29 January

Global Insights

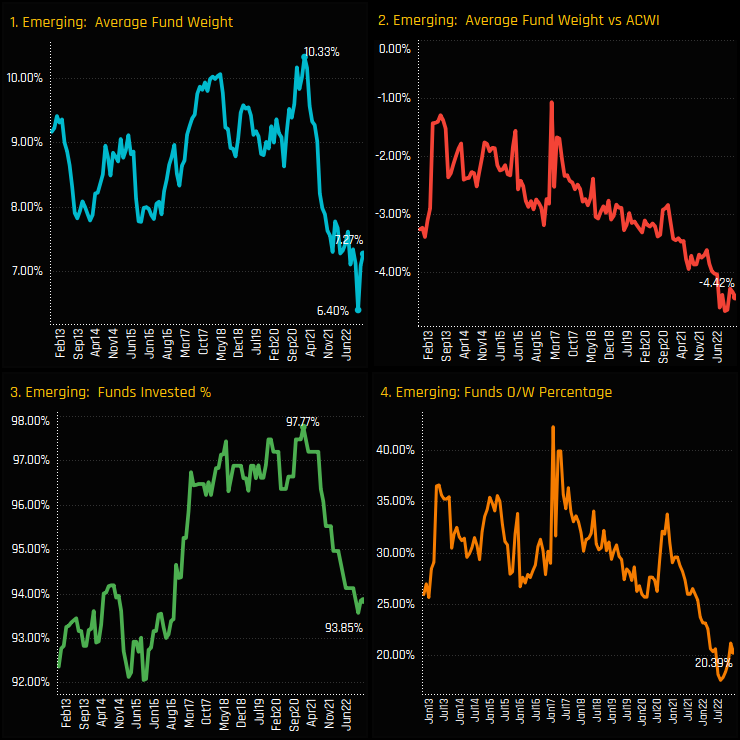

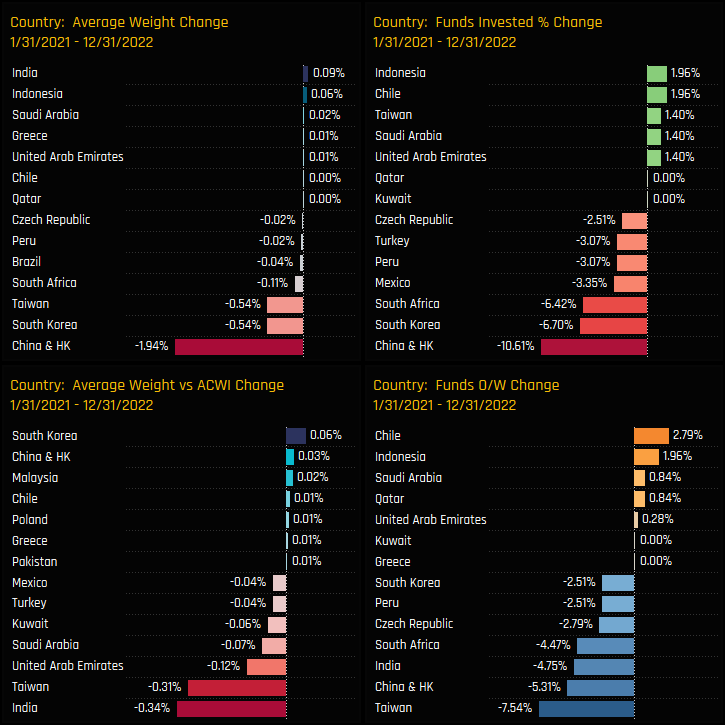

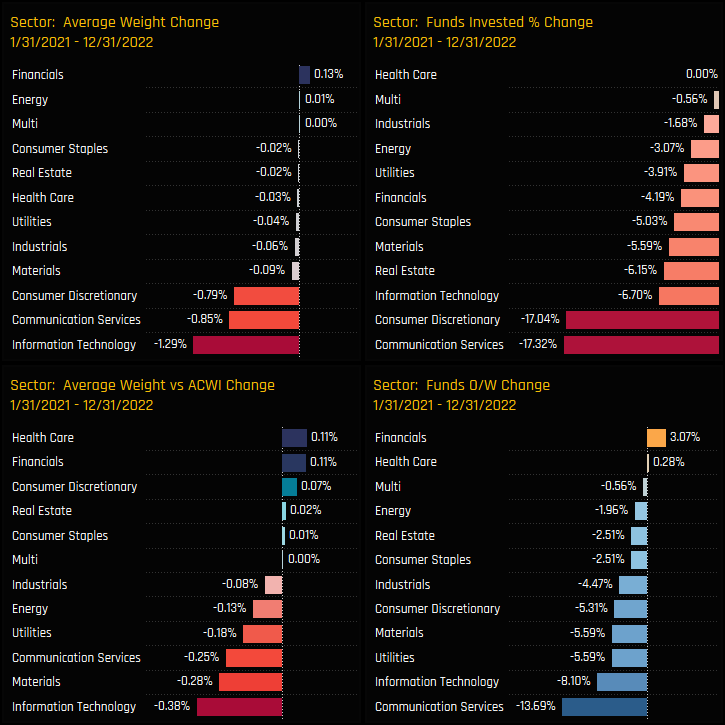

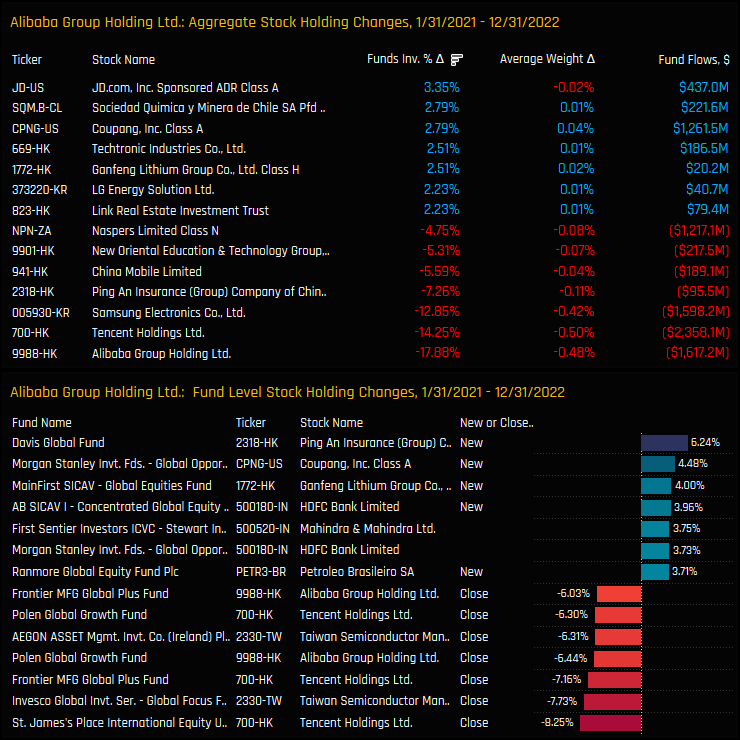

Global Funds: Record Under-Allocation in Emerging Markets

- Steve Holden

- 0 Comments

Related Posts

{kind=link}