In this piece we provide a comprehensive analysis of Utilities sector positioning among active UK Equity funds. We find that Utilities exposure among active UK equity funds has been on an upward trend since bottoming out in 2019. Underweights have been closed as managers increase exposure to key stocks in the sector, led by Drax Group, SSE plc and United Utilities. Whilst Yield and GARP managers have led the charge higher, Growth and Aggressive Funds remain underinvested compared to their own history.

Time-Series Ownership Analysis

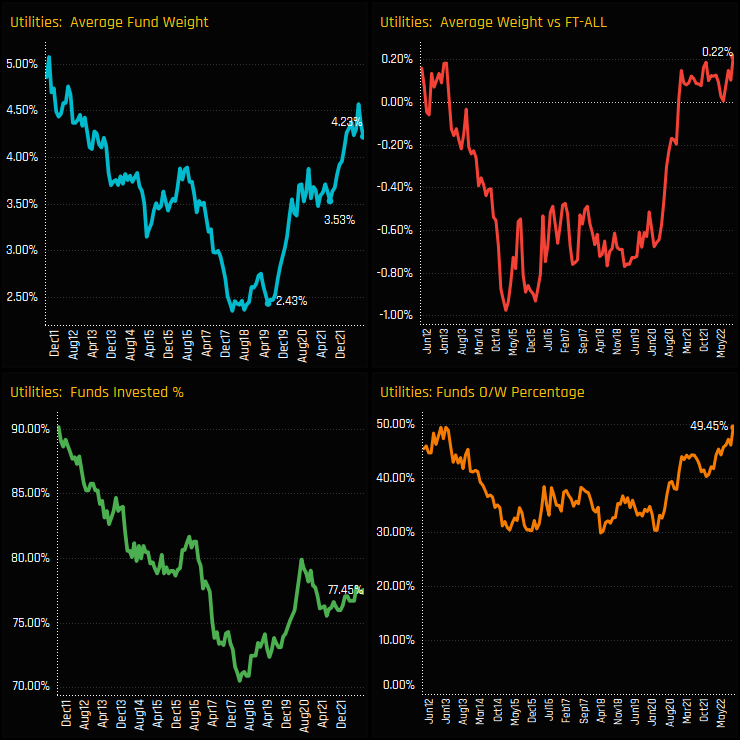

Utilities allocations among active UK equity funds are on an upward trend. From a low of 2.43% in mid-2019, average fund weights have climbed to 4.23% as of the end of last month, with 77.45% of funds invested at the higher end of the 5-year range. Relative to the benchmark FTSE All-Share index, active UK managers are at peak overweights of +0.22%, with a record 49.45% of funds positioned higher than the benchmark index.

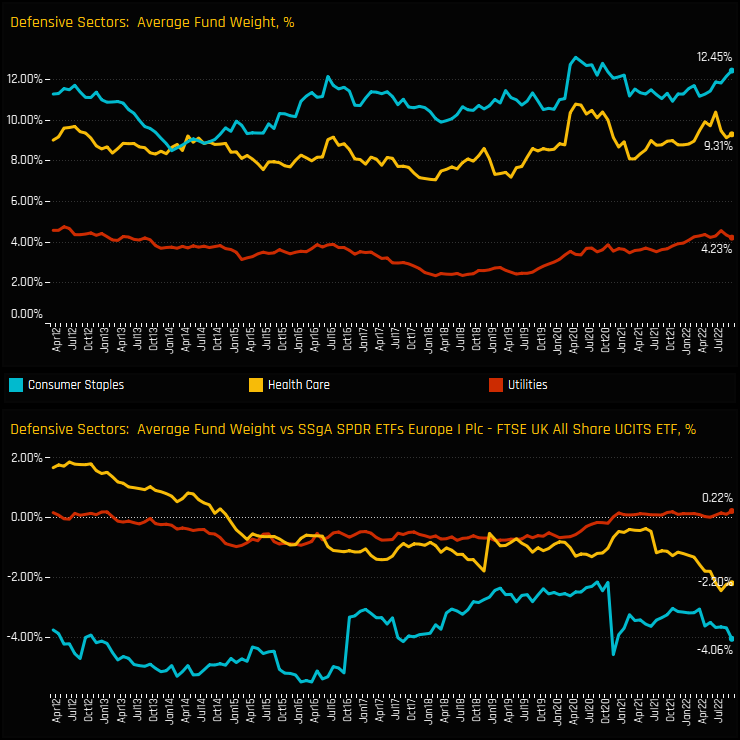

These increases in exposure have brought Utilities closer to their Defensive peers on an absolute basis (top chart), though Health Care and Consumer Staples still occupy a much larger percentage in UK equity funds. Relative to the FTSE All-Share index, active managers switched from underweight Utilities to overweight in 2020, but continue to run significant underweights in the Consumer Staples and Health Care sectors (bottom chart).

Sector Analysis

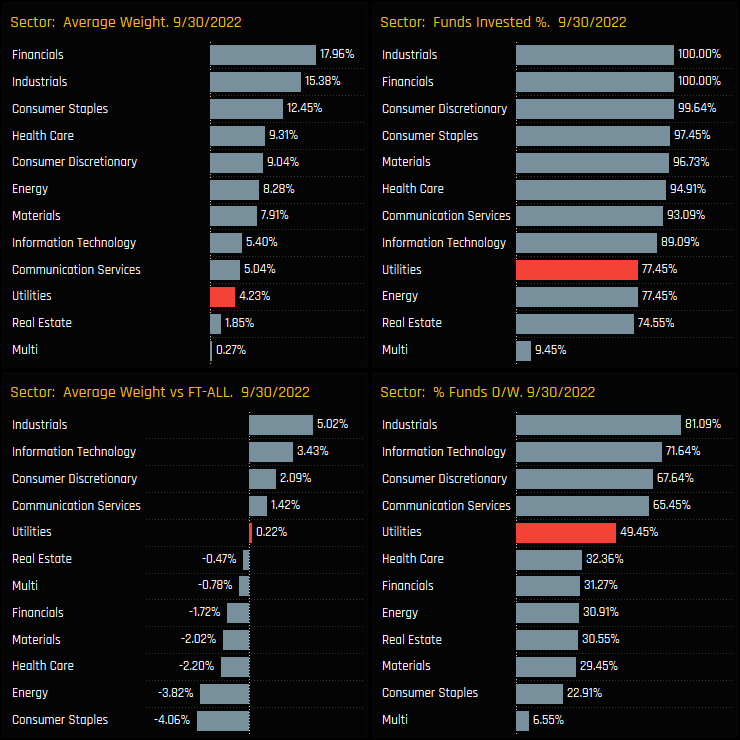

Utilities remain well down the pecking order of sector allocations for the average UK equity fund, being the 2nd smallest sector on an average weight basis as Financials and Industrials occupy the top 2 spots (top left chart). Relative to benchmark, Utilities positioning is largely in line, with UK managers instead running large overweights in Industrials (+5.02%), Information Technology (+3.43%) and Consumer Discretionary (+2.09%), against underweights in Consumer Staples (-4.06%), Energy (-3.82%) and Health Care (-2.20%).

