14 January

Emerging Markets

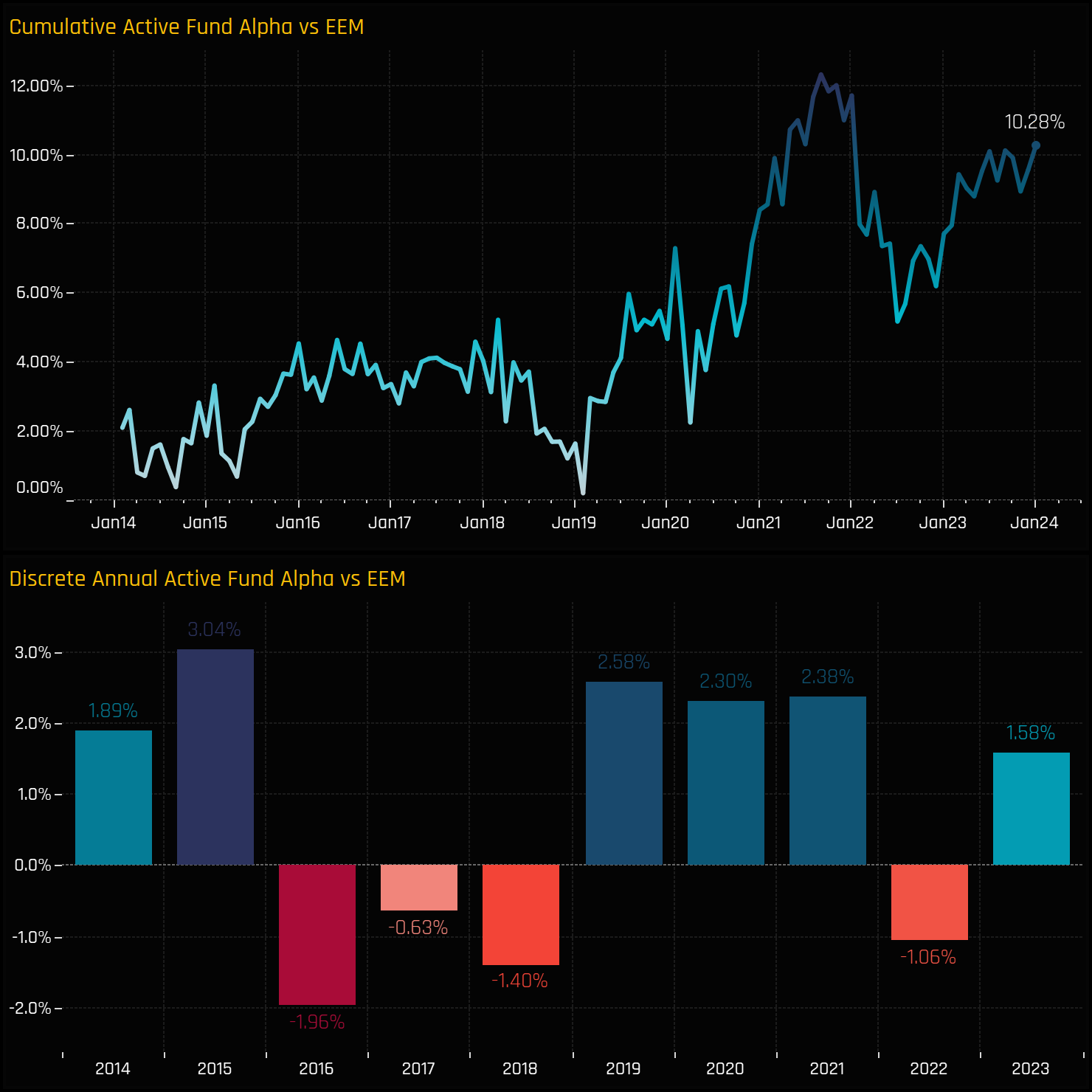

