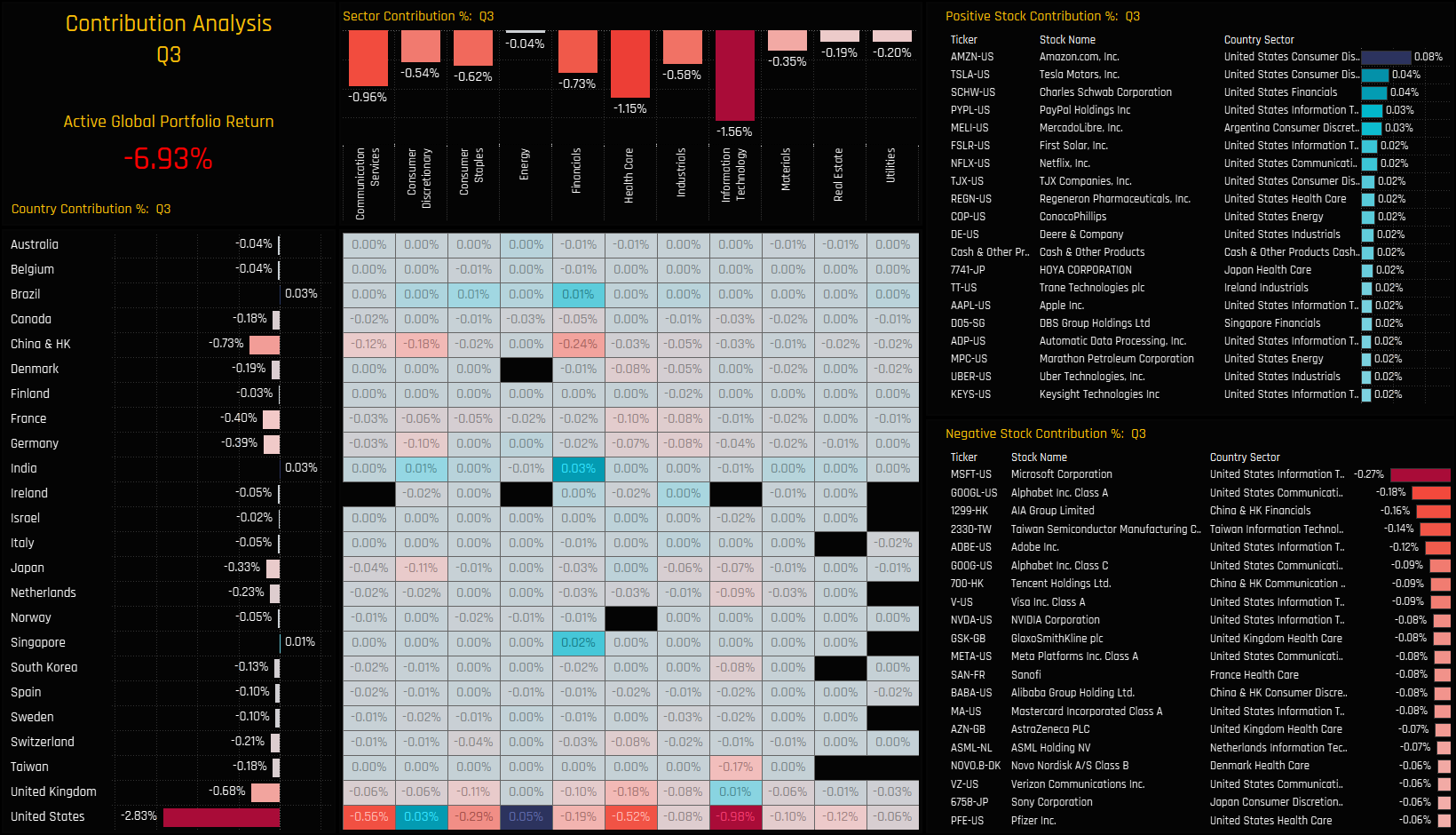

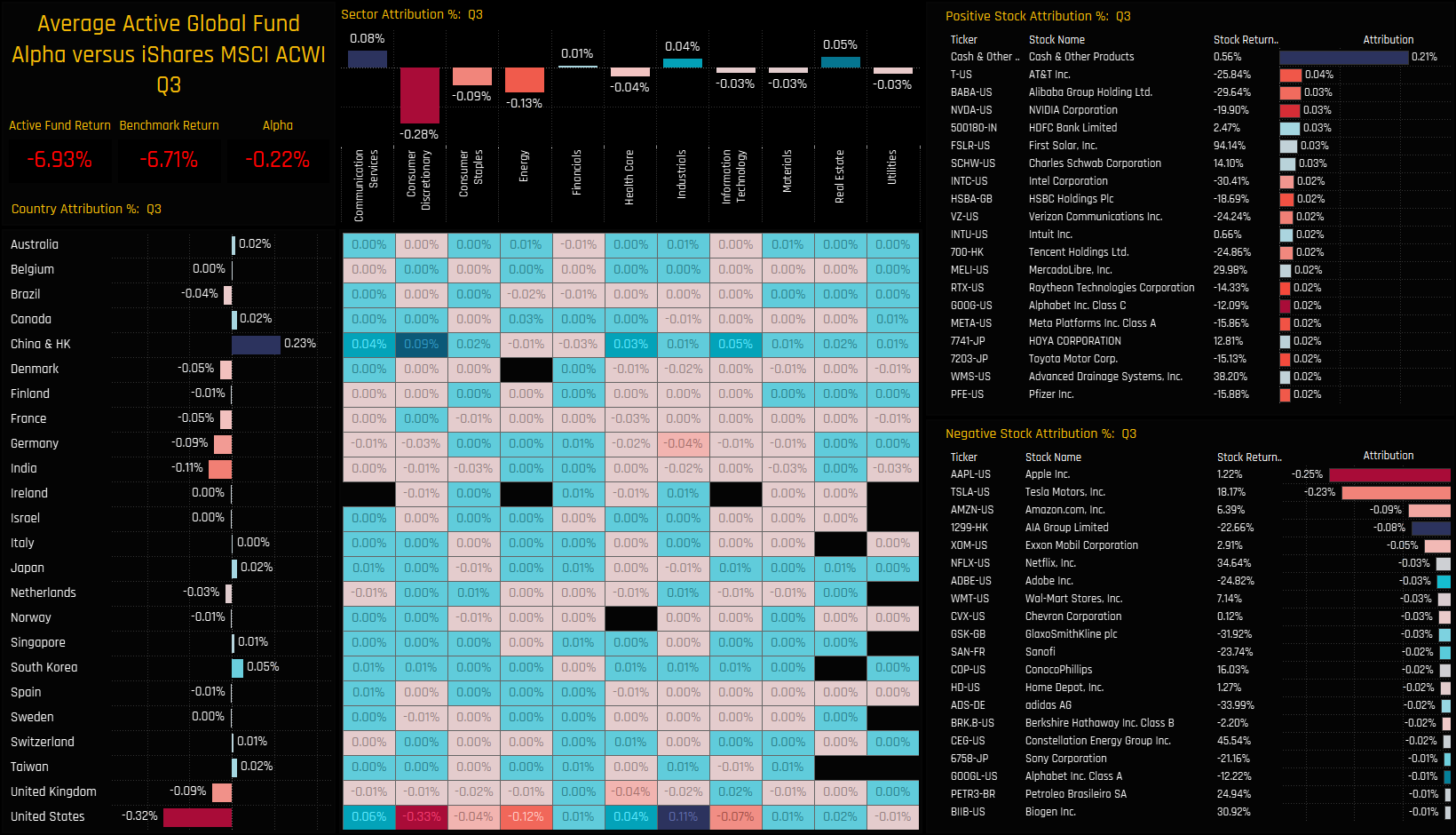

Marrying the performance of each portfolio component with the relative overweights and underweights in the active portfolio provides the attribution of each country, sector and stock towards the overall underperformance of -0.22% on the quarter. Again, this differs slightly from the underperformance of -0.17% derived from the fund performance for the reasons stated above, and the fact that we are using the ETF and not the MSCI Index. Reflecting the fact that performance between active and passive was largely in line, there were few standout generators of relative gains or losses. The underweight in China & HK generated positive outperformance of +0.23%, but this was offset by the outperformance of US Consumer Discretionary underweights, led by Apple Inc and Tesla Motors.

{kind=link}