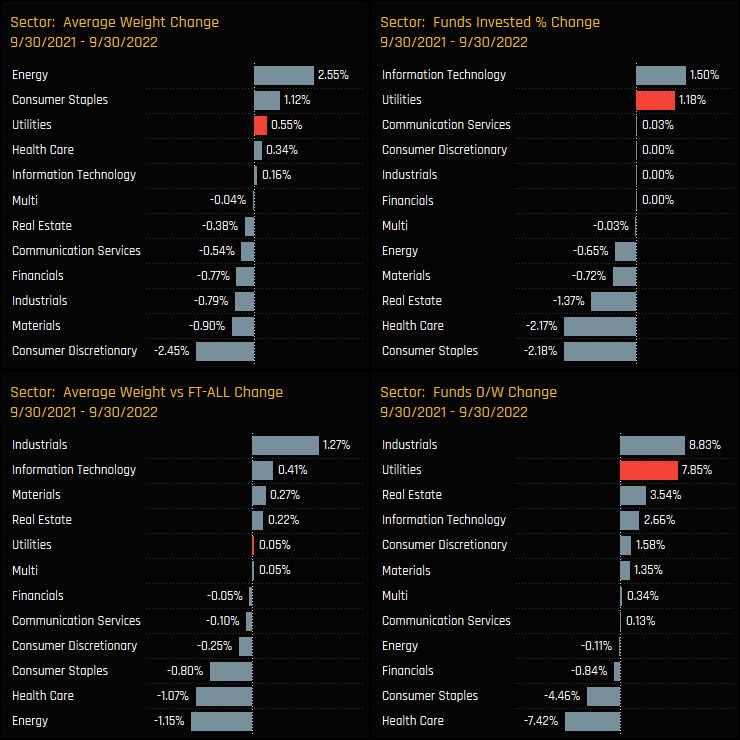

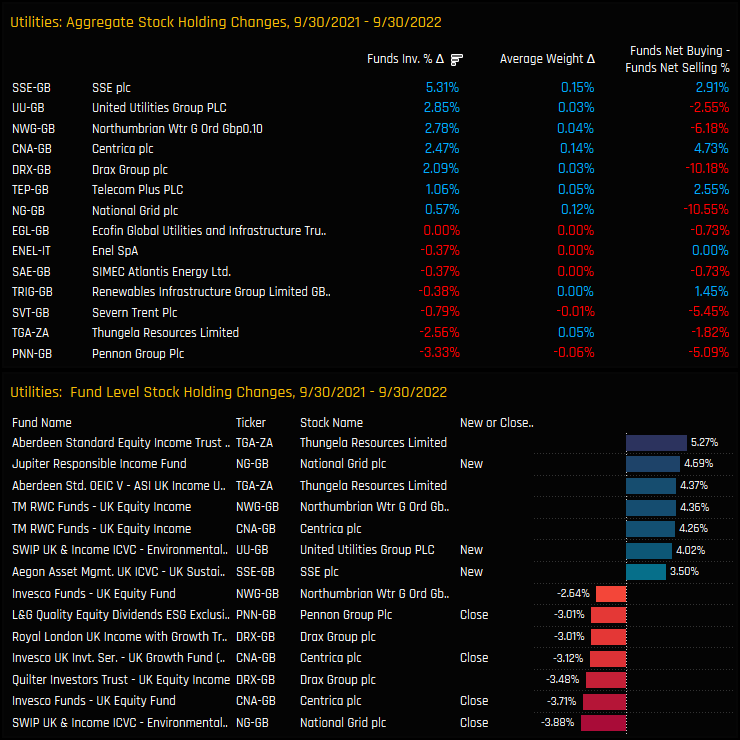

Ownership changes across UK sectors over the last 12-months highlight the change in sentiment towards the Utilities sector. Between 09/30/2021 and 09/30/2022, average weights have increased by +0.55%, the percentage of funds with exposure by +1.18% and 7.85% of the UK funds in our analysis moved to overweight. These moves were among the highest across all sectors in the UK over the period.

Fund Holdings & Style Analysis

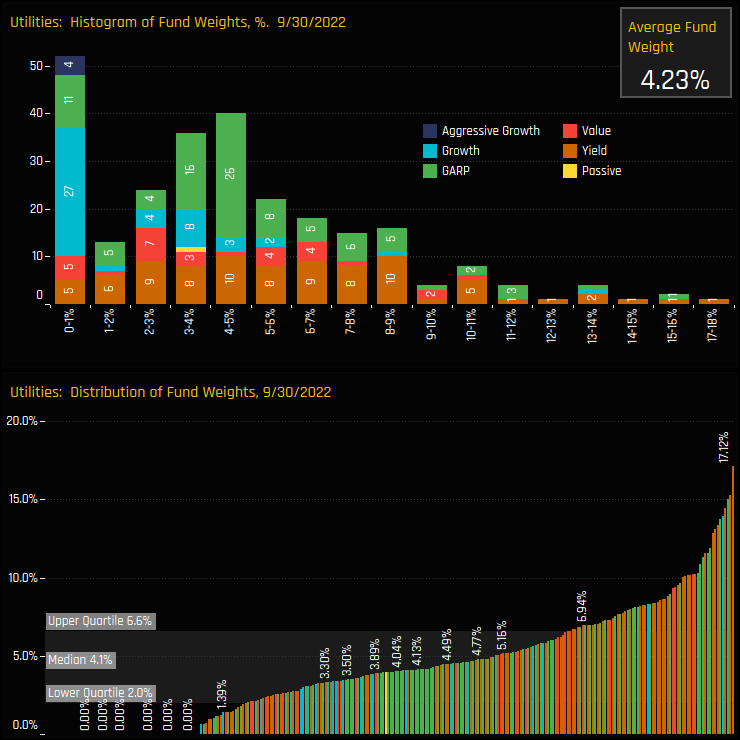

On a fund level, the majority of UK managers hold less than a 10% allocation in the Utilities sector, with 50% of managers sandwiched between the lower and upper quartiles of 2.0% and 6.6%. At the lower end are the 22.5% of funds who hold no exposure at all and the top end 4 funds who hold above 14%, topping out at 17.12%.

