UK Funds suffered another negative quarter, both in absolute terms and relative to the benchmark FTSE All Share benchmark. Only 25% of the funds in our analysis managed to beat the index, lead by poor performance from the Value and Small/Midcap end of the spectrum. Underperformance was driven by underweights in Shell, Glencore and Diageo and on a sector level, underweights in Consumer Staples and Materials, together with overweights in Consumer Discretionary.

Q3 Active Returns

Q3 was a tough quarter for active UK managers, both on an absolute basis and relative to benchmark. Average fund returns came in at -12.67%, lower than the SPDR FTSE All Share ETF by -1.32% with just 25.3% of funds outperforming. The underperformance was led by Value managers at the small/midcap end of the spectrum, with Aggressive Growth the only Style group to outperform the benchmark over the period.

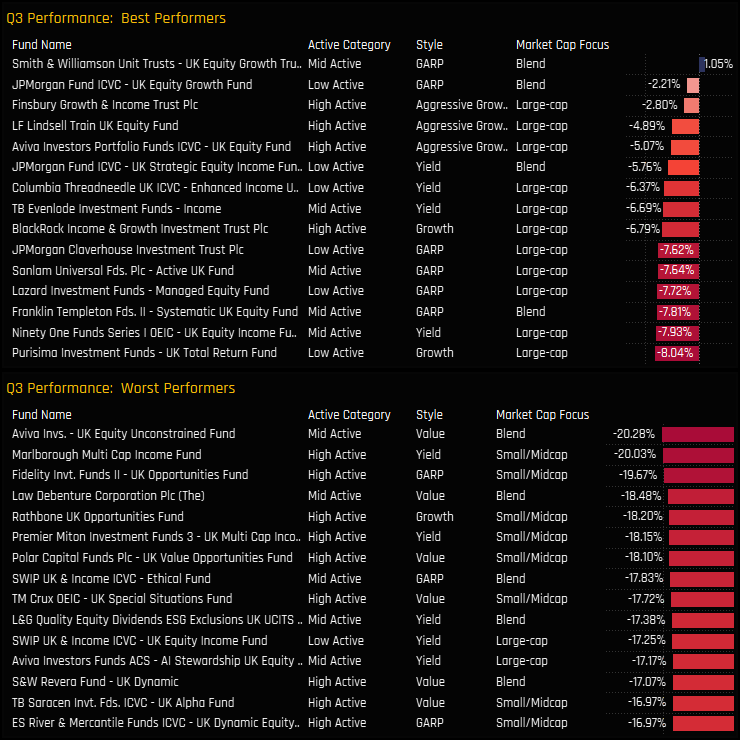

Smith & Williamson UK Equity Growth was the only UK fund to post positive returns in Q3, with fellow GARP stablemate JP Morgan UK Equity Growth in 2nd spot. The worst performers lost over a 5th of their value in Q3, led by Aviva UK Equity Unconstrained(-20.28%) and Marlborough Multi Cap Income (-20.03%). Small/Midcap strategies were prevalent among the bottom performers over the period.

Returns by Style & Market Cap Focus

The grid below shows the top 3 and bottom 3 performers in each Style and Market Cap bucket

