28 April

Emerging Markets

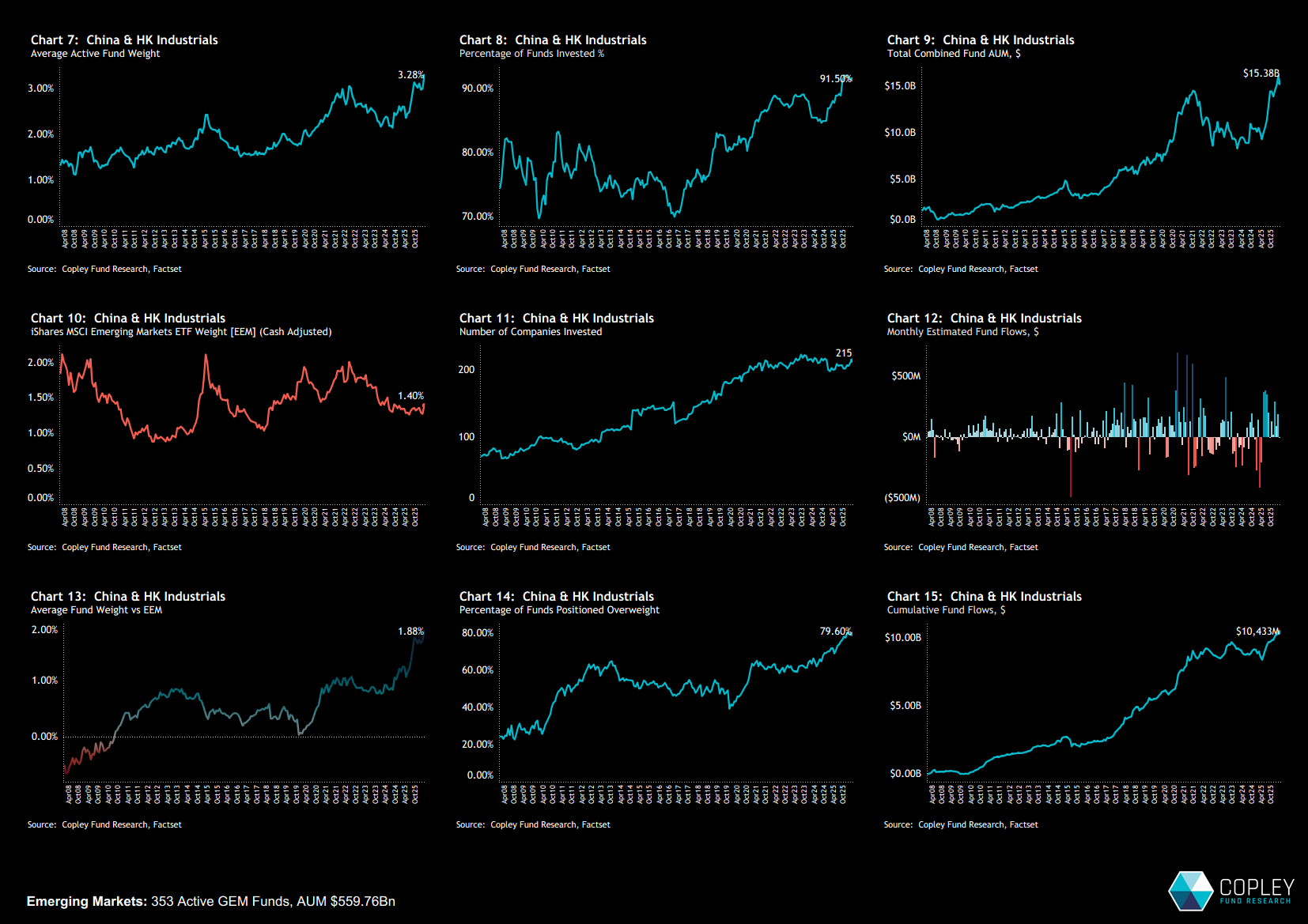

