25 March

Emerging Markets

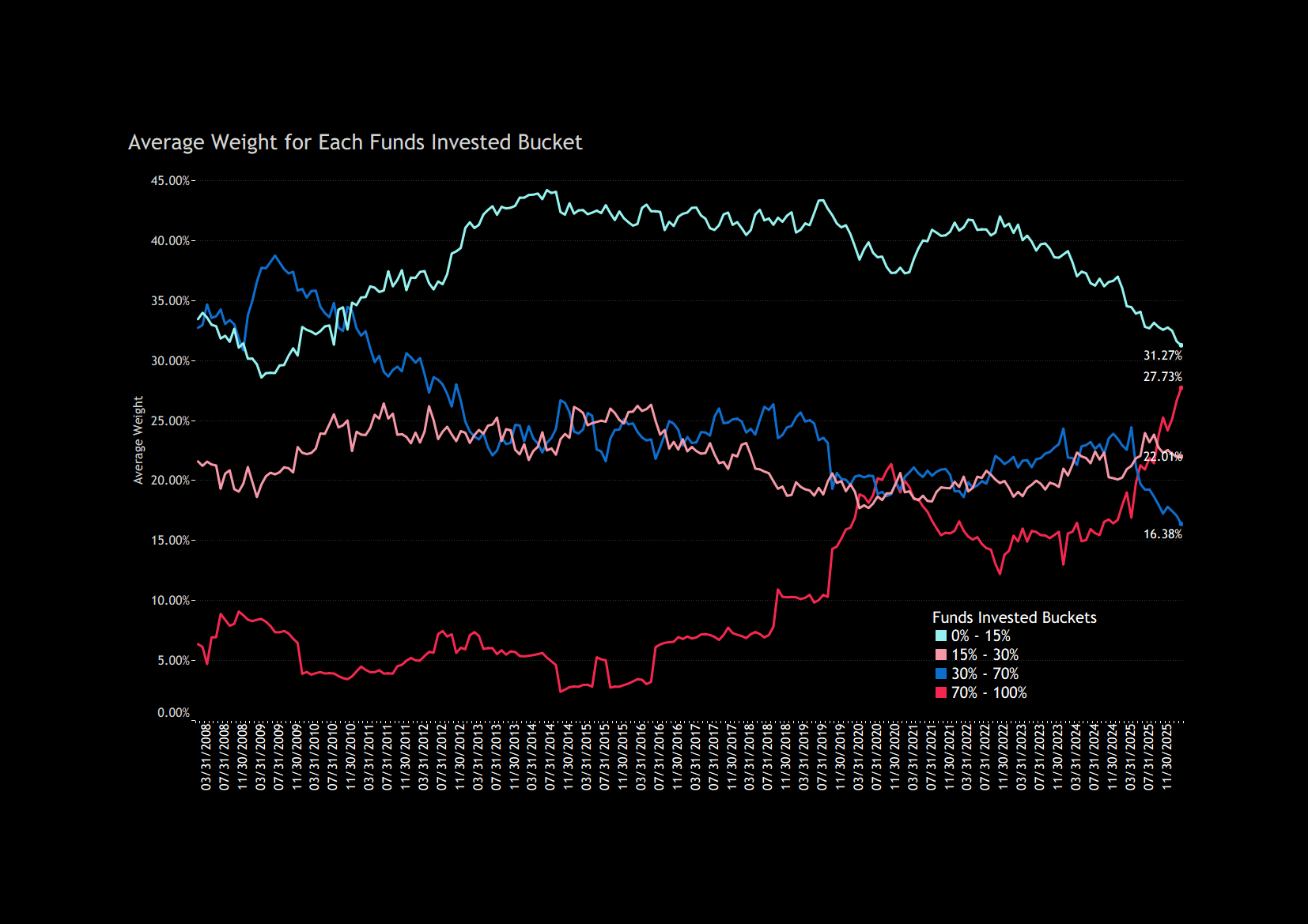