Mid to Long-Term Performance

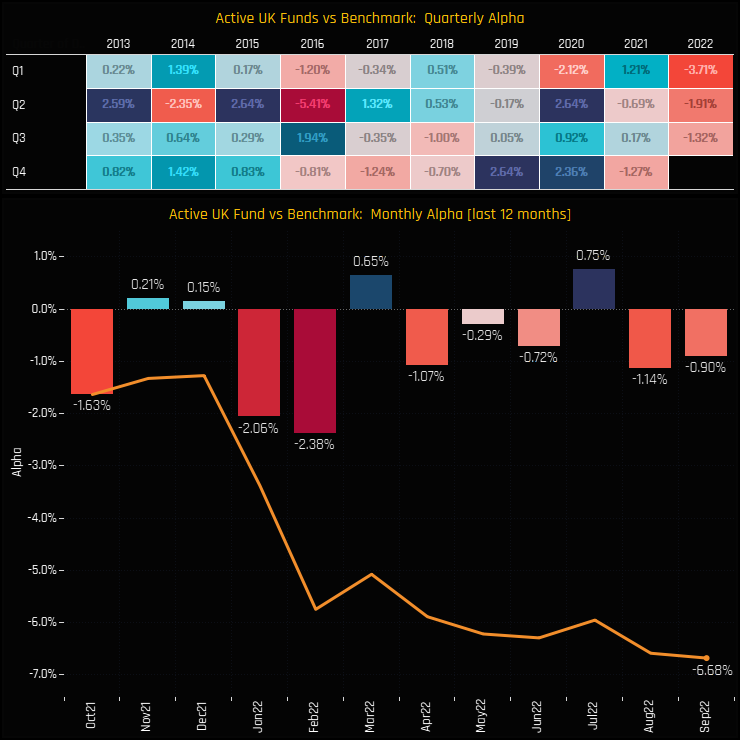

The underformance in Q3 added to the misery in both Q2 and Q1, with significant underperformance in each. Over the last 12-months, UK active managers have underperformed the SPDR FTSE All Share ETF by -6.68%, with 8 of the last 12 months generating negative alpha.

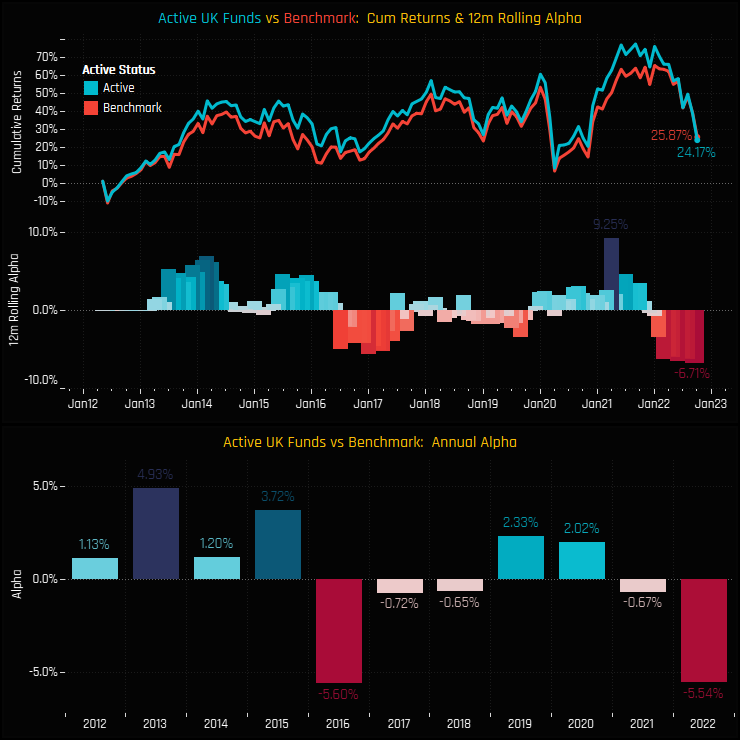

Over the longer-term, this recent period of underperformance is something of an outlier for UK active managers. With the exception of 2016, the last 10 years have been typified by either strong outperformance or minor undperformance.

The Drivers of Performance

We now analyse the drivers behind this quarter’s absolute and relative performance. We run performance analysis on the average stock portfolio generated from the holdings of the 275 funds in our UK analysis. This is the portfolio we use for our monthly positioning analysis. We compare this to the SPDRs FTSE All Share ETF (FTAL), cash removed and weights adjusted.