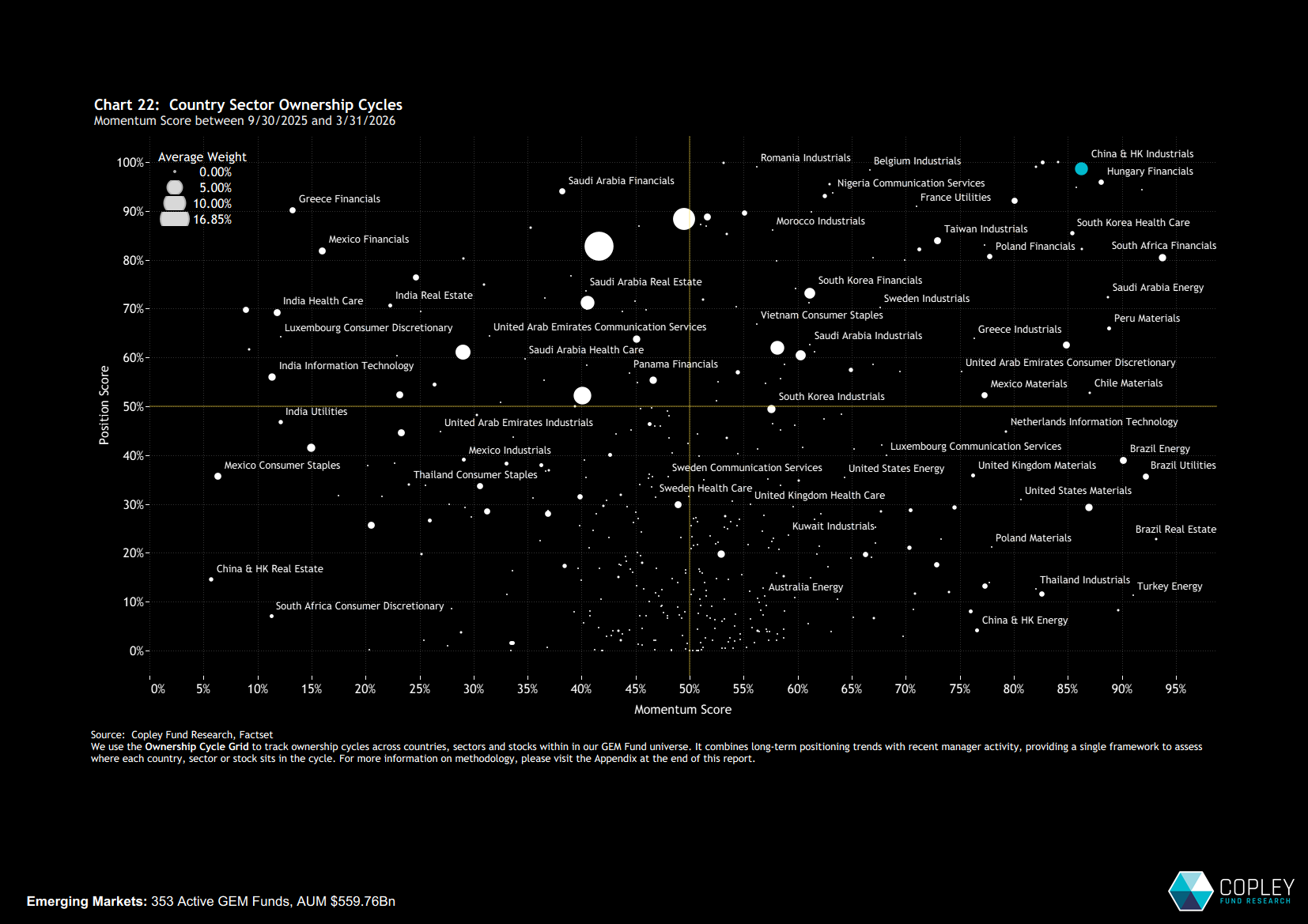

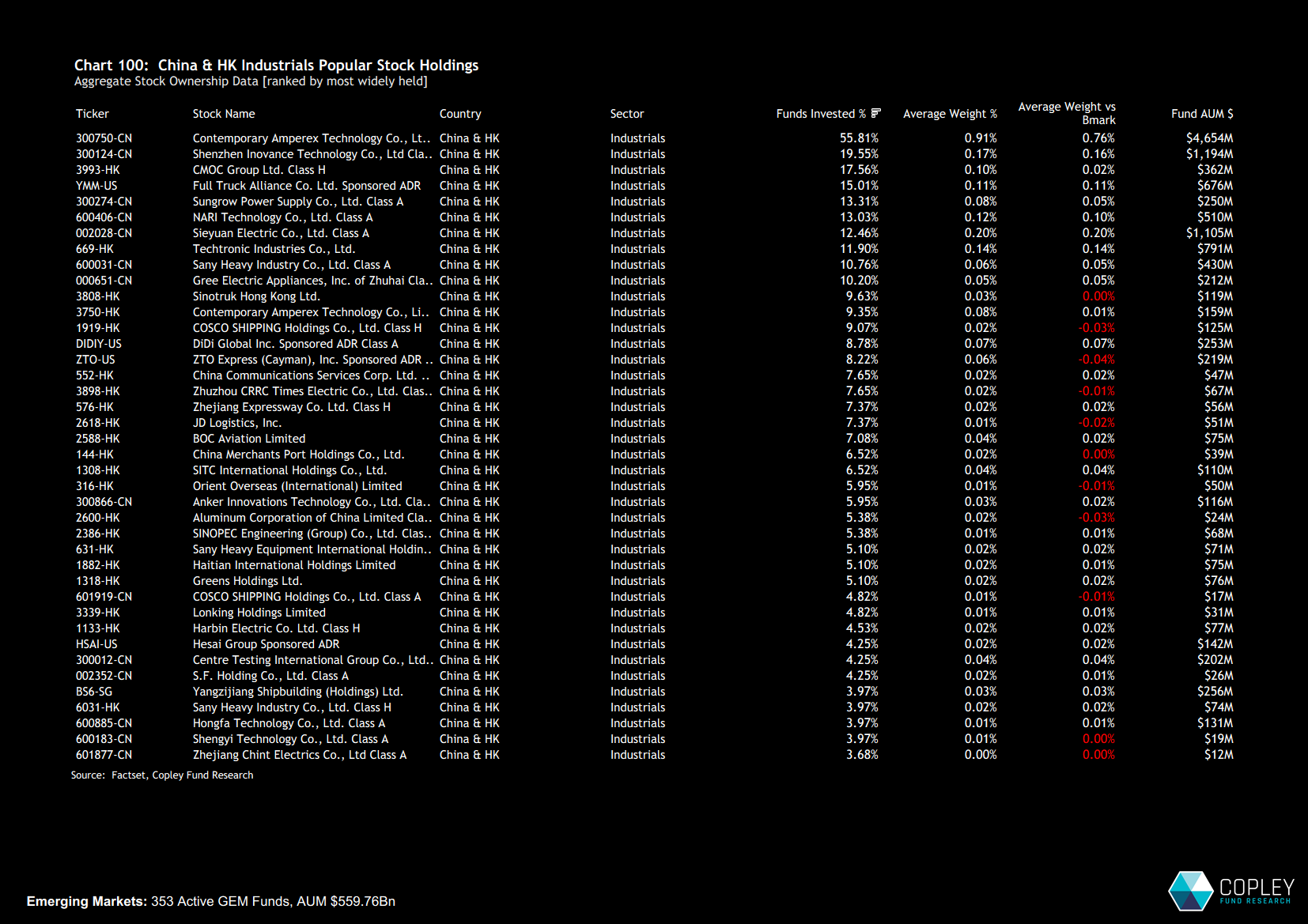