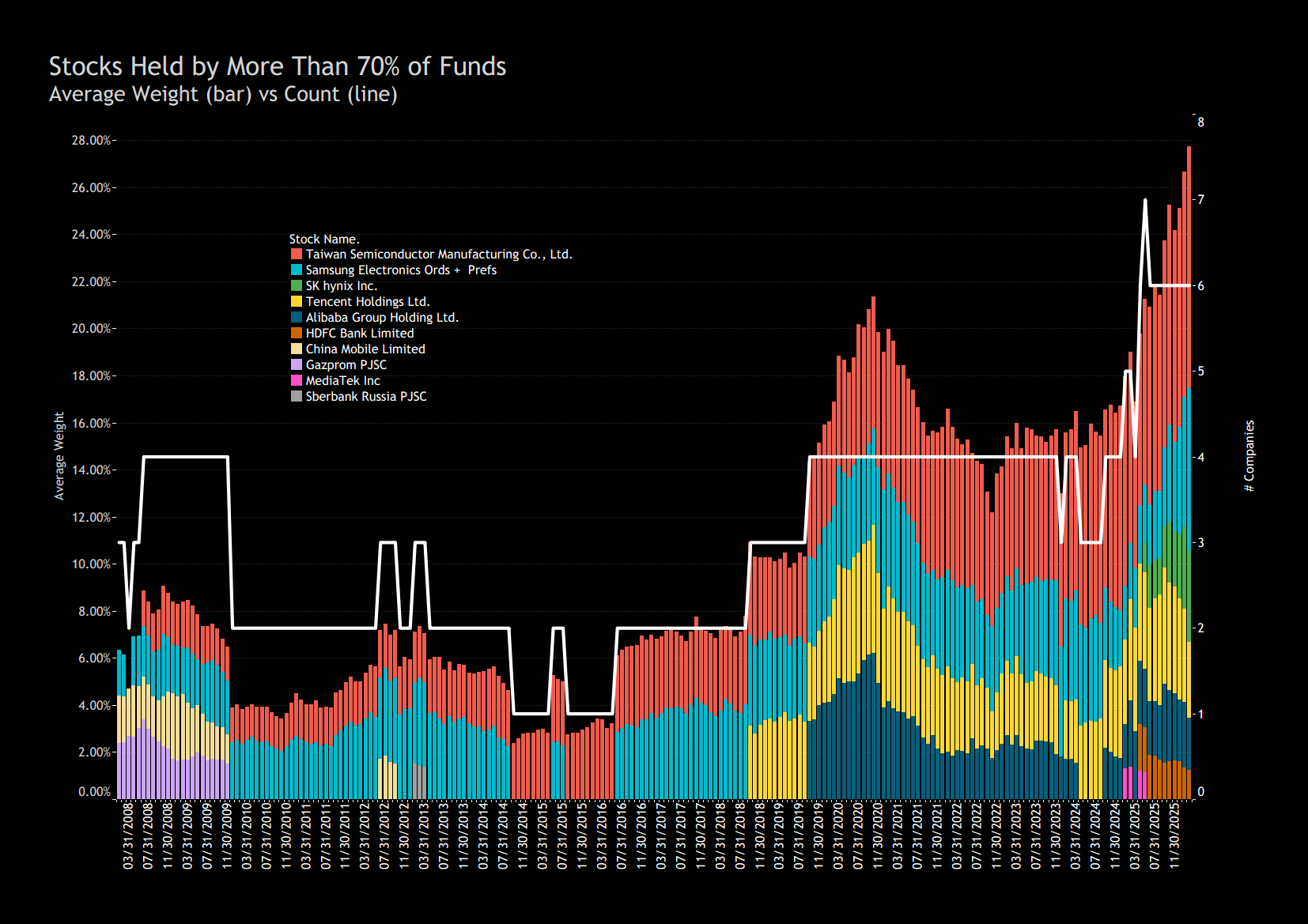

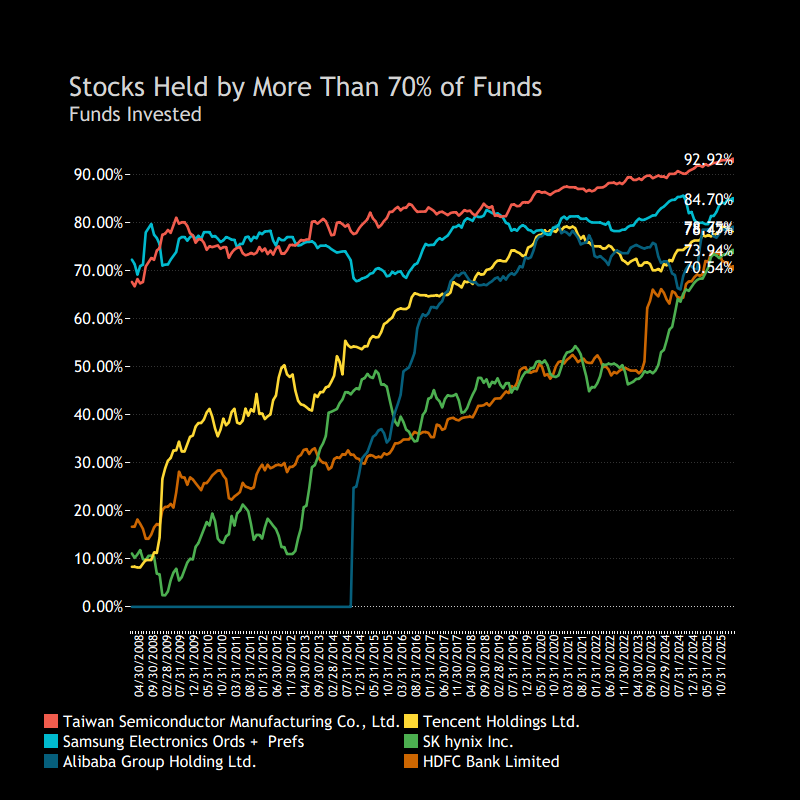

