Active Asia Ex-Japan Funds: Performance & Attribution Q1 2026

April 30th 2026

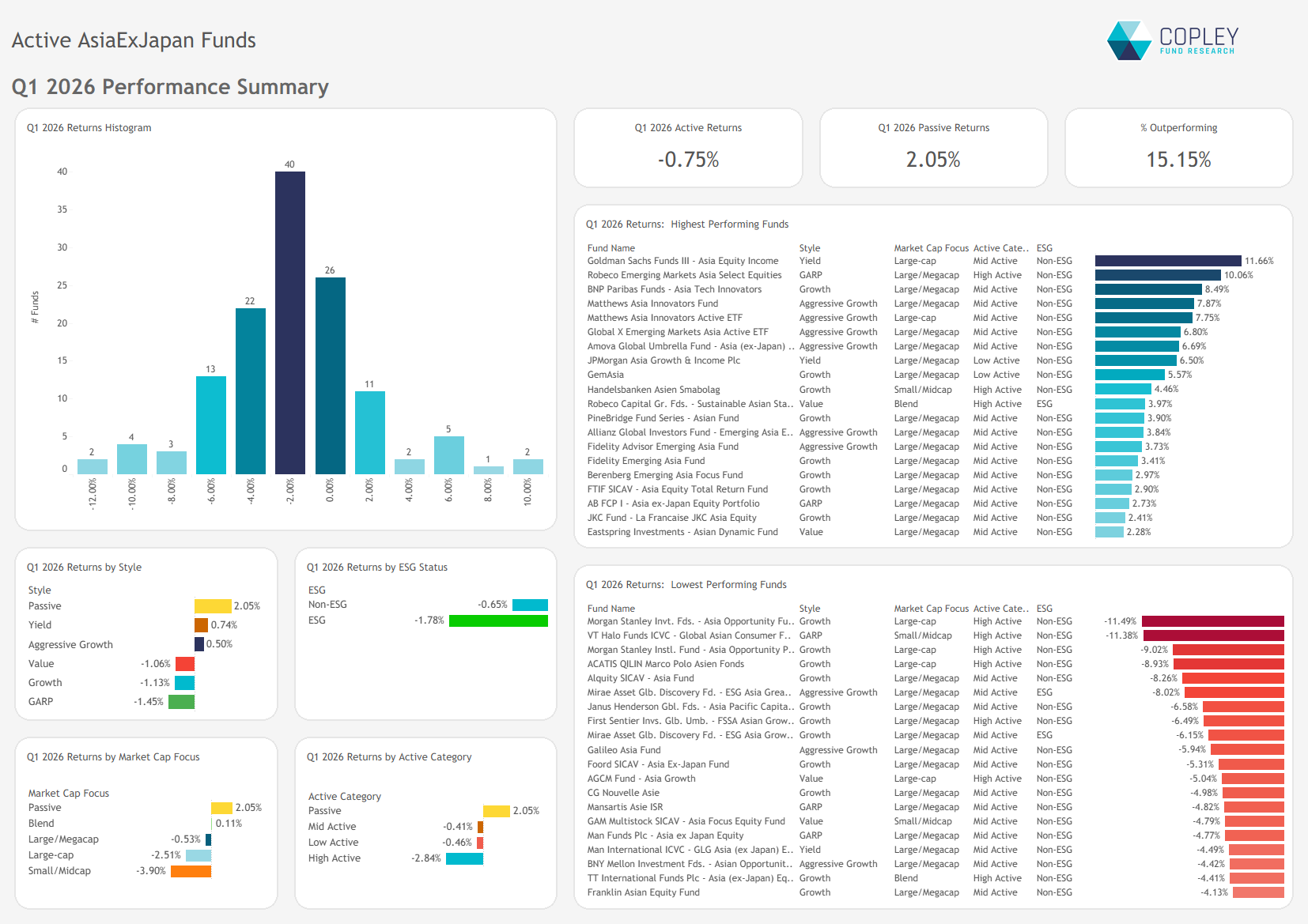

Active Asia ex-Japan funds fell -0.75% in Q1, but the iShares MSCI All Country Asia ex Japan ETF rose +2.05% due to systematic fair value pricing, versus -1.2% for the underlying index.

Narrow leadership, broader weakness: Gains were concentrated in Korea/Taiwan Technology and a handful of stocks, while China and India exposures dragged on overall returns.

Positioning mattered, but gaps remain: Overweights in Korean Tech helped, but underweights in TSMC and China/India positioning drove underperformance, leaving managers still playing catch-up after 2022–2025.

