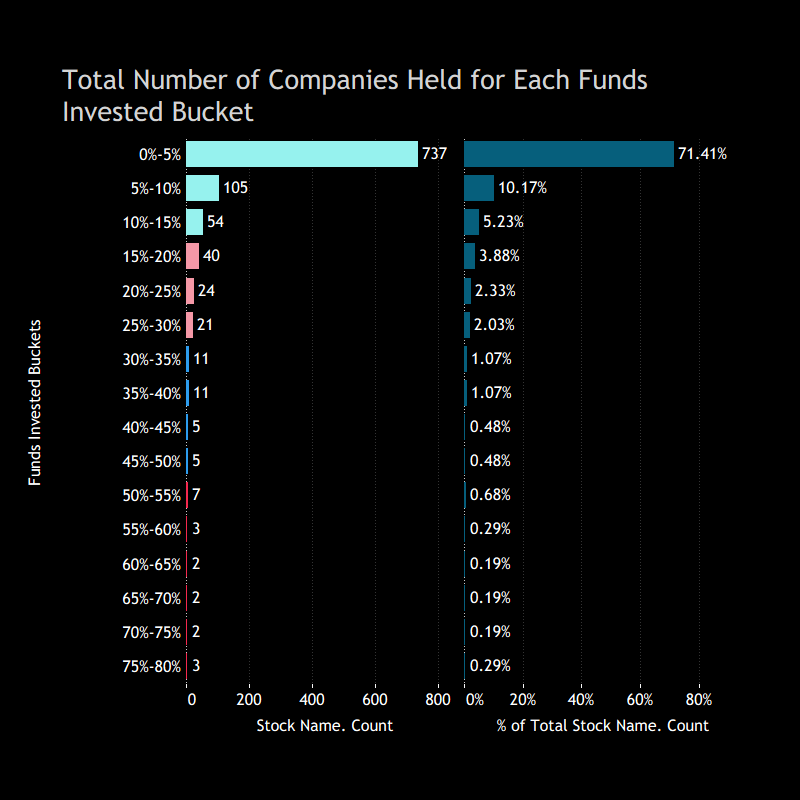

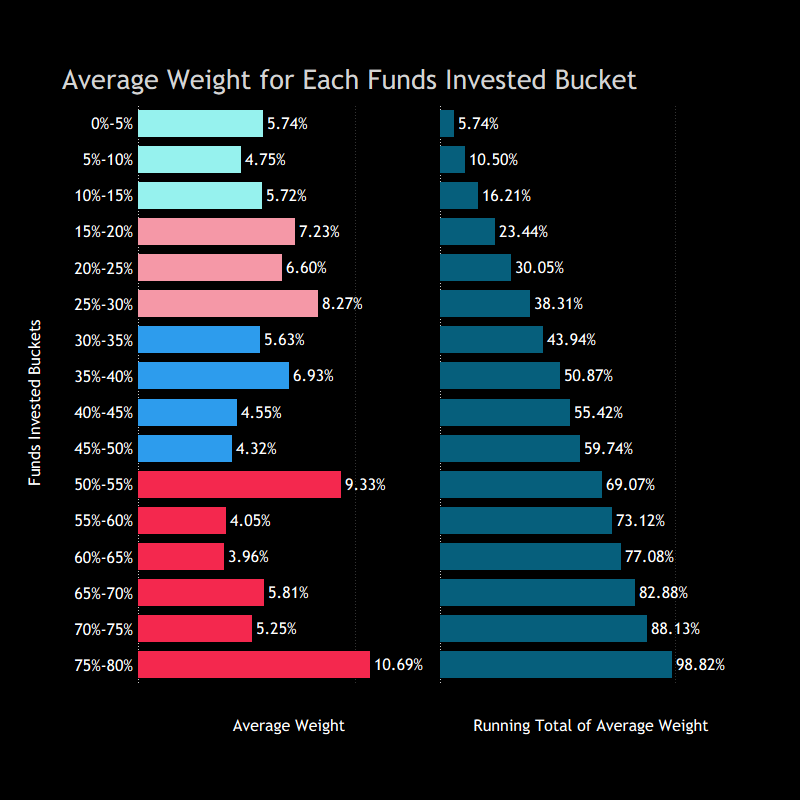

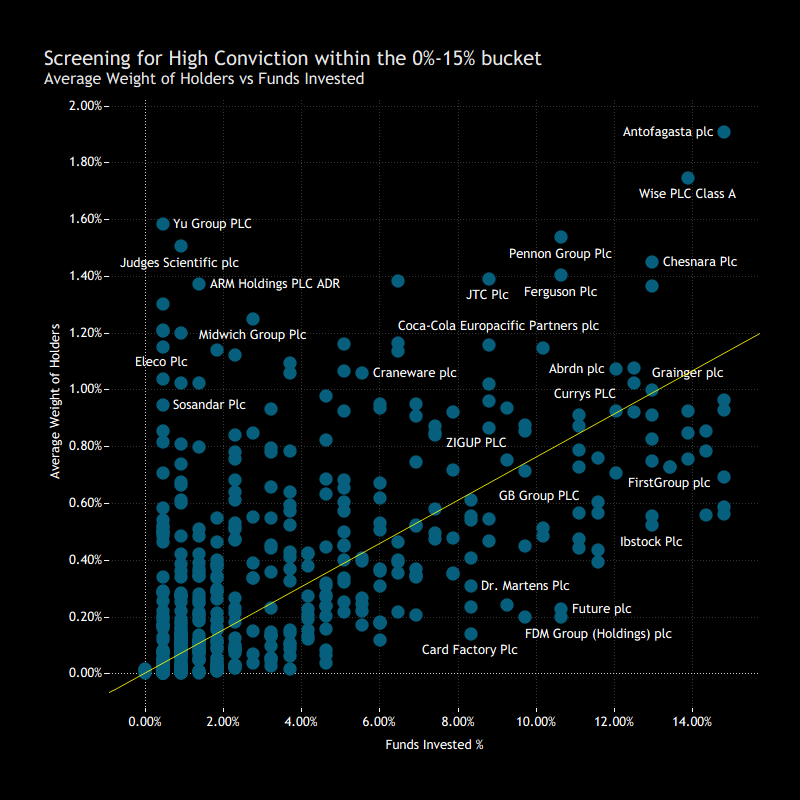

Early-Stage Conviction: Candidates for Broader Adoption

Comparing fund ownership against position size highlights a subset of names held with relatively high conviction despite limited participation. While most stocks in this bucket carry small weights, a number stand out with above-average allocations.

Names such as Antofagasta and Wise show higher average weights despite being held by a relatively small share of funds. Others including Pennon, Ferguson and Chesnara also sit above the broader cluster, indicating stronger conviction among existing holders.