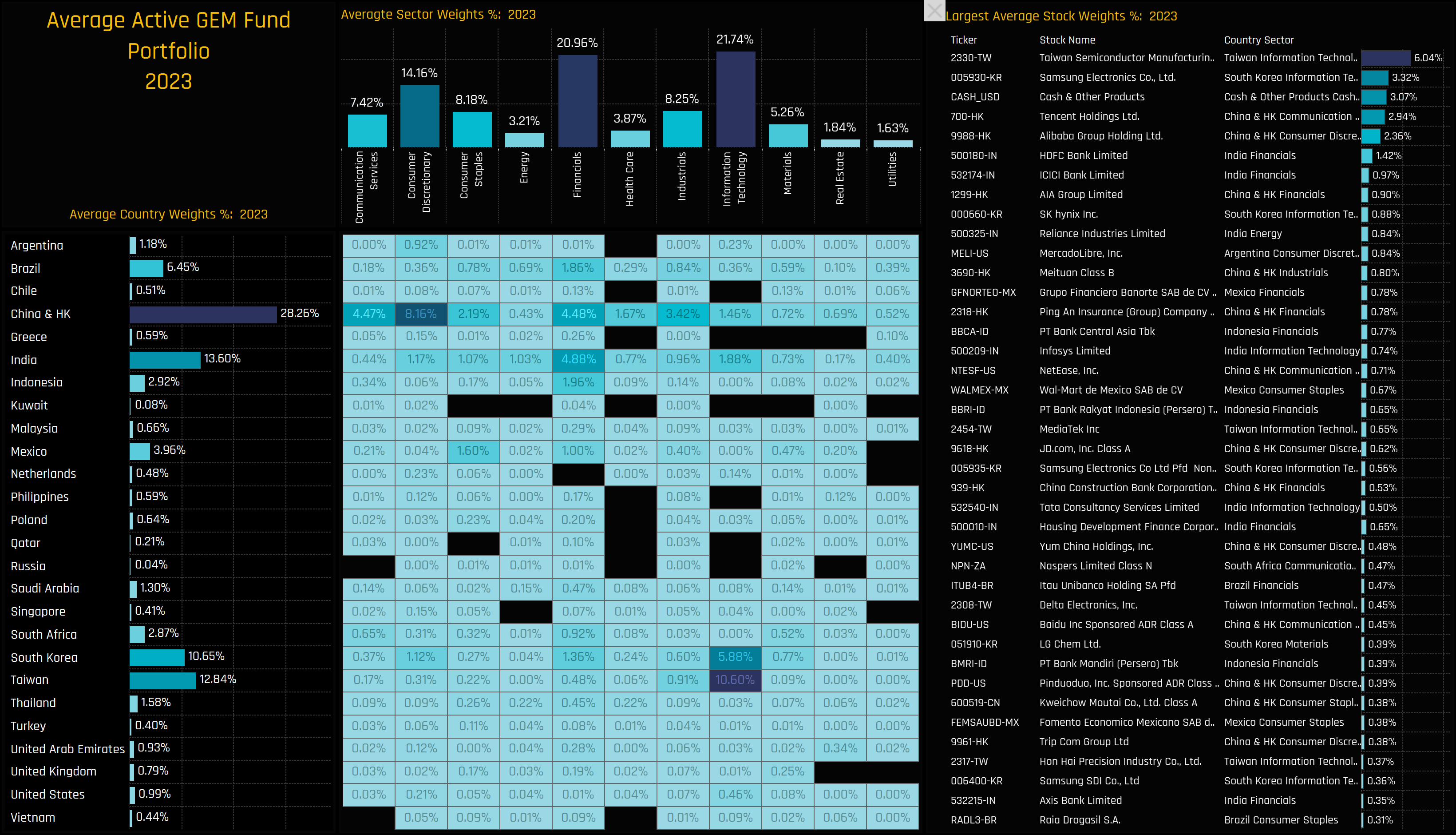

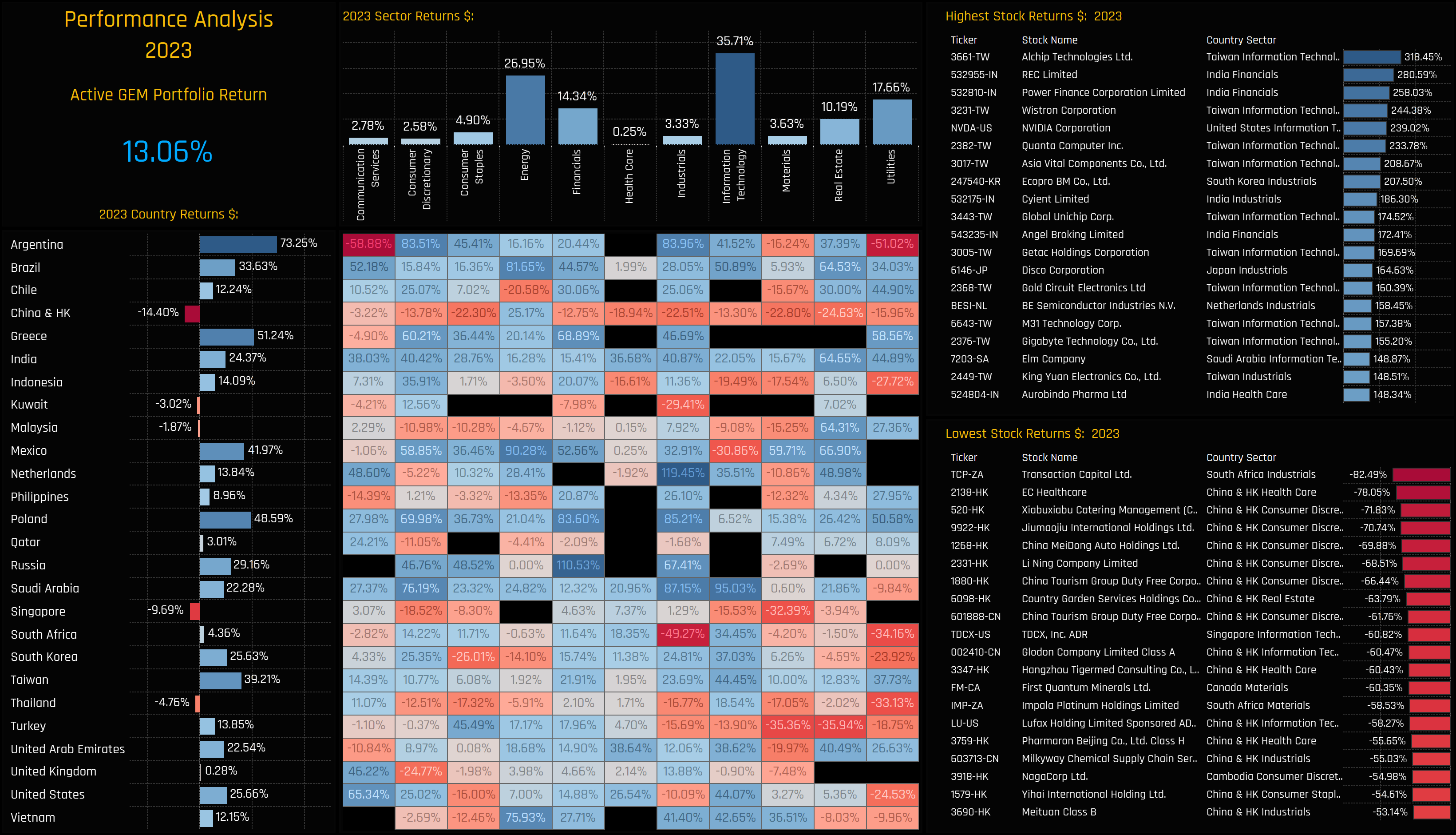