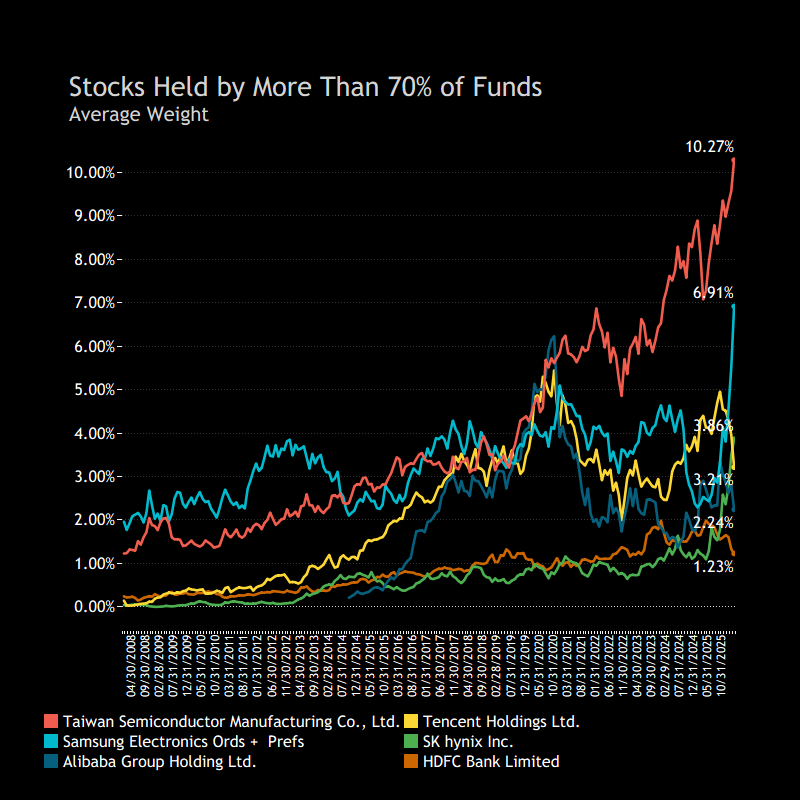

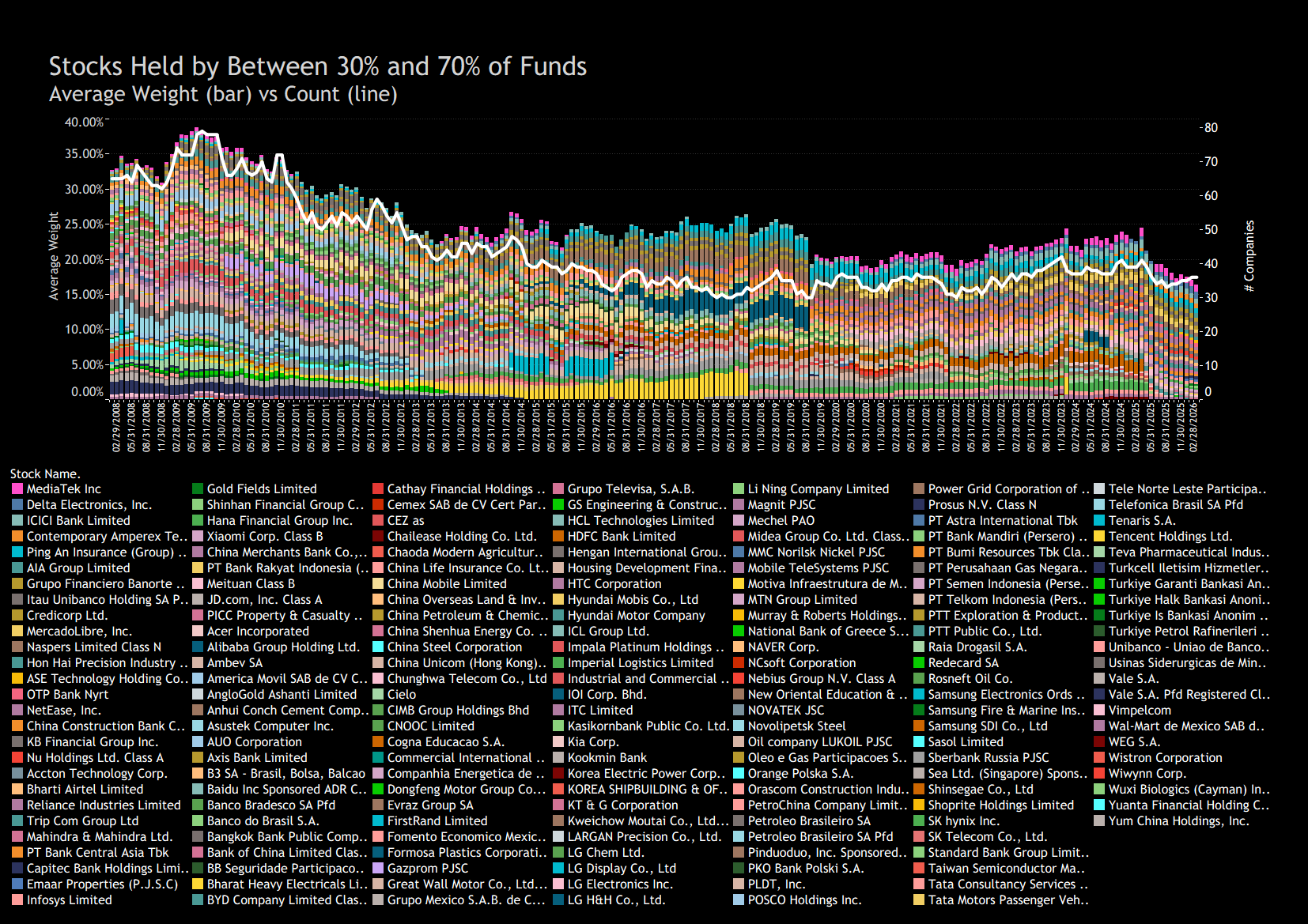