Flat on the Quarter Active Asia ex-Japan funds returned -0.75% over the quarter, with a wide dispersion: top performers delivered double-digit gains while laggards posted double-digit losses. The most common outcome sat in the -2% to 0% range.

The iShares MSCI All Country Asia ex Japan ETF returned +2.05%, a figure flattered by its use of “systematic fair value” pricing. Unlike most funds, which rely on local market closing prices, the ETF adjusts valuations post-close to reflect US market moves. On a like-for-like basis, the underlying benchmark index declined -1.2% over the quarter.

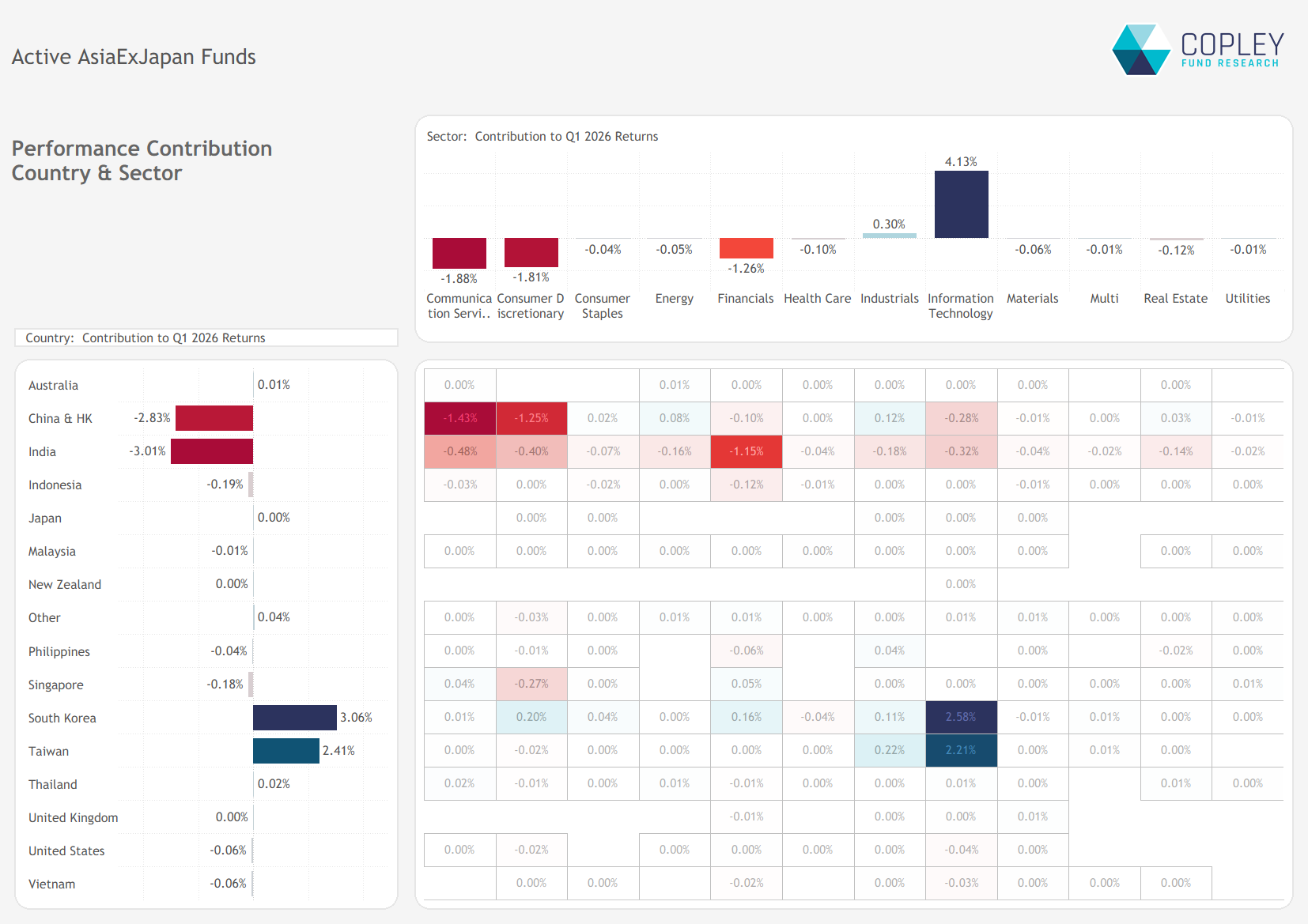

Regional Split The charts below break down Q1 return drivers by country and sector, based on aggregate manager holdings. At the sector level, Technology was the standout contributor, adding 4.1% to returns, but this was more than offset by weakness across Consumer Discretionary, Consumer Staples and Financials.