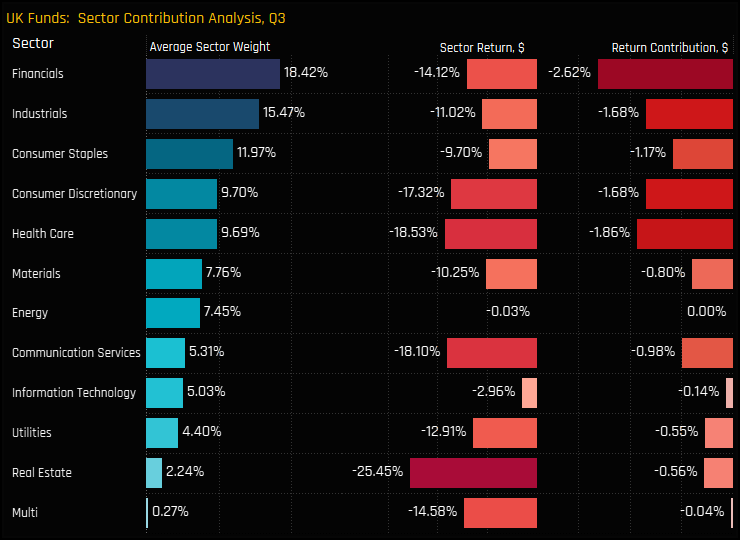

The chart below shows the breakdown of sector weights for the average active UK portfolio, it’s associated Q3 return and the contribution to the overall quarterly performance. Financials is the largest sector weight at 18.42%, and it’s -14.12% return on the quarter contributed -2.62% to overall returns. All sectors were down on the quarter, with Health Care and Consumer Discretionary also painful positions for active UK funds.

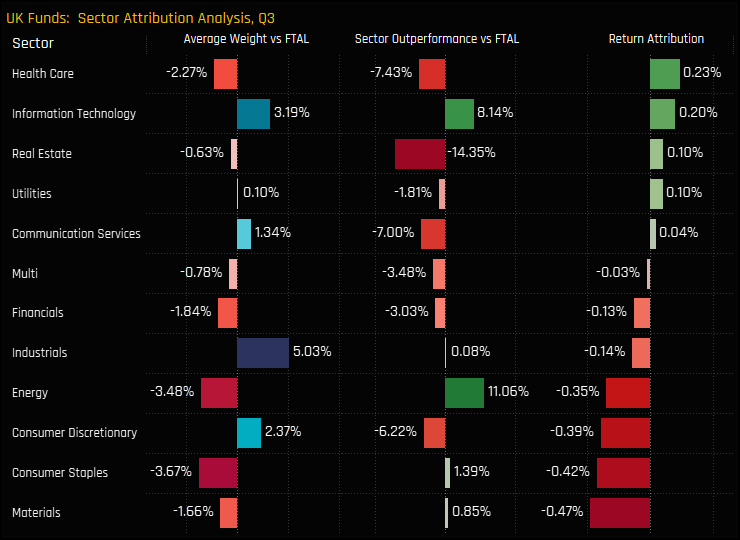

Relative to the FTAL benchmark, UK Active managers are running underweights in Consumer Staples, Energy and Health Care against overweights in Industrials, Technology and Consumer Discretionary. Whilst underweights in Health Care and overweights in Tech generated outperformance, these were outgunned by underweights in Consumer Staples and Materials and overweights in Consumer Discretionary.

