05 March

UK Insights

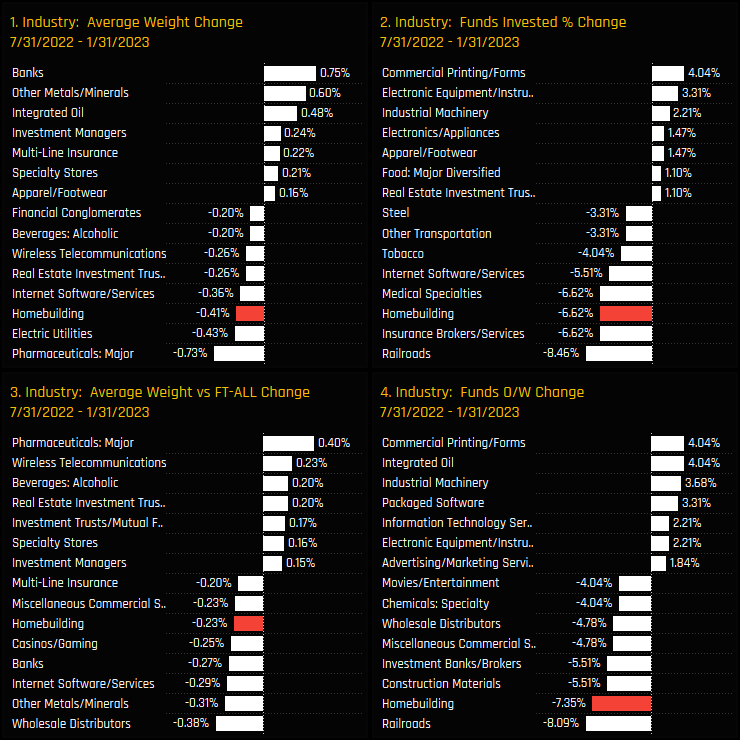

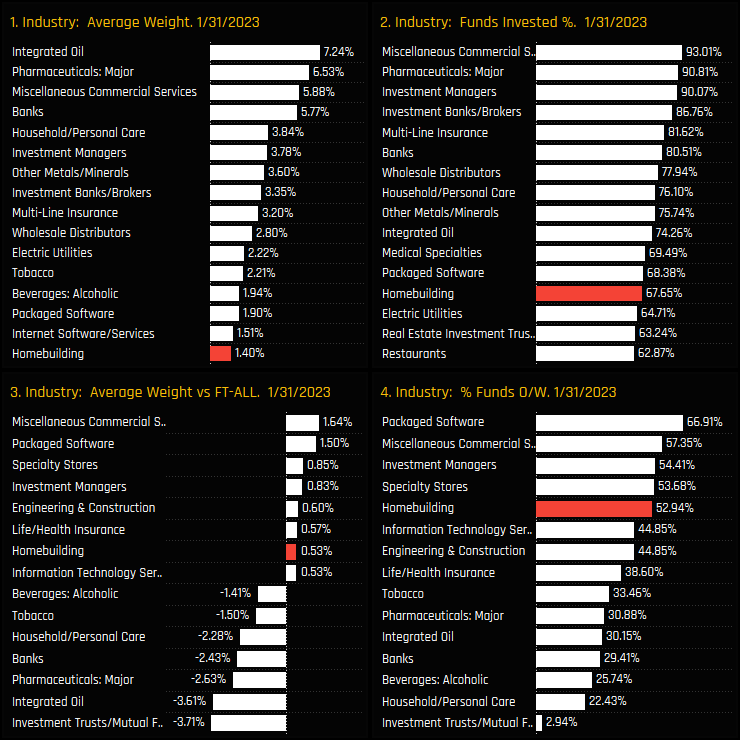

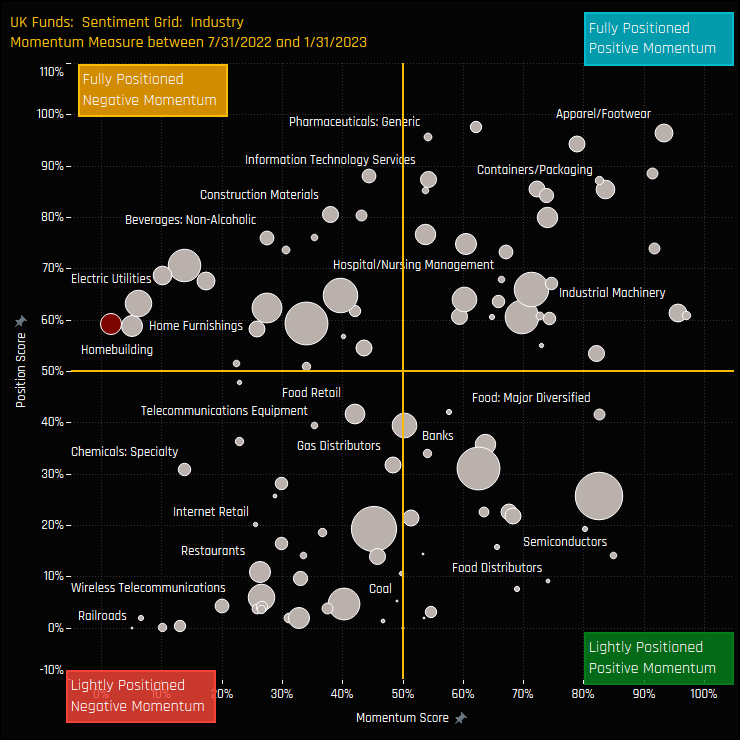

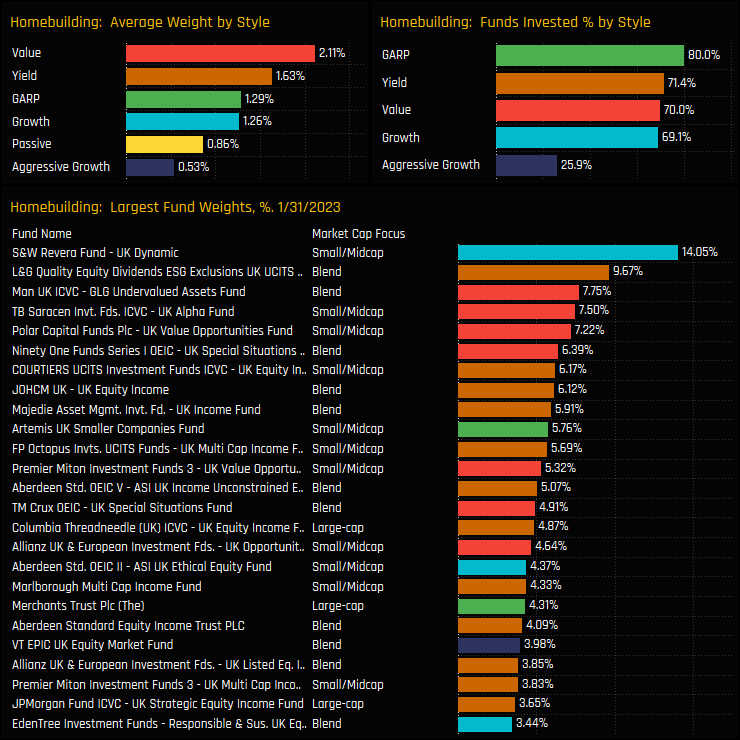

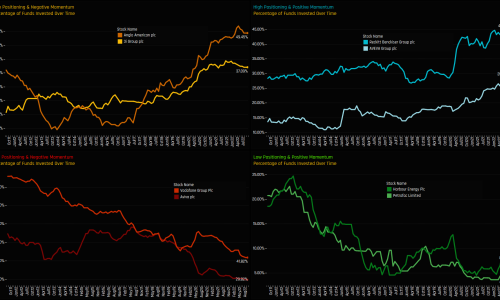

UK Homebuilders: Momentum Reversal Among UK Equity Managers

- Steve Holden

- 0 Comments

Related Posts

{kind=link}