At the country level, Taiwan and South Korea were the only clear contributors, with gains outweighed by declines in China and India. Within South Korea, performance was driven not just by Technology, but also by contributions from Industrials, Financials and Consumer Discretionary.

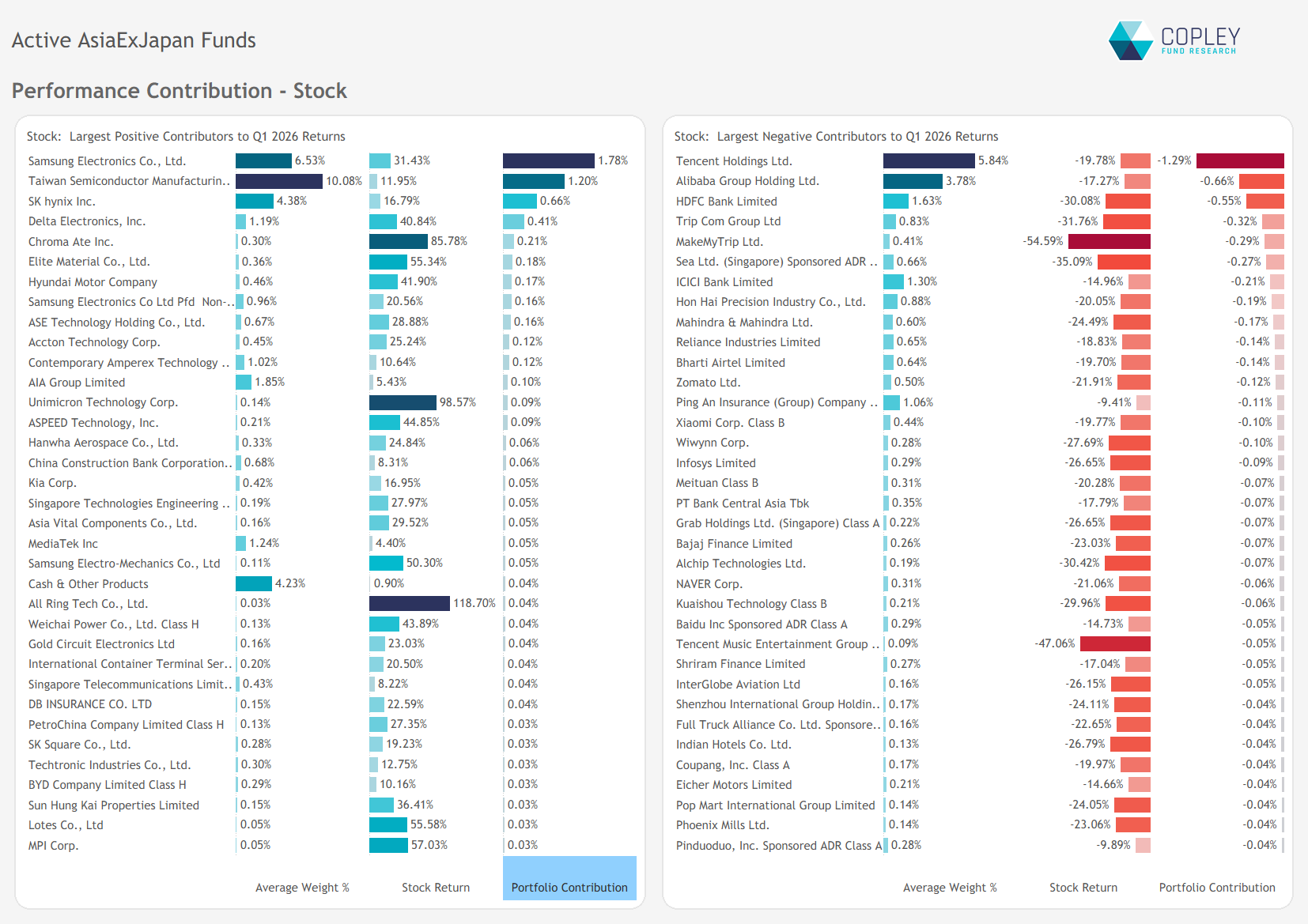

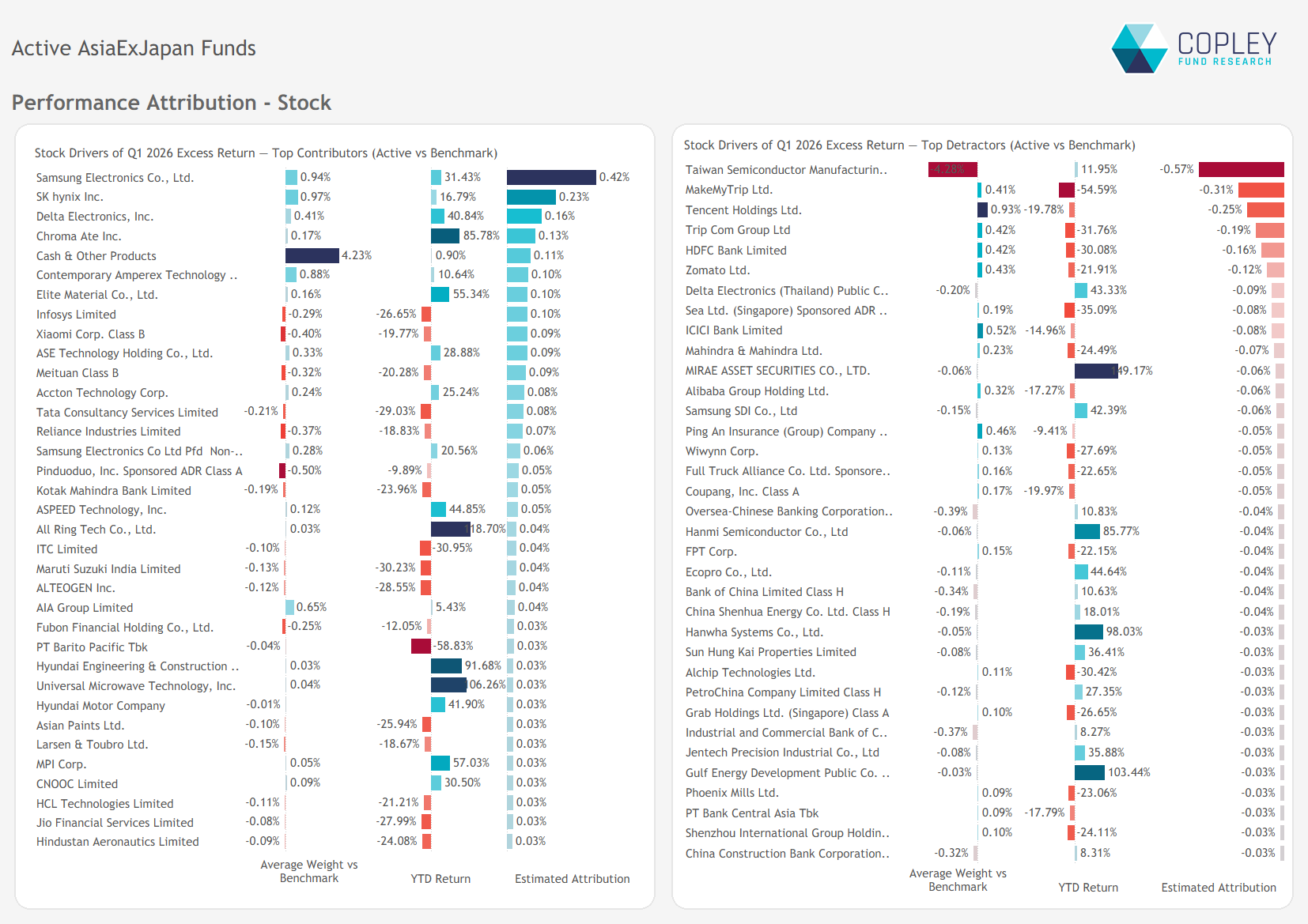

Stock-Level Influence At the stock level, gains were highly concentrated in four key names. Taiwan Semiconductor Manufacturing Company, Samsung Electronics, SK Hynix and Delta Electronics were the primary contributors, adding over 4% to total Q1 returns.

However, these gains were overwhelmed by weakness in core China and India positions. Tencent, Alibaba Group and HDFC Bank detracted a combined 2.5% on average, with further losses from positions in Trip.com Group, MakeMyTrip and Sea Limited.