Stock Positioning & Contribution

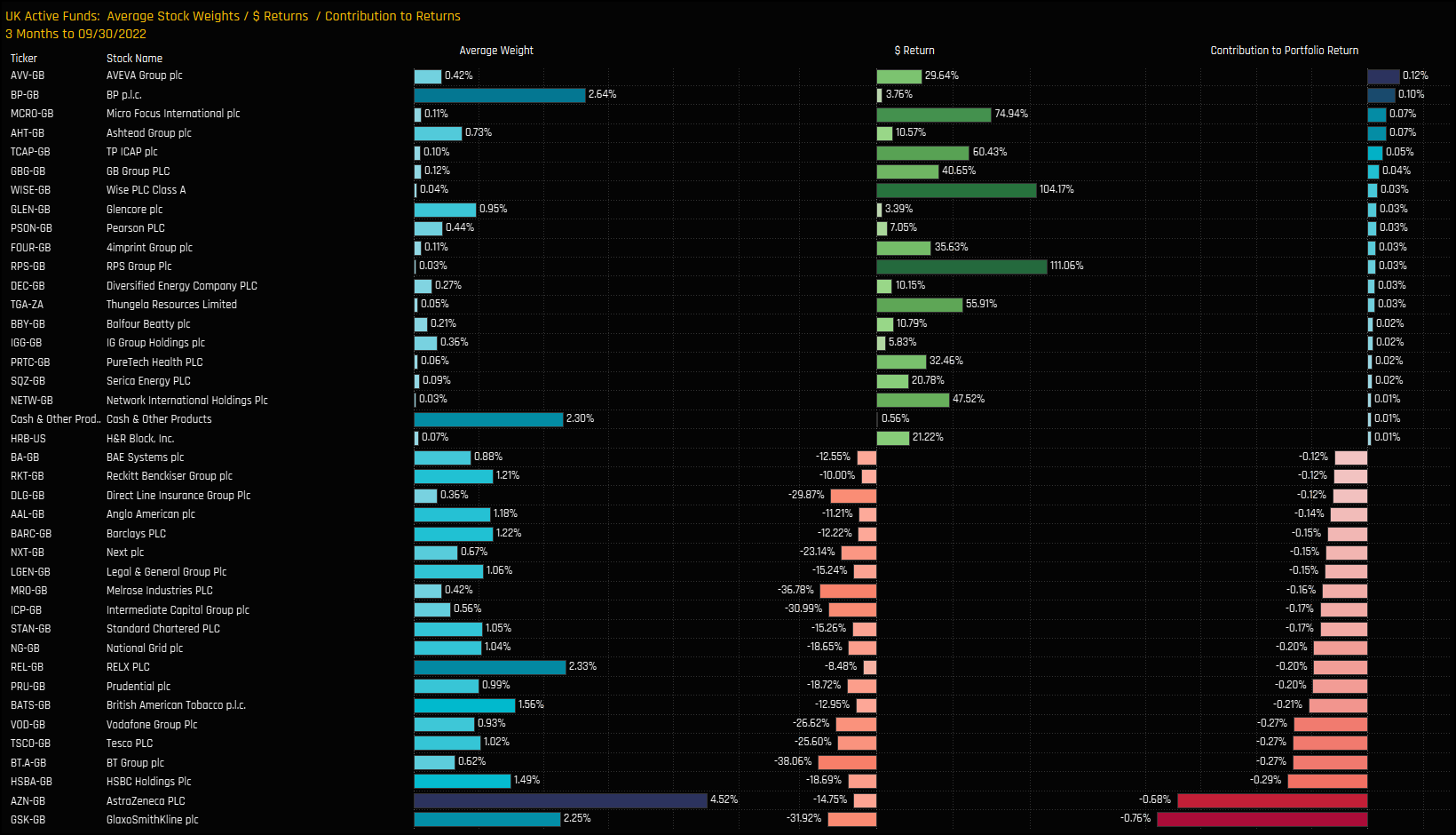

On a stock level, large weights in GlaxoSmithKline and AstraZeneca were key drivers of negative fund returns, in addition to smaller holdings in Tesco, BT Group, HSBC and Vodafone. Positive performers were few and far between on the quarter, with small holdings in AVEVA Group and larger holdings in BP p.l.c the highlights.