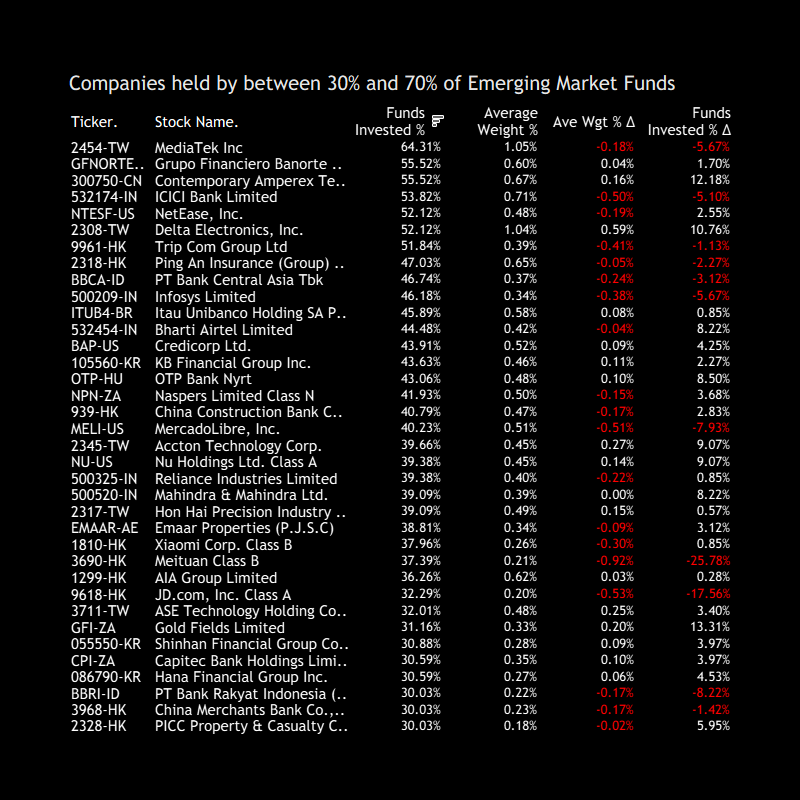

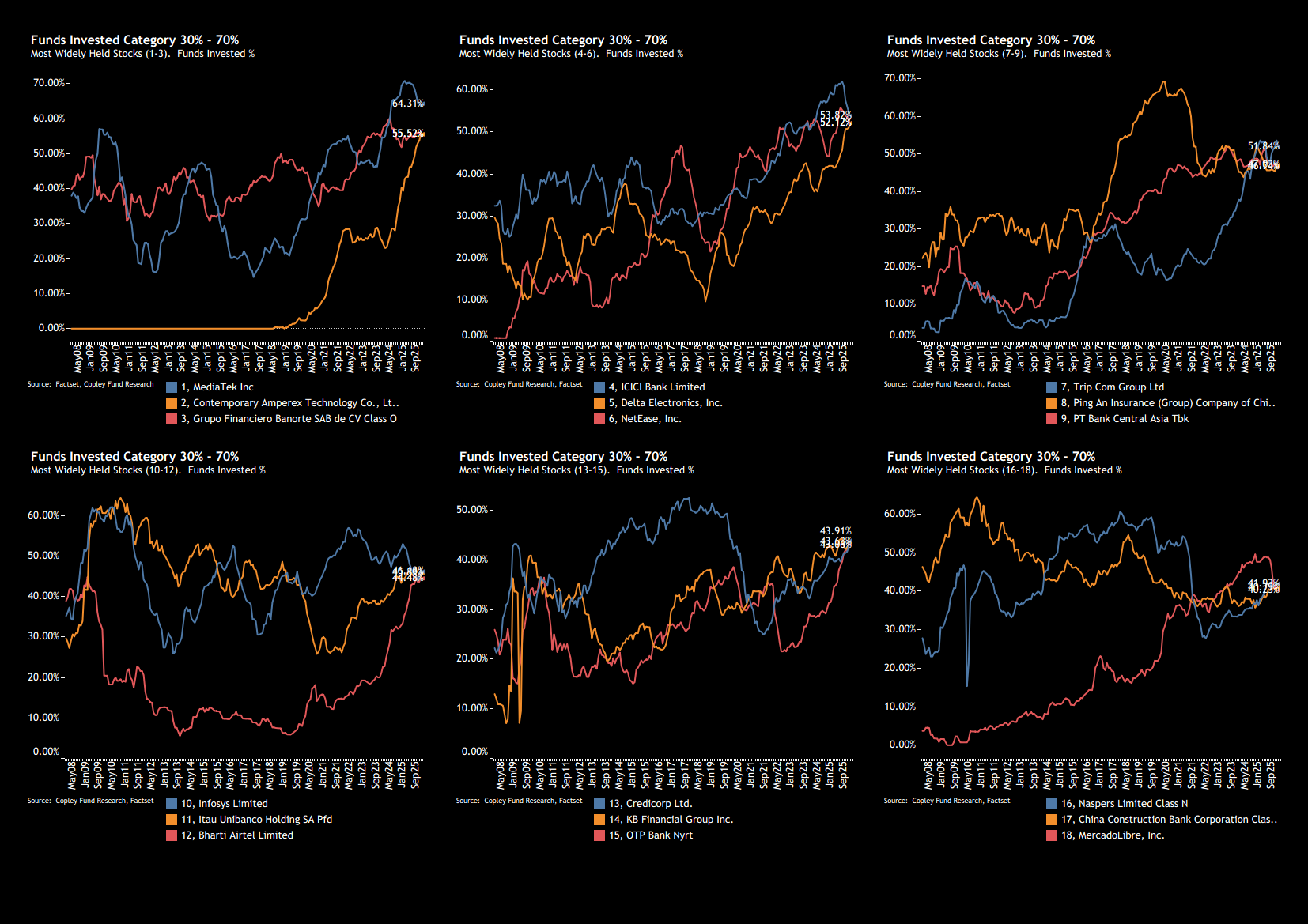