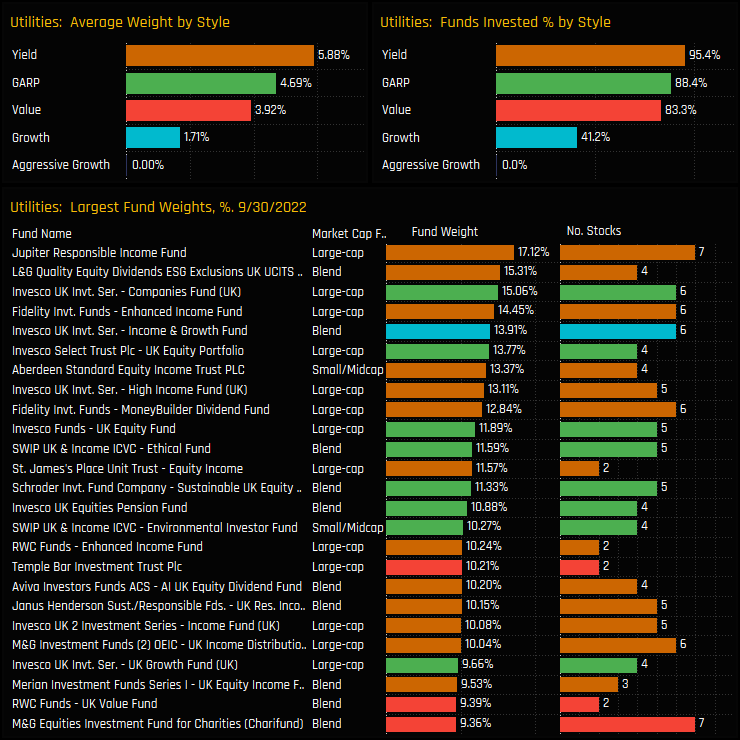

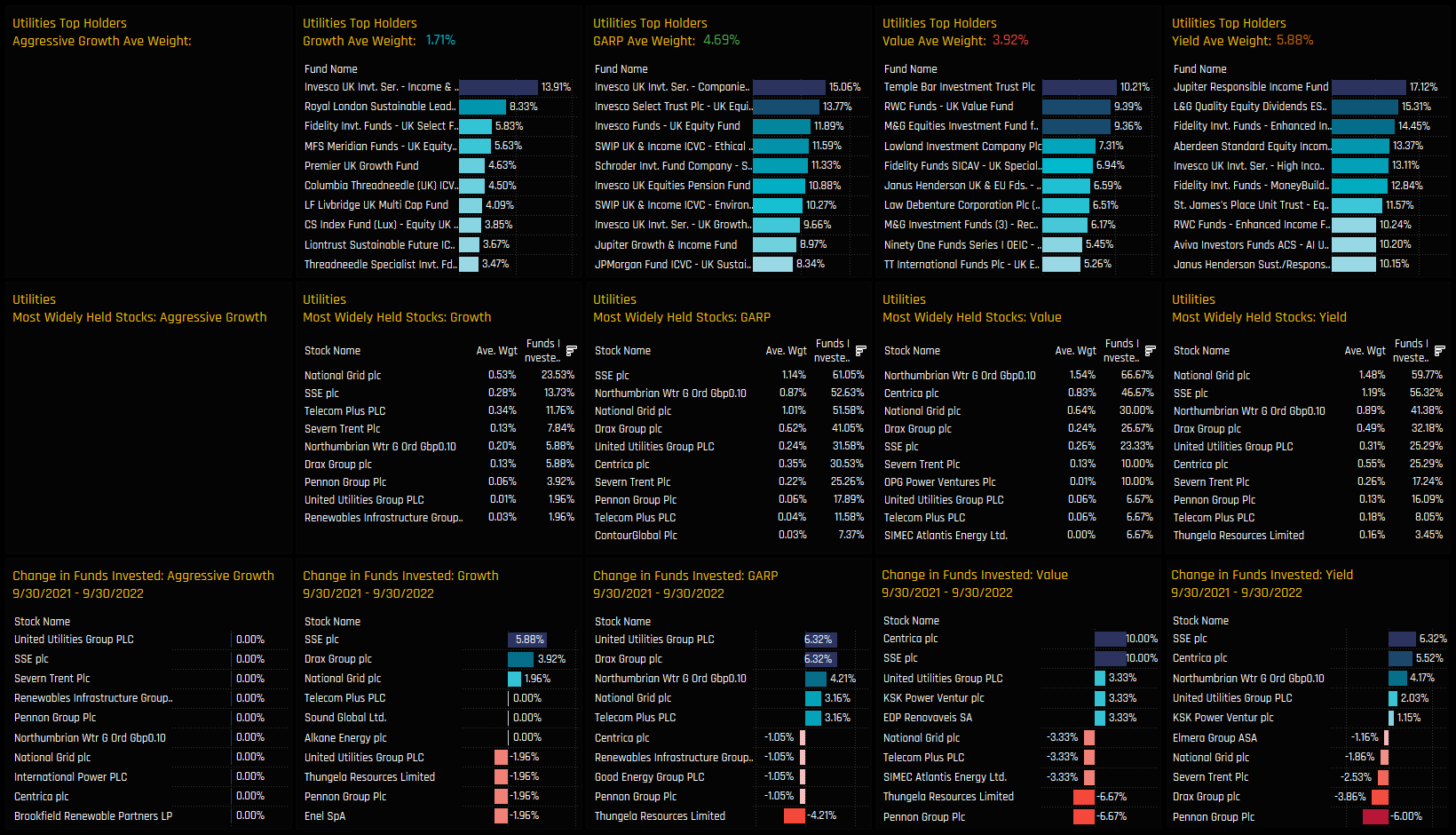

The largest holders are a mixture of Yield and GARP funds, led by Jupiter Responsible Income (17.12%) and L&G Quality Equity Dividends (15.31%). On average, Yield funds are the dominant Style group, with average weights of 5.88% and 95.4% of funds invested. This is in stark contrast to Growth managers, with just 41.2% of managers invested at an average weight of 1.71%. Not a single Aggressive Growth fund in our analysis has exposure to the Utilities sector!

