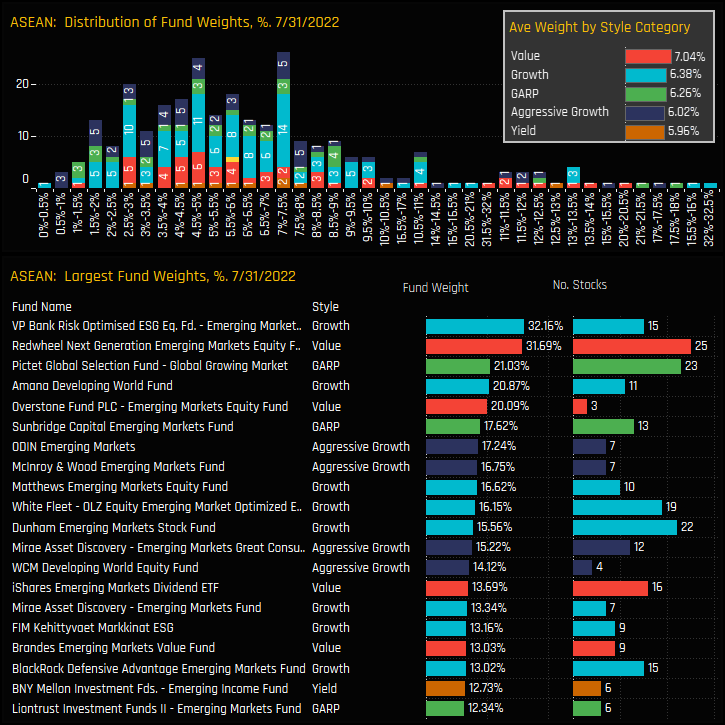

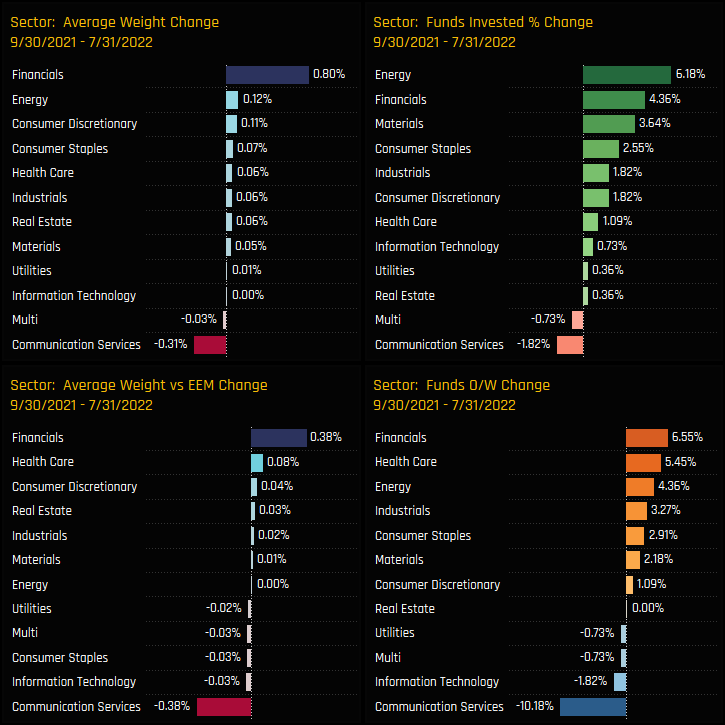

On an average weight basis, Financials have led the charge higher since September of last year, with average weights increasing by +0.8% and 6.55% of funds moving to an overweight stance. Energy and Materials stocks also saw fund participation move higher, with 6.18% and 3.64% of funds opening positions in each sector, respectively. Communication Services saw ownership levels fall over the period, whilst Technology and Utilities haven’t benefited from the ASEAN rotation.

{kind=link}