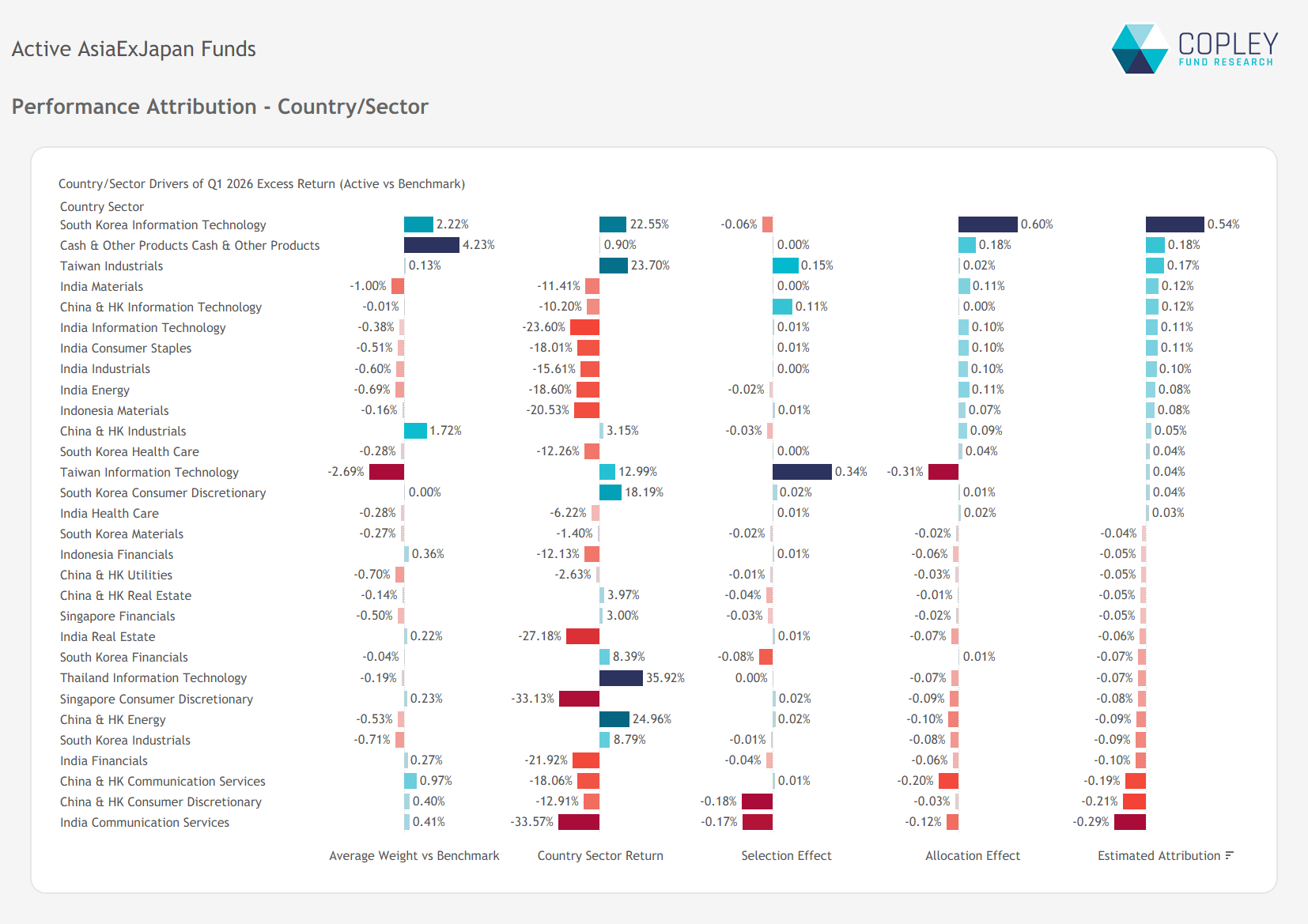

Performance Attribution – Where Funds made and lost versus the Benchmark The chart below breaks down the key drivers of relative performance at the country/sector level. Outperformance was led by overweights to South Korea Technology, cash holdings, and strong stock selection in Taiwan Industrials and China Technology.

On the flip side, underperformance was driven by overweights in China and India Communication Services, alongside weak stock selection in China Consumer Discretionary.

Stock Attribution Active EM managers benefited from net overweights in Samsung Electronics, SK Hynix and Delta Electronics, while underweights in Xiaomi and Infosys also supported relative performance.

On the negative side, the UCITS-driven underweight in Taiwan Semiconductor Manufacturing Company was a key drag, alongside overweights in MakeMyTrip, Tencent and Trip.com Group.