Fund Activity & Style Trends

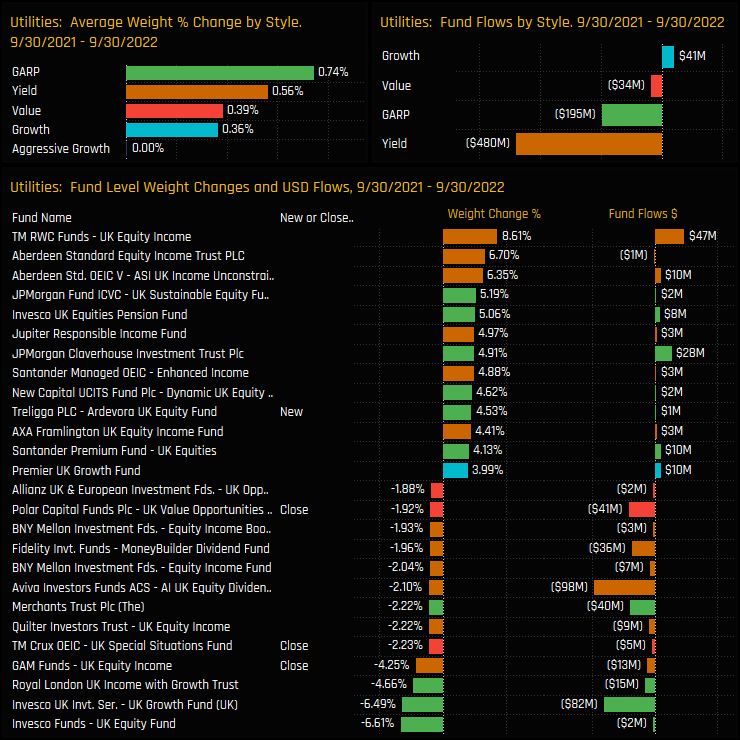

Fund activity between 09/30/2021 and 09/30/2022 is skewed to the buy side, with all Style groups seeing average Utilities allocations increase, save for Aggressive Growth. GARP and Yield funds were again the standouts, with new positions from Ardevora UK Equity (+4.53%) and large increases from RWC UK Equity Income (+8.61%) and Aberdeen Equity Income Trust (+6.7%). The net fund outflows from Yield and Value funds were on the back of -$10bn in net outflows for the UK equity fund group as a whole over the period.

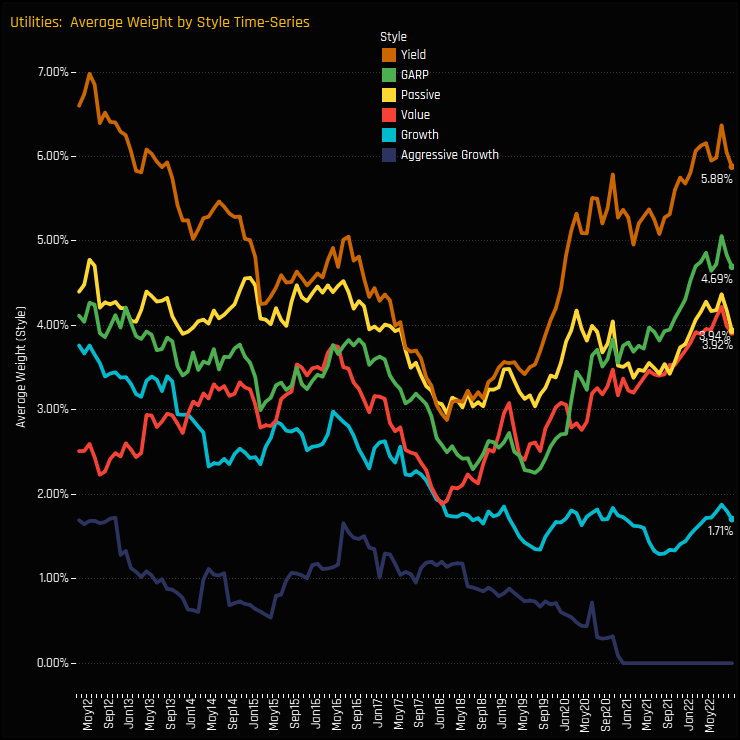

Analyzing Style allocations in the Utilities sector over the last decade shows a growing dispersion between Yield, Value and GARP funds who have increased weights relative to benchmark, versus Growth and Aggressive Growth funds who have let underweights increase to near record levels.