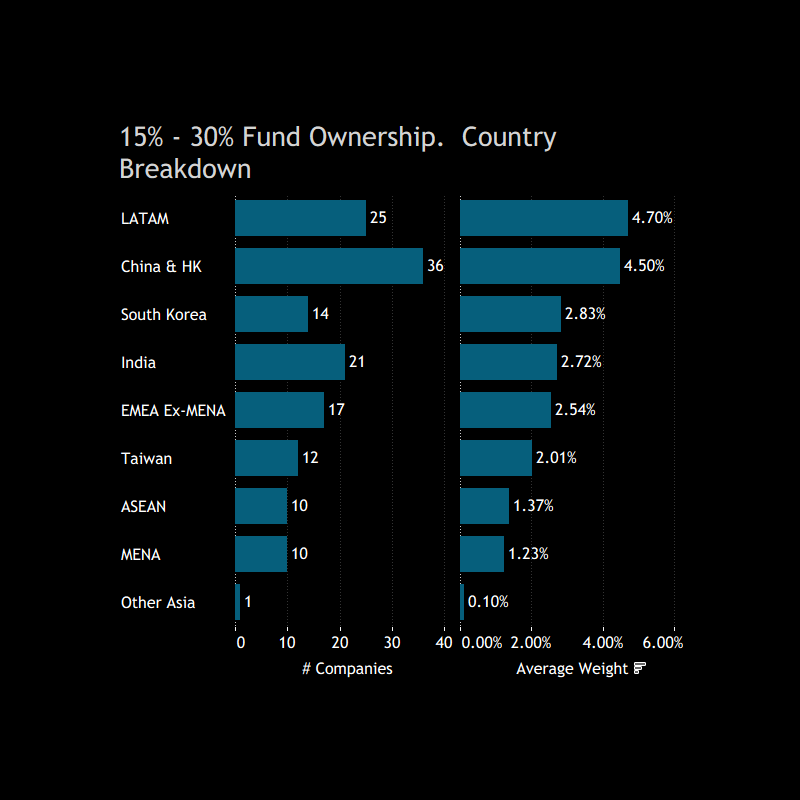

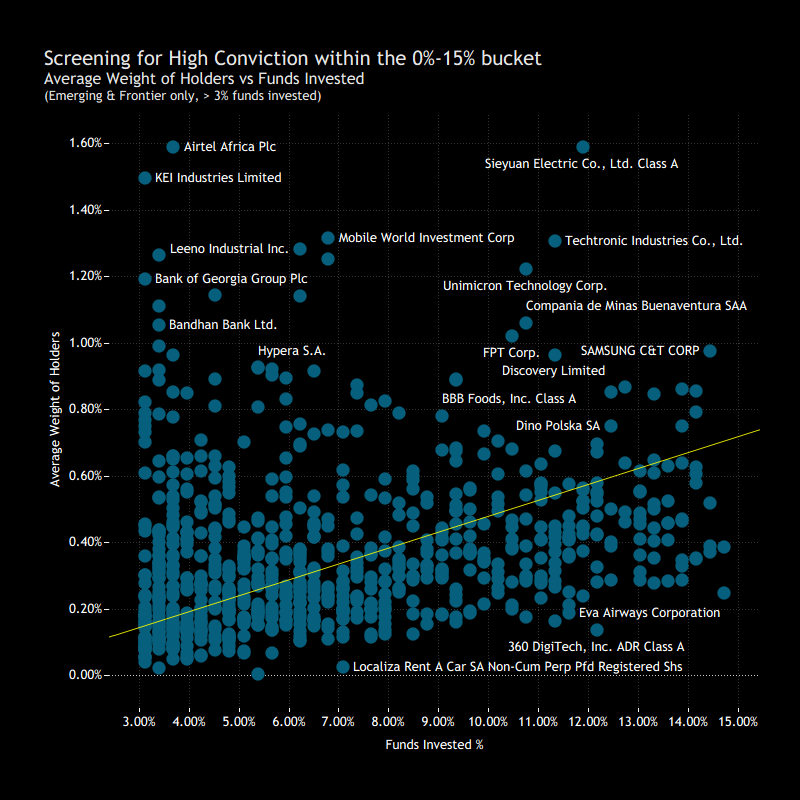