Stock Positioning & Attribution

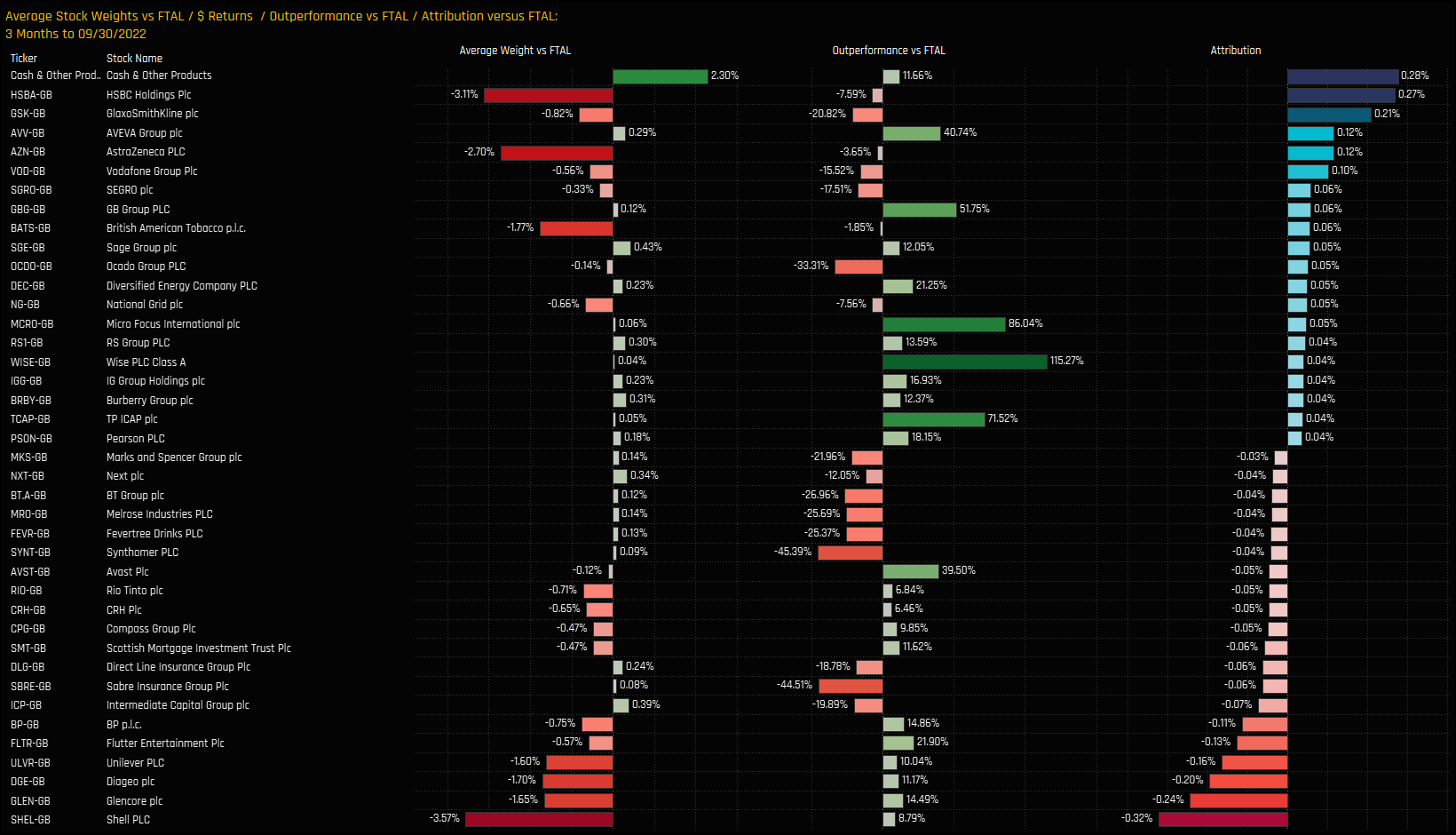

Relative to benchmark, Cash was king and generated +0.28% of relative outperformance, as did underweights in HSBC Holdings and GlaxoSmithKline plc. Offsetting these gains were underweights in Shell plc, Glencore plc and Diageo plc. Overall, a tough quarter for active UK managers, lets hope Q4 can salvage something from the year.

For more analysis, data or information on active investor positioning in your market, please get in touch with me on steven.holden@copleyfundresearch.com

{kind=link}