Stock Holdings & Activity Analysis

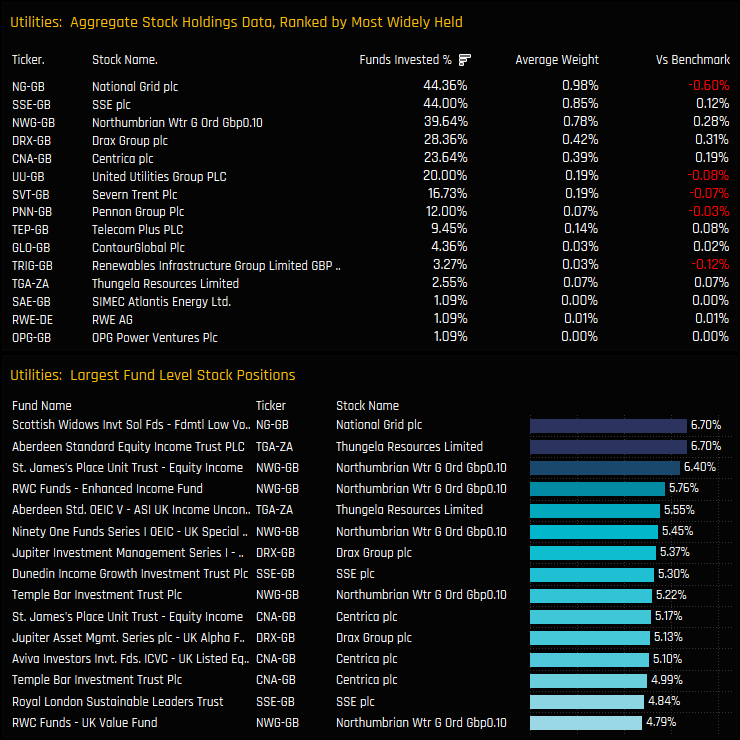

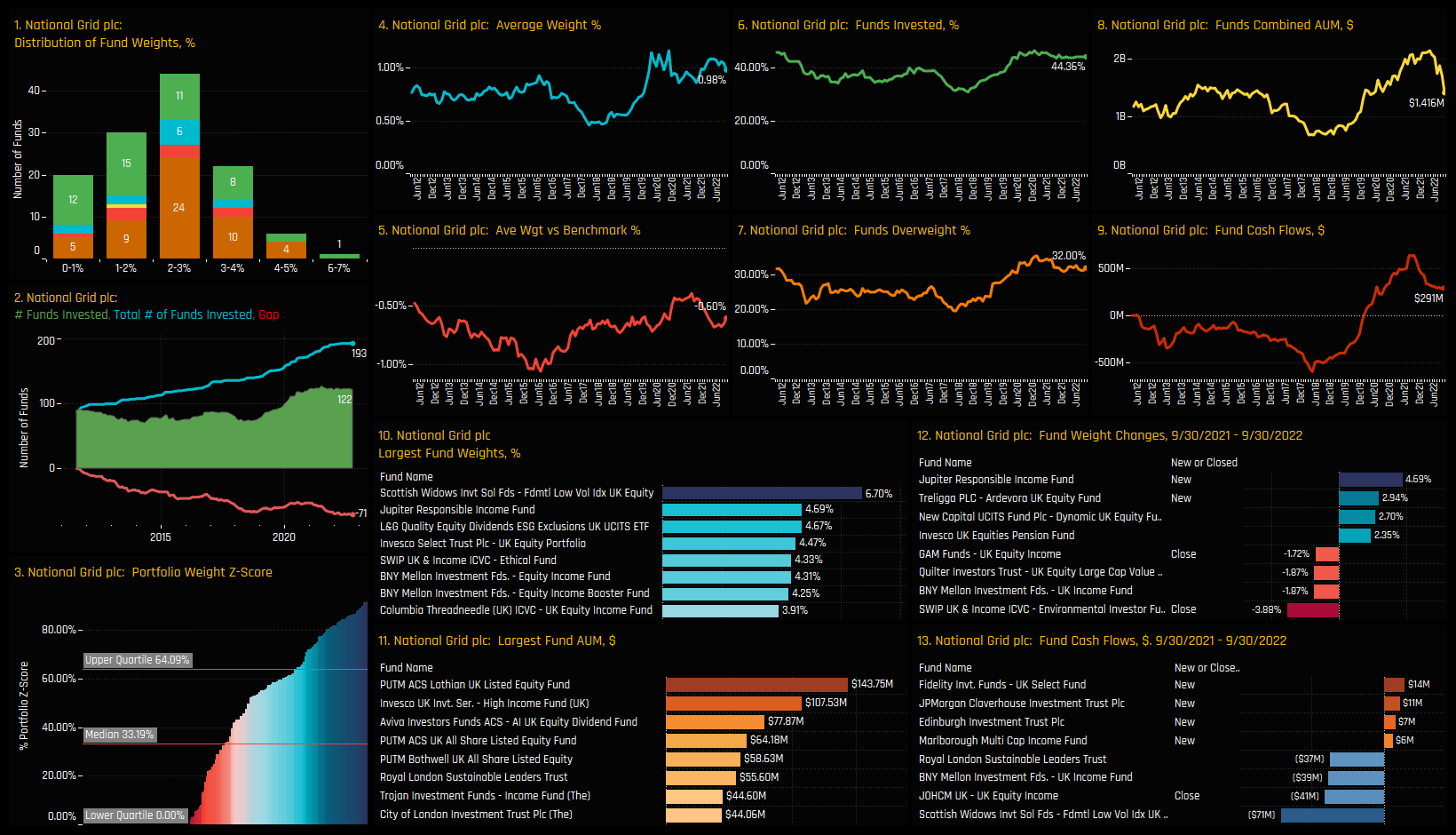

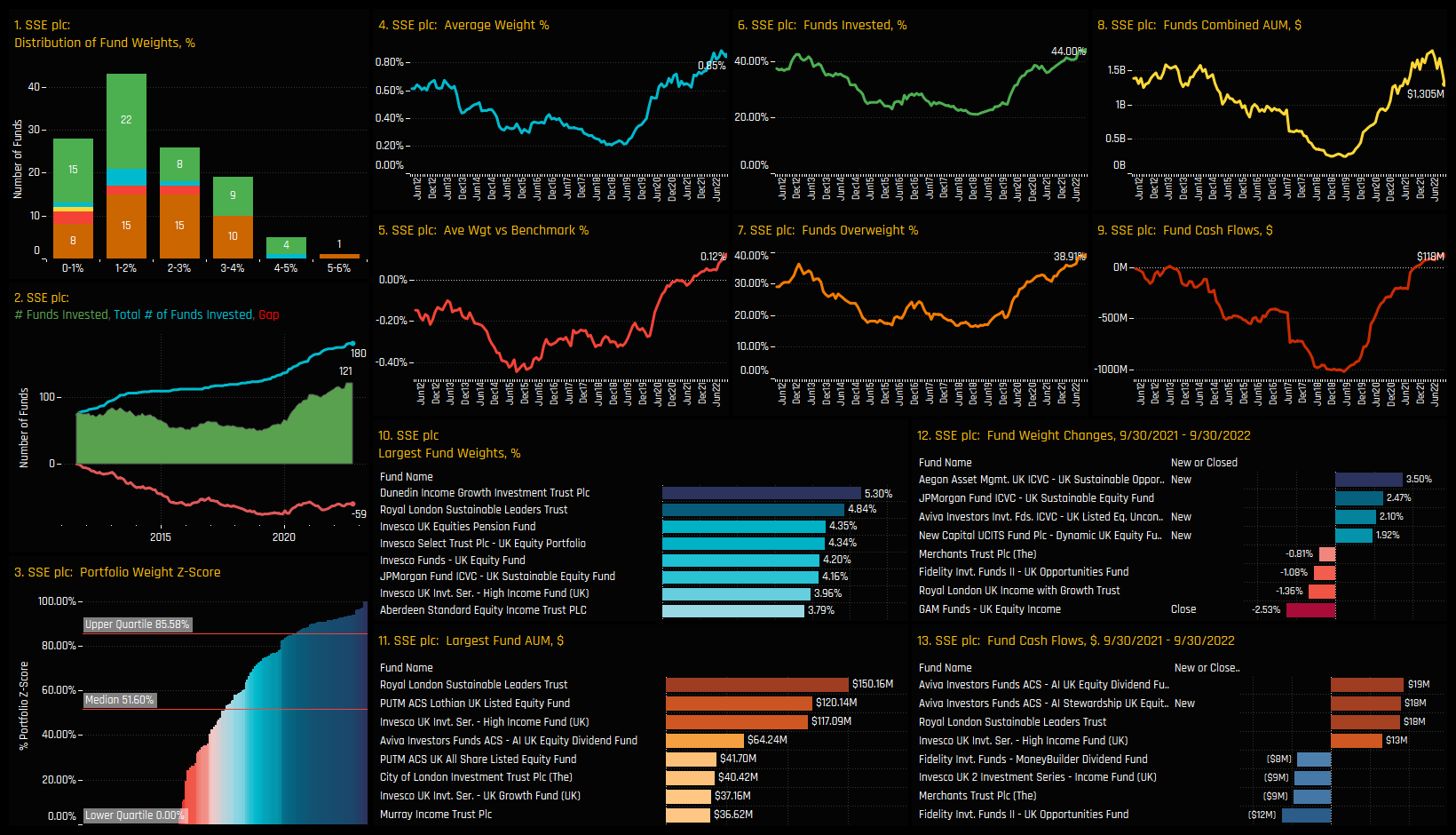

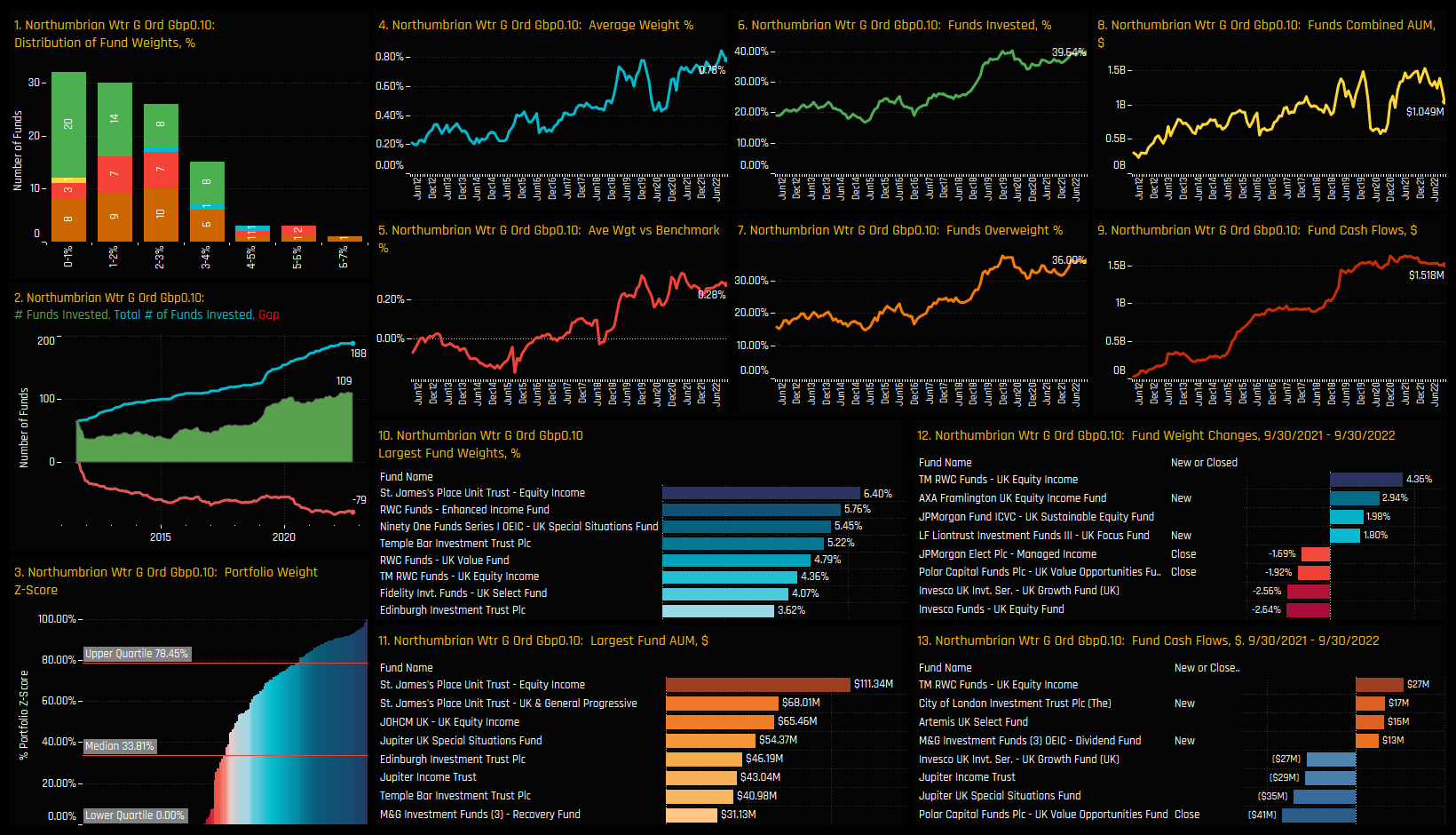

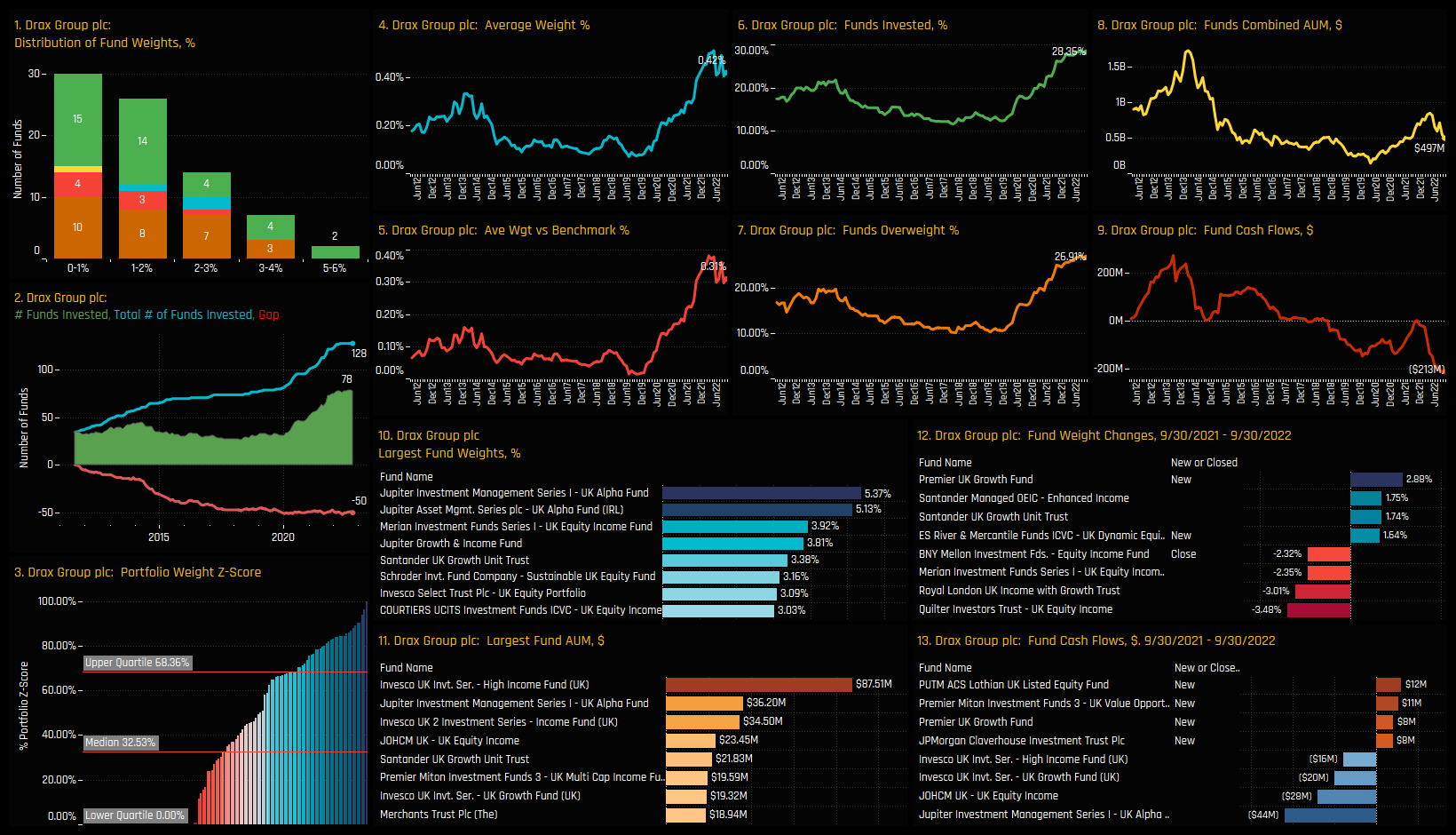

The most widely held stocks in the Utilities sector are National Grid plc, SSE plc and Northumbrian Water, held by 44.4%, 44.0% and 39.6% of UK equity funds respectively. A further 5 stocks are held by more than 10% of managers, led by Drax Group plc and Centrica plc. High conviction positions are mainly spread across the 4 most widely held stocks, with Northumbrian Water the standout among the top 20 (bottom chart).

Activity over the last 12-months has favoured SSE plc, with a further +5.31% of funds buying in to the stock as well as United Utilities Group plc with +2.85%. Northumbrian Water, Centrica plc and Drax Group have also seen ownership levels rise, whilst Pennon Group plc and Thungela Resourced Limited provided balance on the sell side. Overall though, it’s a positive picture.

Stock Holdings by Style

Split by Style, SSE plc and National Grid plc are top holdings across every Style group (except Aggressive Growth). Northumbrian Water holds particular appeal to Value managers, whilst Drax Group plc has captured strong increases in ownership growth across Growth and GARP managers over the past 12 months.

Conclusions

Our data shows an increasing level of exposure towards the Utilities sector among active UK investors. From bottoming out in late 2019, average holding weights have climbed back towards the highs of the last decade.

Stock holdings are fairly concentrated, with 62% of allocations directed towards the top 3 holdings of National Grid plc, SSE plc and Northumbrian Water, though UK managers are raising exposure in 2nd tier names such as Centrica, Drax Group and United Utilities. There is clearly some depth to the sector.