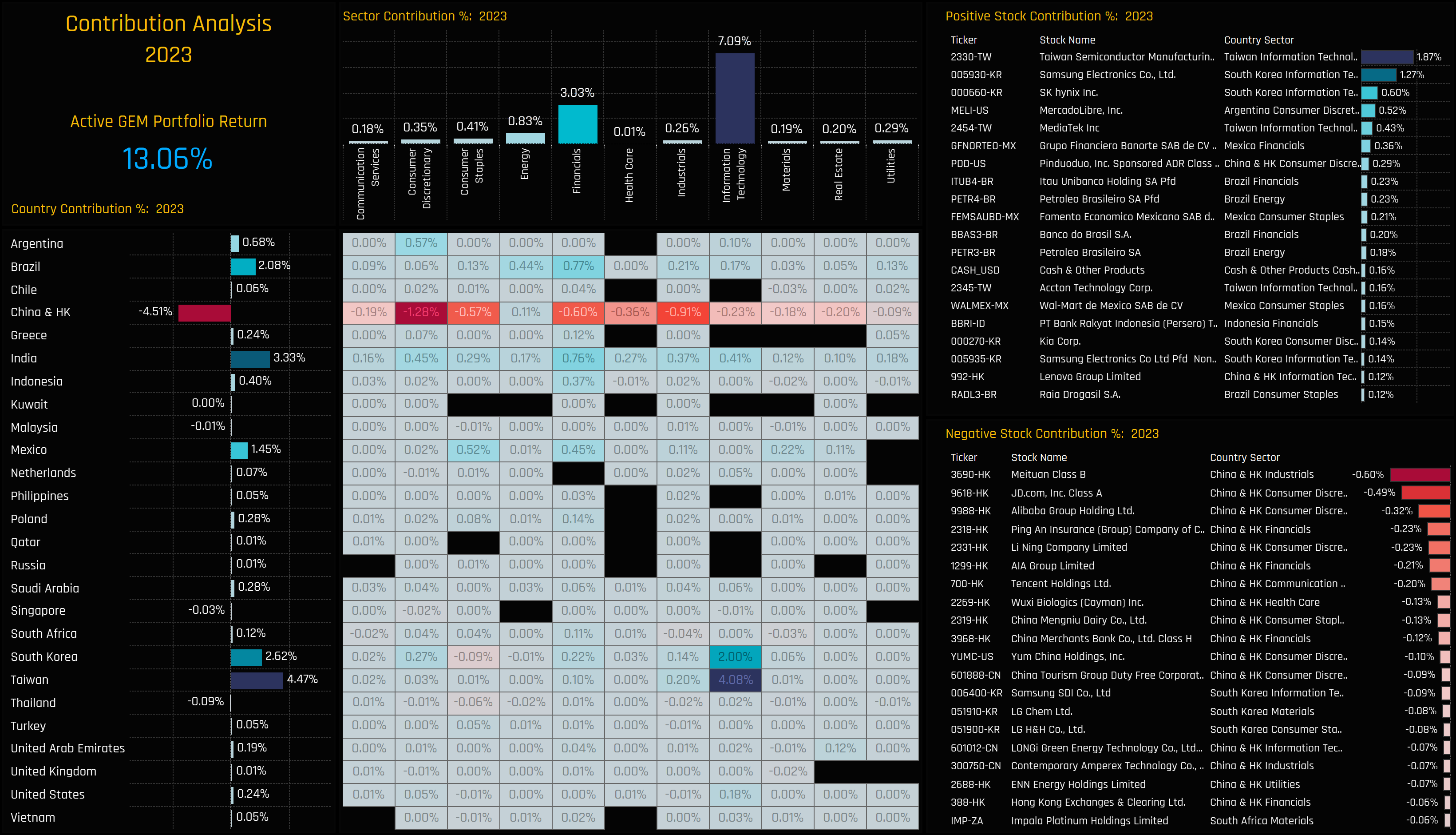

Emerging Market Active Fund Performance & Attribution Review, 2023

- Steve Holden

- 0 Comments

Related Posts

{kind=link}