Further along the spectrum, several names combine higher ownership (within the bucket) with still meaningful position sizes. JTC, Ferguson and Fevertree Drinks sit closer to the upper end of the range, while also appearing among the largest individual fund positions.

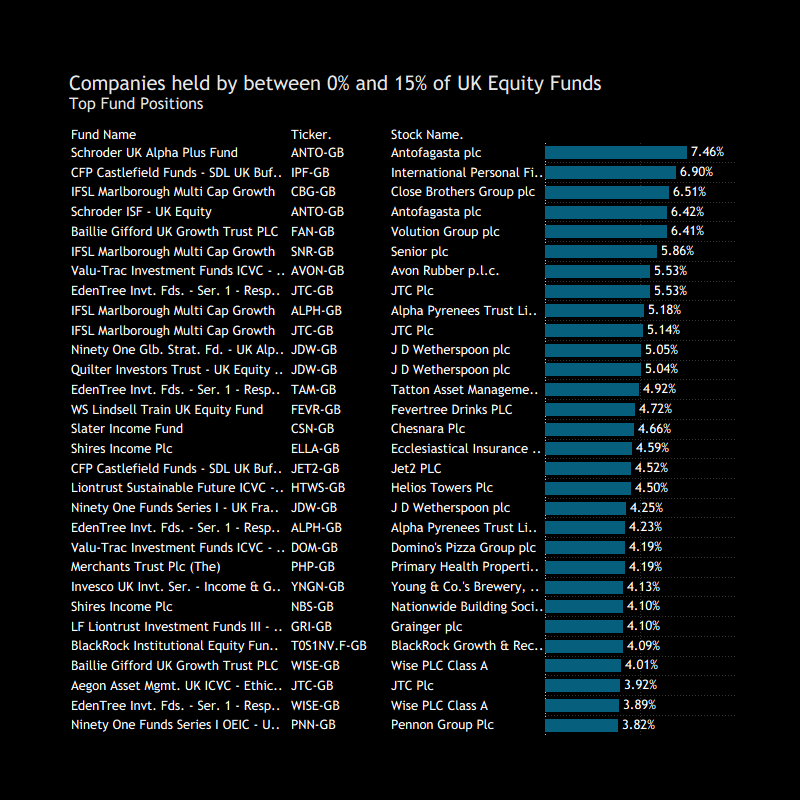

This is reinforced in the top holdings data, where stocks like Antofagasta, Close Brothers and Volution feature prominently — names that are not widely owned, but where participating funds are allocating capital in size.

{kind=link}