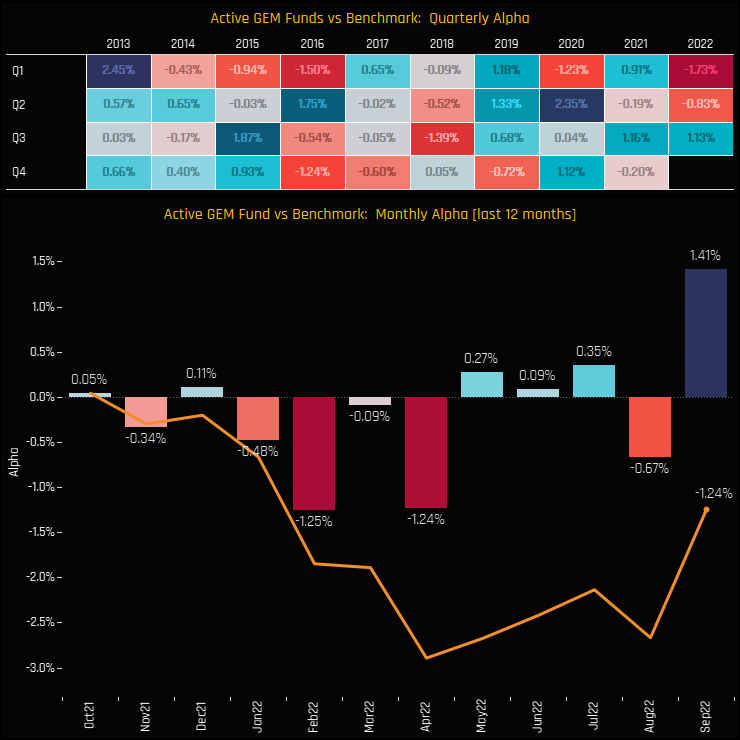

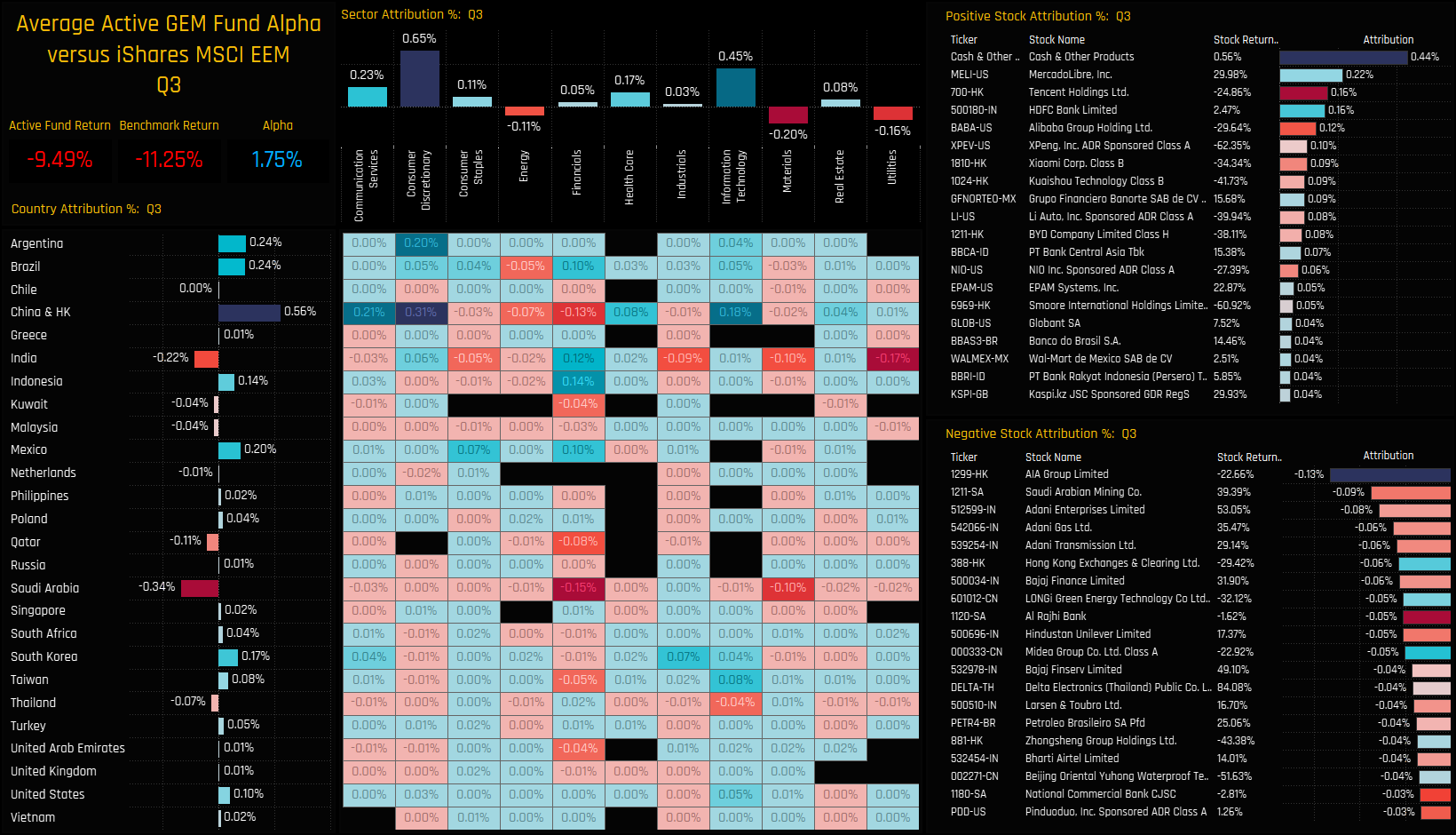

Marrying the performance of each portfolio component with the relative overweights and underweights in the active portfolio provides the attribution of each country, sector and stock towards the overall outperformance of +1.75% on the quarter. Again, this differs slightly from the outperformance of +1.13% derived from the fund performance for the reasons stated above, and the fact that we are using the ETF and not the MSCI Index. Nevertheless, the drivers of the outperformance are clear, with the underweight in China & HK generating +0.56% of relative outperformance on the month, together with overweights in Brazil, Argentina and Mexico. Active managers lost out to underweights in Saudi Arabia (Financials, Materials), India (Utilities, Energy) and Energy (Brazil, China). On a stock level, Cash was king in a falling market, generating +0.44% of relative outperformance, together with overweights in MercadoLibre and underweights in Tencent Holdings. Relative underperformance was down in part to overweights in AIA Group, underweights in Saudi Arabian Mining Co and the 3 high performing Indian Utility stocks.

{kind=link}