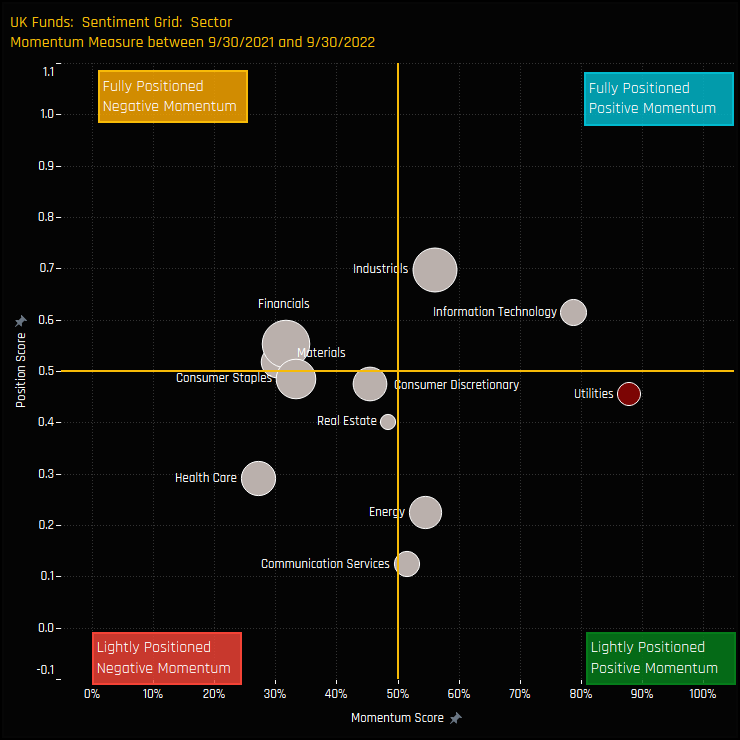

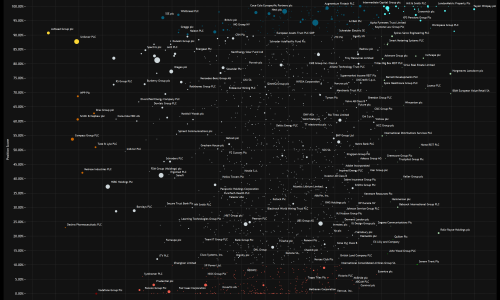

The chart to the right shows where current positioning in each UK sector sits versus history going back to 2011 on a scale of 0-100% (y-axis), against a measure of fund activity for each sector between 09/30/2021 and 09/30/2022 (x-axis). Utilities sit in the far right of the Grid, indicative of strong momentum among managers compared to all other sectors over the period.

On the positioning front, there is clearly headroom for allocations to move higher from here – remember there are 22.5% of managers still opting out of the Utilities sector entirely. For that to happen, the sector has to hold some appeal for Growth investors, who so far are significantly underinvested compared to their Value/Yield peers.

See below for more detailed profiles of the 5 key stock holdings in the Utilities sector, together with a link to the UK Active Fund Ownership Report for the Utilities sector.

National Grid plc

SSE plc

Northumbrian Water

Drax Group plc

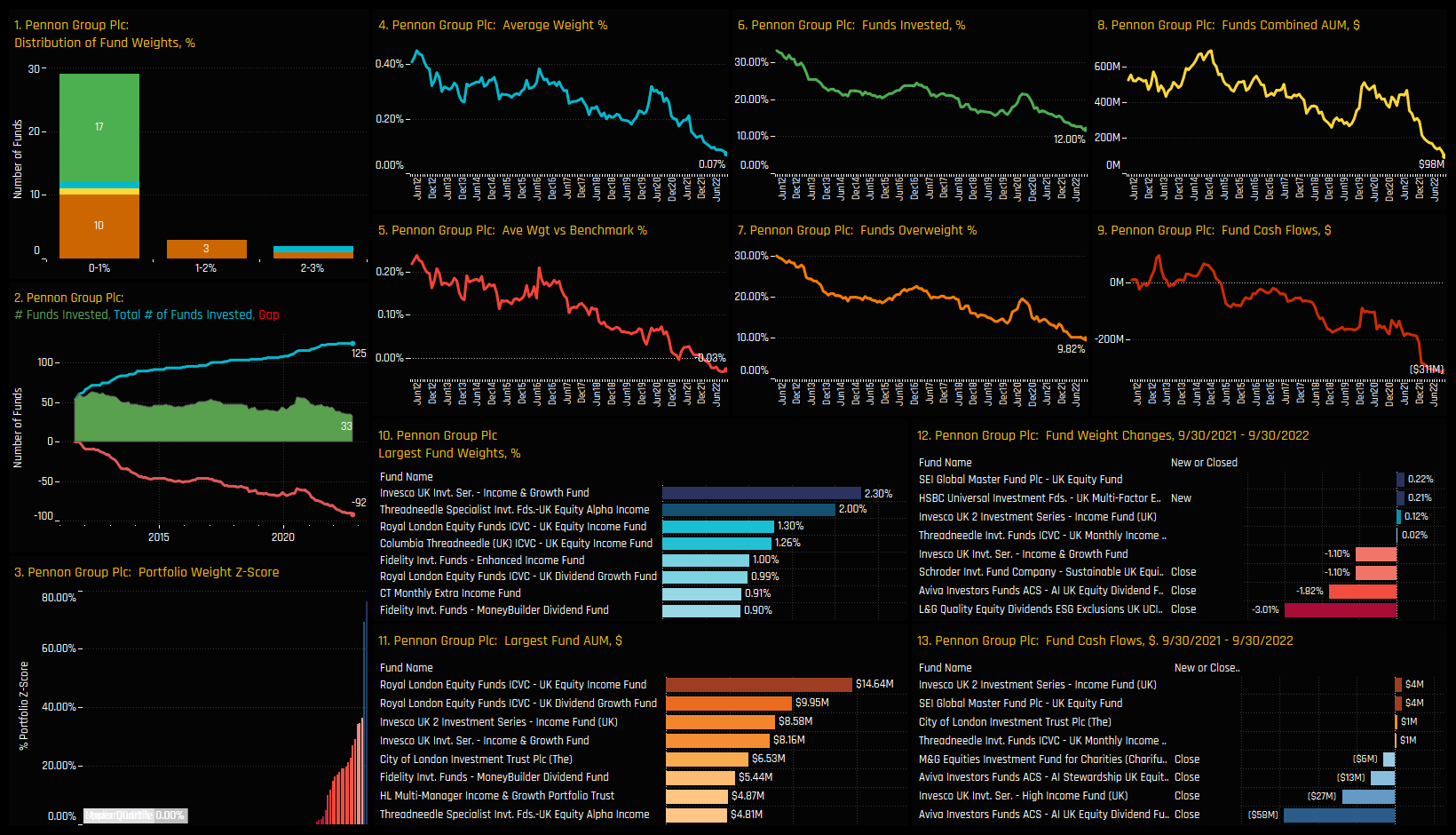

Pennon Group plc

Click on the link below for the latest data report on Utilities positioning among active UK funds.

For more analysis, data or information on active investor positioning in your market, please get in touch with me on steven.holden@copleyfundresearch.com

{kind=link}