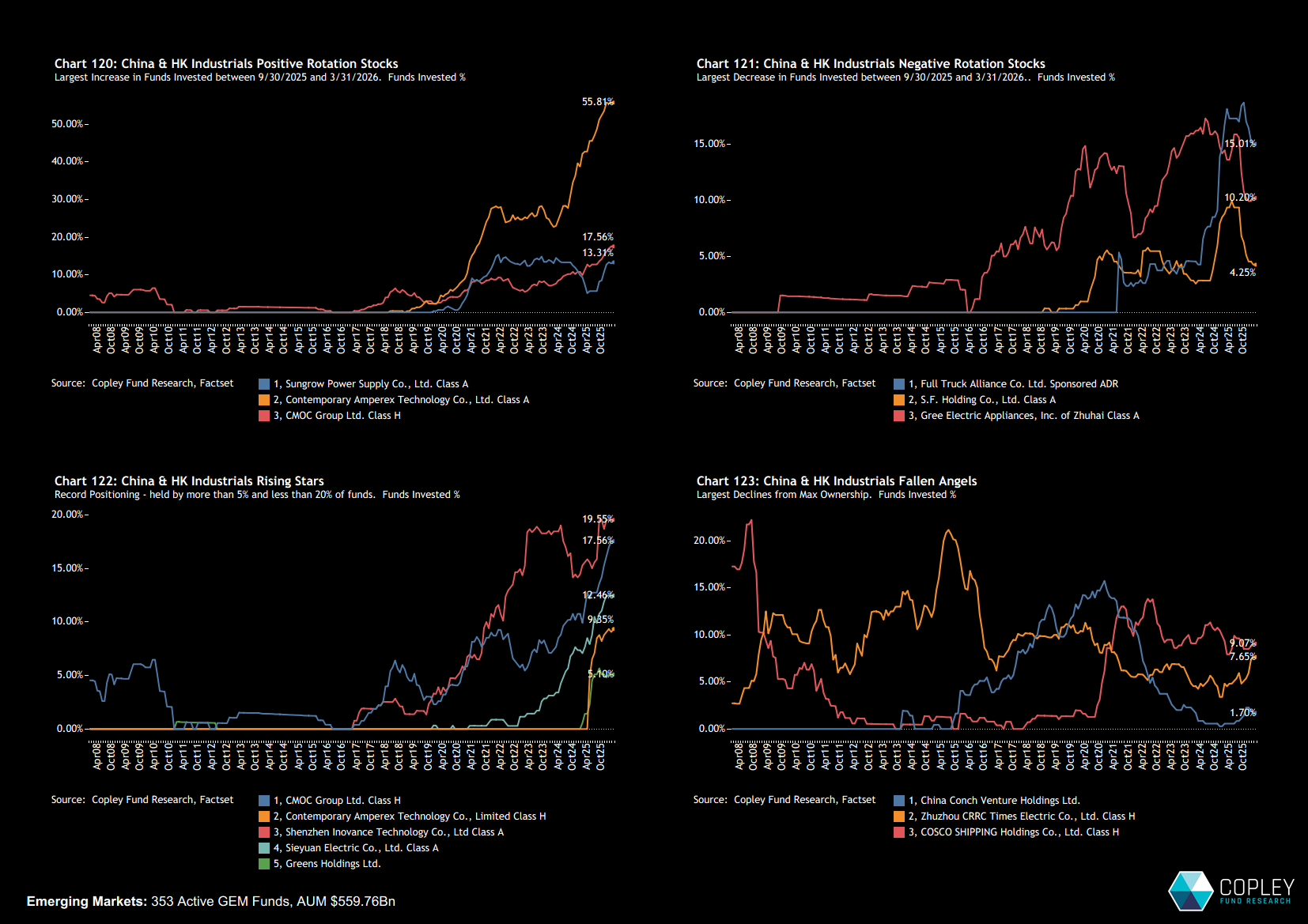

China Industrials: Bullish Positioning Strengthens Further

- Steve Holden

- 0 Comments

Related Posts

{kind=link}