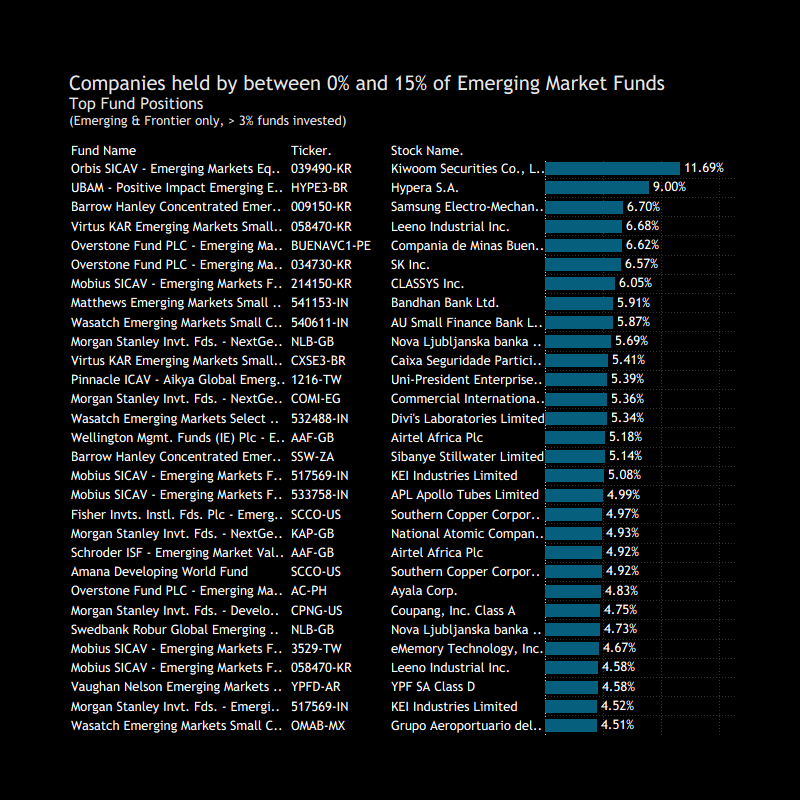

Emerging Markets Stock Radar: Positioning Concentrates as the Middle Hollowes Out

- Steve Holden

- 0 Comments

Related Posts

{kind=link}