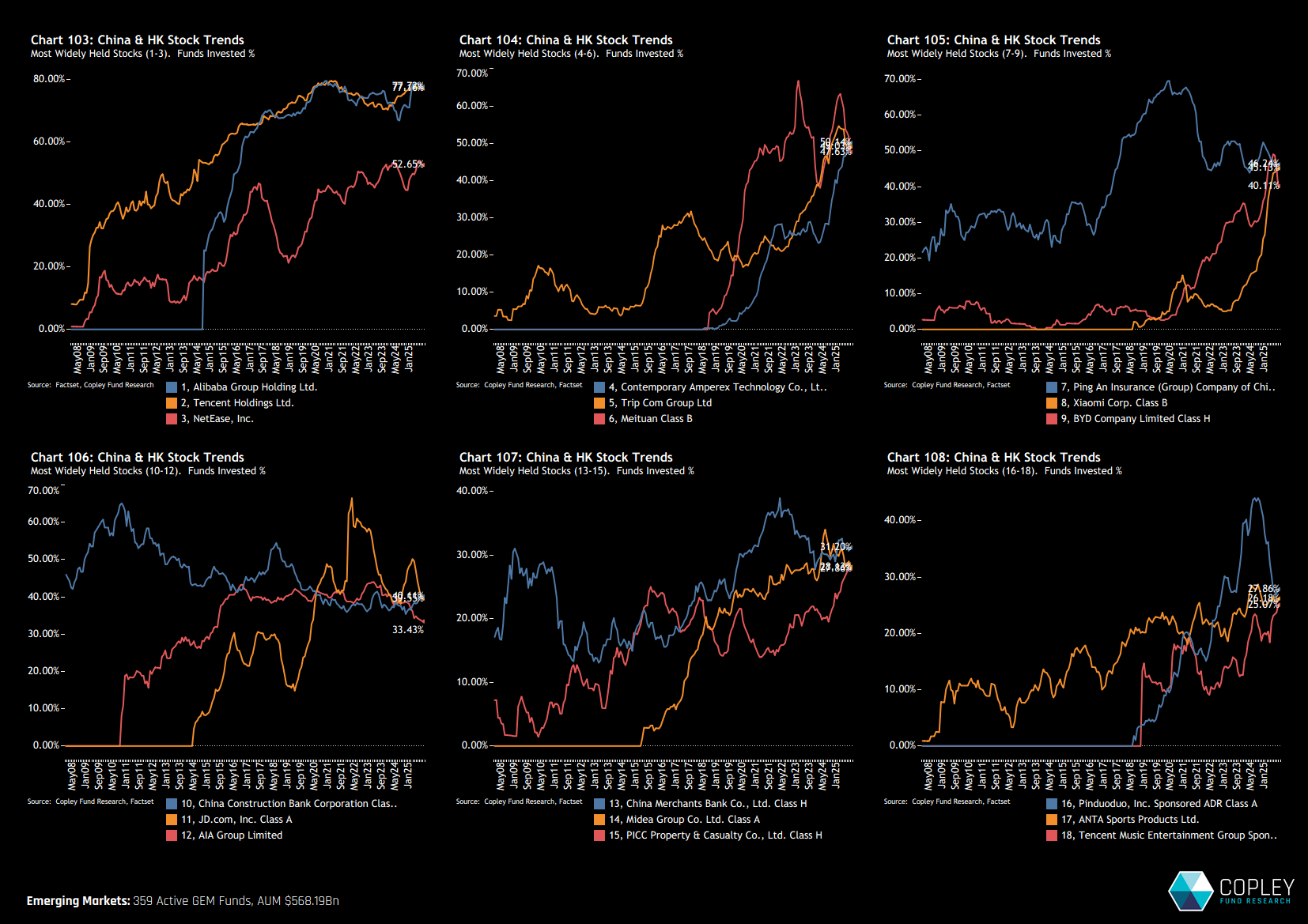

China & HK: Rebuild Slows Amid Heavy Sector and Stock Rotation

- Steve Holden

- 0 Comments

Related Posts

{kind=link}