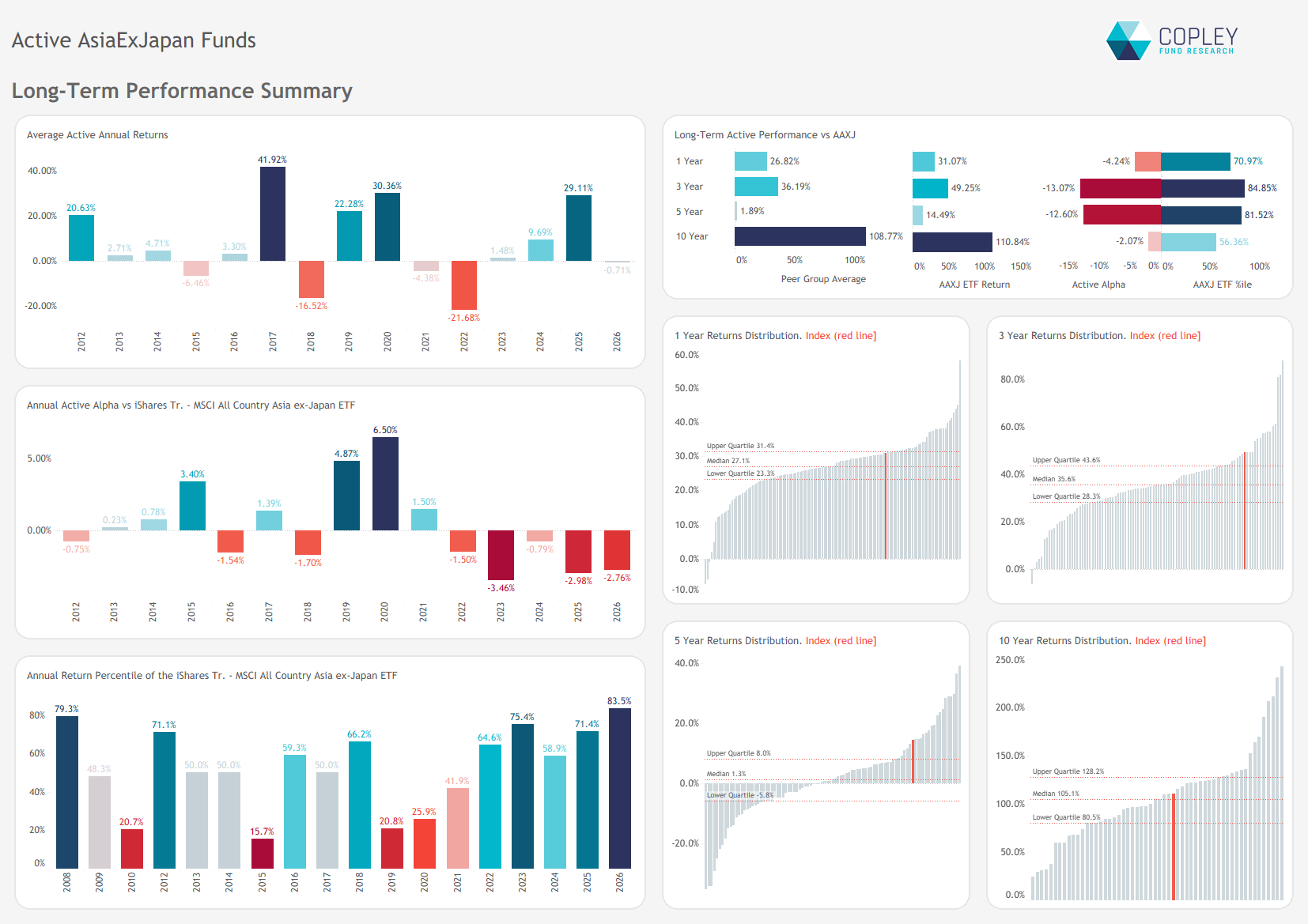

Long-Term Performance With the inflated returns of the iShares MSCI All Country Asia ex Japan ETF — driven by its use of systematic fair value pricing — active returns appear weaker than they should, creating what is effectively a short-term distortion rather than a true performance gap.

That said, managers still need to close the gap, with underperformance over 2022–2025 leaving little room for complacency.

Performance & Attribution Report

Click the link opposite for full charts and data detailing the drivers of Q1 2026 performance, along with a review of 3-, 5-, and 10-year results across the active Asia Ex-Japan peer group.

{kind=link}